Intuitive Surgical, Stryker, and Tesla highlight robotics innovation in surgery, orthopedics, and AI-powered humanoid systems heading into 2026.

Sectors & Industries

September 24, 2025

Table of Contents

The robotics industry is entering a phase of rapid growth, driven by advances in artificial intelligence (AI) and automation across manufacturing, healthcare, and logistics. In the United States, several public companies in industrial automation, medical robotics, and AI-powered robotics are poised for strong performance heading into 2026.

Below is a mix of established leaders and high-growth up-and-comers in these sectors, examining their ticker symbols, robotics involvement, recent performance, key technologies, and market sentiment. A comparison table is provided at the end for a side-by-side summary.

Companies in industrial automation provide the robots, software, and control systems that power modern factories and warehouses. They are enabling “smart” production lines and supply chains by reducing human error and increasing efficiency. The following stocks offer exposure to this space:

Rockwell is a leading provider of industrial control systems and software that integrate with robotics on assembly lines and in logistics. Its Allen-Bradley controllers and FactoryTalk software help coordinate robotic arms and machines in manufacturing.

While Rockwell doesn’t manufacture robots, its automation platforms are the “brains” behind many robotic manufacturing cells. The company’s solutions power robotics in automotive, packaging, and other industries, and it has partnered with autonomous mobile robot makers (e.g. OTTO Motors) to expand into warehouse robotics.

Despite a 6% sales decline in Q2 2025, Rockwell improved margins and raised its full-year guidance, which drove an ~8% jump in its share price. Looking ahead, analysts project Rockwell’s earnings to grow ~16% in FY2026 on 7% higher sales, reflecting robust demand for automation. The company’s focus on digital transformation and high-margin software/services is gaining traction, positioning it for steady growth.

Allen-Bradley programmable logic controllers (PLCs), FactoryTalk industrial software, and safety/autonomy features for industrial robots. These allow seamless integration of robots into factory workflows. Rockwell also owns a stake in PTC, aligning it with industrial Internet-of-Things and digital twin technologies.

Market Performance:

.png)

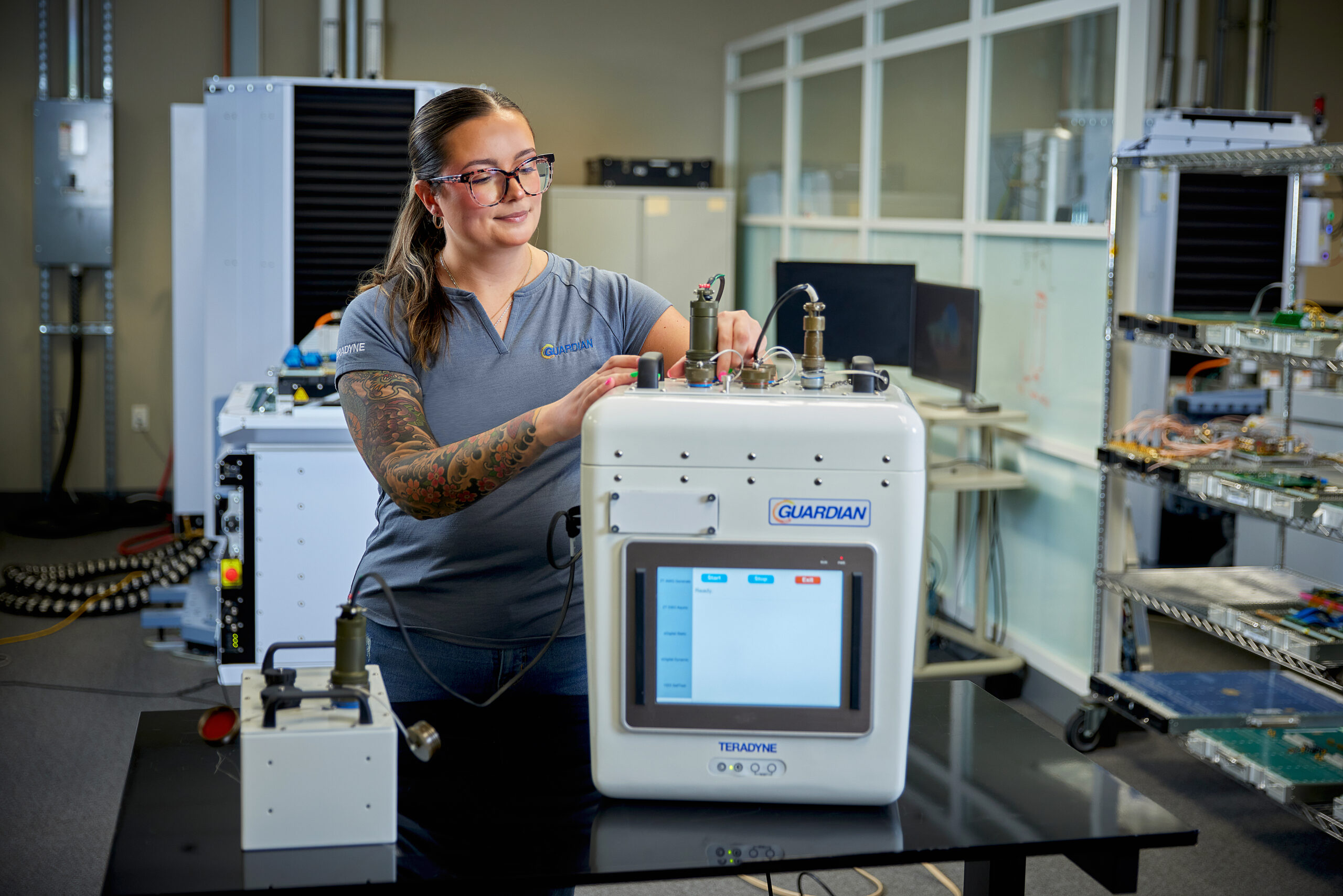

Teradyne is a unique play that straddles factory robotics and electronics testing. It makes automated test equipment for chips, but also owns Universal Robots, a top maker of collaborative robots (cobots), as well as Mobile Industrial Robots (autonomous mobile robots). Teradyne’s Universal Robots subsidiary commands over 50% of the global cobot market, with more than 50,000 cobots sold worldwide. These smaller, user-friendly robots are increasingly adopted by small and mid-sized manufacturers to automate tasks alongside human workers. Teradyne’s robotics segment also provides autonomous robots for material transport in factories. This robotics focus complements its core semiconductor test business.

The company’s automation portfolio is delivering growth. In Q1 2025, Teradyne reported a 14% year-over-year revenue jump, fueled by strength in semiconductor test and new robotics applications. This diversified revenue stream offers stability (from the electronics side) plus growth (from robotics). Analysts view TER as a balanced choice – its strong financials and cash flows provide stability, while the robotics segment adds high-growth potential. As cobot adoption rises and AI-driven automation spreads, Teradyne is expected to see continued demand.

Universal Robots’ collaborative robotic arms (e.g. UR5, UR10) which are leading cobots globally, Mobile Industrial Robots’ AMRs for warehouses, and Teradyne’s core J750 and UltraFLEX semiconductor test systems. Teradyne also integrates AI into its testing and robotics for smarter, more adaptive automation.

Analyst Sentiment

Teradyne is often highlighted among top automation/robotics stocks. Analysts note its “picks-and-shovels” role in the automation boom, with many maintaining Buy ratings. The stock is seen as a solid long-term play on robotics, given its dual exposure to booming chip demand and factory automation.

Market Performance:

.png)

Symbotic is a newer entrant focusing on AI-powered warehouse robotics systems. Its end-to-end automated warehouse solution uses fleets of robots and AI software to sort, store, and retrieve inventory for large retailers.

Symbotic’s technology is behind the futuristic warehouses of Walmart and others – robots on autonomous vehicles zip through warehouses to fetch products, guided by the company’s proprietary AI algorithms. By partnering with major retailers like Walmart and Target, Symbotic helps optimize supply chains through automation. This dramatically increases efficiency and accuracy in distribution centers.

Symbotic is a high-growth, not yet profitable company, but investor optimism is strong. Analysts forecast a share price target of about $45 by late 2025 (up from the mid-$30s in mid-2025), reflecting confidence in its expanding deployments. The company is rapidly scaling – it’s moving from serving U.S. partners to expanding into Europe and Asia. Symbotic achieved >100% revenue growth as it rolls out systems to new warehouses, and it has a substantial order backlog (Walmart alone has committed to automating dozens of distribution centers). While execution risks exist, Symbotic’s niche in the booming e-commerce logistics sector makes it a high-growth pick.

The Symbotic System an integrated hardware and software platform for warehouse automation. Key elements include autonomous mobile robots (for moving cases of product), automated storage structures, vision systems, and AI that orchestrates everything in real time. This proprietary technology can handle a retailer’s inventory with minimal human labor, significantly improving throughput.

And while the headlines may seem new, LevelFields AI had its eye on Symbotic last year.

On July 24, 2024, LevelFields featured Symbotic in a dedicated video, calling it “the Amazon of logistics.” The video detailed Symbotic’s:

Here’s a direct excerpt from that video:

“Symbotic revolutionizes the supply chain with flexible on-demand inventory management, seamlessly moving products to reduce transportation costs with high-density mixed SKU pallets. Their system transforms warehouses into strategic assets by lowering costs, boosting efficiency, and enhancing safety and capacity.”

— LevelFields AI video, July 24, 2024

Symbotic’s story began with CEO Rick Cohen’s family grocery business. A simple prototype on a sheet of plywood evolved into a robotics system now redefining global logistics—and LevelFields flagged it before the crowd.

Analyst Sentiment

Bullish but risk-aware. Symbotic’s strong partnerships give credibility to its technology, and analysts highlight its “blistering growth potential” in warehouse automation. Market sentiment is optimistic given the secular trend toward automated fulfillment, though investors understand Symbotic is an emerging company (with stock volatility and ongoing net losses). For those seeking high-growth exposure to AI robotics, SYM is often recommended, provided one can tolerate the risk.

Market Performance:

.png)

Zebra is an established mid-cap that has transformed from a barcode printing company into an industrial tech leader offering robotics and automation solutions for logistics. Its products span barcode scanners, RFID tags, machine vision systems, and since 2021, autonomous mobile robots for warehouses.

Zebra’s move into robotics was cemented by its acquisition of Fetch Robotics, whose Autonomous Mobile Robots (AMRs) are used in warehouses for material handling and order picking. These robots, combined with Zebra’s tracking technology, create smart warehouses that can boost productivity by ~30% for major clients. Zebra also provides machine vision and fixed industrial scanners (enhanced by its 2022 acquisition of Matrox Imaging), which help guide robotic systems.

After some soft demand in 2023, Zebra saw a sharp rebound in 2024. In Q3 2024 its enterprise automation segments grew dramatically – mobile computing and data capture sales jumped 33.7% year-over-year, while its tracking segment (RFID, etc.) grew 26.5%. The company expected 28–31% revenue growth in Q4 2024 as supply chains normalized and orders picked up. This turnaround drove Zebra’s stock up about 43% year-to-date by late 2024. With continued e-commerce growth and new acquisitions (e.g. the pending buyout of AI firm antuit.ai and touch-screen maker Elo), Zebra’s financial outlook is positive. The company is also improving margins via cost management, further boosting earnings.

Warehouse AMRs (from Fetch Robotics) for automated picking and material movement; RFID tracking systems that give real-time visibility of assets; industrial machine vision cameras and sensors; and its legacy of barcode printers and mobile computing devices. By integrating these, Zebra offers an end-to-end “visibility and productivity” solution for logistics and manufacturing.

Analyst Sentiment

Its recent growth resurgence and strategic expansion into robotics have impressed the market. Investors see Zebra as a key beneficiary of warehouse automation trends and have rewarded it with a rising valuation (around $20B market cap) as confidence grows in its execution. Analysts do note that Zebra’s success is tied to cyclical capital spending trends, but its strong positioning in retail and logistics automation underpins a favorable long-term outlook.

Market Performance:

Medical robotics is revolutionizing healthcare through surgical assistance, rehabilitation, and other applications. Companies in this sector build robots that can perform or assist in procedures with greater precision and often less invasiveness, improving patient outcomes. Below are two top stocks in medical robotics – a clear market leader and a major medical device player – both leveraging robotics for growth:

.png)

Intuitive Surgical is the undisputed leader in robotic-assisted surgery, best known for its da Vinci Surgical System. The company focuses on minimally invasive surgery across disciplines like urology, gynecology, and general surgery.

Intuitive’s da Vinci robots allow surgeons to perform complex procedures through tiny incisions, using robotic arms controlled from a console. With over 7,500 da Vinci systems installed worldwide and more than 11 million surgeries completed to date, Intuitive has built an enormous installed base that generates recurring revenue from instrument sales and servicing. It continues to innovate new robotic tools and software (e.g. advanced imaging, AI guidance) to expand what these robots can do.

Intuitive has been delivering steady growth. In Q1 2025, the company reported earnings of $1.81 per share, beating estimates, on strong growth in procedure volumes. Procedure count – a key metric – has been rising double-digits annually as robotic surgery gains wider adoption. Intuitive is also expanding geographically (with growing sales in Asia) and working on next-generation systems (the recently FDA-approved da Vinci SP and upcoming da Vinci X platforms). Analysts remain optimistic that Intuitive can sustain ~10–15% annual revenue growth; in fact, its sales have grown ~13% annualized over the past five years and analysts expect a similar trajectory going forward. With competitors still far behind, Intuitive’s dominance and continual innovation suggest a strong outlook into 2026.

The da Vinci Surgical System (multiple models including Xi, X, SP) is Intuitive’s flagship. It also offers the Ion system for robotic bronchoscopy (lung procedures). Key technologies include 3D HD vision, wristed micro-instruments, and an expanding suite of AI-enhanced software for things like surgical training, automated suturing, and data analytics in surgery. Intuitive’s ecosystem (training programs, surgeon community, etc.) reinforces its moat.

Analyst Sentiment

Strongly positive. Intuitive is often cited as a top “must-own” healthcare technology stock. Analysts highlight its high margins, debt-free balance sheet, and huge competitive lead. The stock carries a “Buy” rating consensus on Wall Street and price targets in the mid-$500s (around $590 per share was a target cited in one 2025 report) – a reflection of moderate upside since the stock already performed well. While its valuation is not cheap, market sentiment is that Intuitive’s long-term growth runway in surgical robotics justifies a premium.

Market Performance:

.png)

Stryker is a large medtech company that has embraced robotics to enhance its product offerings, especially in orthopedics. It markets the Mako SmartRobotics system for joint replacement surgeries and has been integrating robotics across its surgical tools portfolio.

Stryker’s Mako robotic-arm assisted surgery platform is used for knee and hip replacements, enabling surgeons to pre-plan procedures in 3D and execute with robotic precision. This improves implant alignment and patient outcomes. Stryker has installed hundreds of Mako systems in hospitals worldwide, leveraging robotics to drive sales of its replacement joints. The company is also developing robotic applications in spine surgery and other areas (it unveiled an updated Mako and discussed future spine robotics at the AAOS 2025 conference).

Stryker’s embrace of robotics has contributed to strong financial results. In Q2 2025, the company posted 11.1% year-over-year sales growth to $6.1 billion, with broad momentum across its orthopedic and surgical divisions. Notably, Stryker raised its full-year 2025 guidance to 9.5–10% organic sales growth (and ~$13.5 in EPS) amid robust demand. Management cited the success of its new products – including Mako – as growth drivers. The MedSurg & Neurotechnology segment (which houses Mako) saw double-digit growth. Going into 2026, Stryker expects continued high-single to low-double-digit growth, fueled by an aging population’s need for joint replacements and the premium pricing its advanced tech commands.

Mako SmartRobotics for knee, hip (and soon shoulder/spine) surgeries – combining a robotic arm, specialized implants, and Stryker’s AccuStop haptic feedback to assist surgeons. Beyond Mako, Stryker’s broader portfolio includes surgical navigation systems, AI-driven imaging (e.g., its Blueprint planning software), and a range of medical devices from endoscopes to hospital beds – many of which are seeing incremental improvements from digital and robotic integration.

Analyst Sentiment

Moderately bullish. Stryker is a well-covered large-cap with generally favorable ratings. As of mid-2025, 38 analysts collectively rated SYK a Buy with a 2025 price target around $337 (the stock has since risen above that). Analysts are impressed by Stryker’s consistent execution and its strategy of using technology (like Mako) to differentiate itself in crowded medical device markets. There are some macro caution points (elective procedure trends, hospital capex budgets), but overall Wall Street maintains a “cautiously optimistic” outlook. The successful integration of robotics into its line has solidified Stryker’s growth narrative, which bodes well for 2026.

Market Performance:

AI-powered robotics companies leverage artificial intelligence as a core element of their products – from autonomous vehicles and humanoid robots to software “bots.” These firms often straddle the line between pure robotics and broader AI tech. They are included here because their innovations in AI are driving real-world robotics applications:

.png)

NVIDIA is not a robot maker, but it provides the critical AI computing platforms that enable advanced robotics. Its GPUs and AI chips act as the “brains” for many robots, and NVIDIA has developed specialized robotics software (like its Isaac platform) to accelerate autonomous machine development.

Virtually every category of cutting-edge robot – from self-driving cars to warehouse robots to drones – can leverage NVIDIA’s technology. The company’s Jetson embedded AI modules and Isaac SDK help developers build autonomous robots with computer vision and deep learning capabilities. NVIDIA also offers Omniverse and Isaac Sim simulation tools for training robots in virtual environments. In short, NVIDIA provides the AI infrastructure that makes modern robotics possible, and it continuously innovates new AI models for robotics (e.g. recently announcing an open humanoid robot AI model at its GTC conference).

NVIDIA has been one of the market’s top performers thanks to the AI revolution. Its revenues surged in 2023–2025 primarily from data center GPU sales (for AI training), but robotics is cited as an emerging contributor as well. In fact, NVIDIA’s robotics and automotive segments helped drive record revenues in recent quarters. In Q2 2025, net income was up 59% year-on-year amid the AI boom. The stock roughly tripled in 2023 and has held those gains in 2024–2025, reflecting high expectations. Going into 2026, NVIDIA’s outlook remains strong: demand for its AI chips in cloud computing, autonomous vehicles, and robotics is expected to outstrip supply. Analysts continue to see upside, though at a more measured pace, and the consensus rating is “Moderate Buy” as of late 2025.

NVIDIA’s A100/H100 GPUs (used in training AI models that robots use for perception and decision-making), Jetson Orin modules (small AI computers that go into robots and drones), and software like CUDA libraries for robotics, Omniverse, and Isaac. The company is also building the DGX AI supercomputers and cloud services that companies use to develop robotics AI. These technologies have made NVIDIA almost synonymous with AI computing in robotics.

Analyst Sentiment

Positive (Buy-rated). NVIDIA is widely regarded as a cornerstone of any AI/robotics investment strategy. It’s often the top-mentioned stock when discussing robotics themes. While some analysts caution about valuation, most agree NVIDIA has a dominant position in the AI hardware market that will extend into robotics. MarketBeat reports the stock carries a Moderate Buy consensus with price targets still above current levels. In summary, sentiment is that NVIDIA will continue to be a key beneficiary of robotics and AI trends through 2026 and beyond.

Market Performance:

.png)

Tesla, known for its electric cars, is also at the forefront of AI-powered robotics in two notable ways: its vehicles operate with advanced self-driving AI (essentially robots on wheels), and the company is developing “Optimus,” a general-purpose humanoid robot. CEO Elon Musk often emphasizes that Tesla is as much an AI & robotics company as it is a car manufacturer.

Tesla’s cars use an array of sensors and the company’s proprietary Full Self-Driving (FSD) AI to navigate roads autonomously – putting Tesla among the leaders in robotic vehicle technology. The company is also leveraging its AI expertise to create Optimus, the humanoid robot unveiled in prototype form in 2022. Optimus is intended for tasks in factories or even homes in the future. Musk has even claimed that Optimus “could be worth more than the car business” eventually. In addition, Tesla’s manufacturing operations heavily use robotics (its gigafactories are famously automated). All these factors place Tesla firmly in the robotics conversation.

Tesla’s stock saw a huge rally in the past year (over +100% in 1-year return as of early 2025), fueled by enthusiasm for AI and Tesla’s continued growth in vehicle deliveries. Financially, Tesla is growing revenue (~$90B in the past year) but has faced margin pressures due to vehicle price cuts. Looking ahead, any material progress on FSD software or Optimus could unlock new revenue streams. The market outlook is optimistic that Tesla will maintain a high growth rate through 2026 by scaling vehicle production and potentially monetizing its self-driving tech (e.g. robotaxi services). However, some skepticism exists: at a 2024 demo, observers noted that Tesla’s humanoid robot still required human teleoperation for some functions, suggesting it’s far from fully autonomous. Therefore, while the conceptual upside from Tesla’s robotics initiatives is enormous, timelines are uncertain.

FSD (Full Self-Driving) software, which uses neural networks and Tesla’s custom AI chip (Dojo) to enable autonomy in cars. The Optimus robot, still in development, which shares some AI hardware/software with Tesla cars. Additionally, Tesla’s prowess in battery and actuator technology (from cars) is an asset in building robots. Tesla also employs AI in its energy products and humanoid robot training simulations.

Analyst Sentiment

Divided but generally bullish. Tesla is a trillion-dollar company with a wide range of analyst opinions. On average, it’s rated a Buy/Overweight, as many see it leading the future of both EVs and AI-driven transportation. The robotics angle (Optimus) is often not fully factored into valuations – it’s seen as a “free” long-term option by bulls. Some analysts are more cautious, labeling Tesla’s robot plans as overhyped until proven otherwise. In summary, market sentiment acknowledges Tesla as a transformative tech player (hence the high valuation), with the robotics initiatives serving as a potential catalyst that could make the company even more valuable by 2026 if successful.

Market Performance:

.png)

Serve Robotics is a small-cap pure-play robotics company specializing in self-driving delivery robots. Spun off from Uber, it designs toaster-sized sidewalk robots that can carry food and small packages to customers autonomously, addressing the “last-mile” delivery challenge.

Serve’s wheeled robots use AI and sensors to navigate city sidewalks and deliver orders without human drivers. The company has a partnership with Uber Eats, meaning its robots are being tested and used to deliver meals in select urban markets. This positions Serve at the intersection of robotics and the on-demand economy, with a first-mover advantage in sidewalk delivery. As demand grows for contactless delivery and cost-effective logistics, Serve’s robots offer a compelling solution.

After listing publicly in April 2024, Serve’s stock has been volatile – it traded down about 35% from its IPO by early 2025, reflecting the challenges early-stage tech companies face. However, the company’s operational metrics are surging: in 2024, Serve achieved +773% revenue growth year-over-year (albeit from a small base) and planned to deploy 2,000 robots by the end of 2025. Such growth underscores the high demand and rapid expansion of its services. Looking ahead, Serve’s financial outlook depends on scaling deployments and improving unit economics. If it can successfully expand with Uber and other partners, the revenue could continue exponential growth into 2026. As a sub-$1 billion market cap company, it has significant room to grow – but also carries high risk.

Serve’s autonomous sidewalk robots, which are battery-powered four-wheeled rovers equipped with cameras, LiDAR, and AI navigation software. They are designed to safely maneuver on sidewalks and carry about 50 pounds of goods in a secure compartment. Serve uses machine learning for route planning and obstacle avoidance, and a cloud fleet management system to supervise and coordinate its robot fleet. Its technology emphasis is on safety and reliability to gain city regulatory approvals.

Analyst Sentiment

Speculative but enthusiastic. Being newly public, Serve Robotics has limited analyst coverage. The thematic appeal of its story – robotics + food delivery – has attracted investor interest, but also caution given its heavy spending and nascent stage. Commentary from tech investing sites suggests high growth potential (the company is clearly in hyper-growth mode) but also notes the valuation must be considered carefully. In short, market sentiment among early investors is that Serve could be a long-term winner in delivery automation if it executes, but it remains a speculative pick for 2026 with a need to prove its unit economics and fend off competition.

Market Performance:

Symbotic’s meteoric rise in AI logistics didn’t go unnoticed.

In fact, LevelFields AI featured Symbotic in a video on July 24, 2024, calling it “the Amazon of logistics.” That was months before many investors caught on. Their platform highlighted its $424 million in revenue, 59% revenue growth, and 67% operating income growth in Q1–Q2 of fiscal 2024—all before Symbotic gained wider momentum.

This is exactly what LevelFields does best.

By scanning 6,300+ companies and over 30,000+ press releases, earnings transcripts, filings, and news sources per minute, LevelFields identifies high-impact event catalysts—before they drive stock price surges.

.png)

For robotics investors, that means early alerts on:

With Level 2 Premium Access, you get weekly trade setups, curated stock watchlists, macro context, and alert filters customized to your exact sector focus—including robotics, AI infrastructure, and industrial automation.

Real-time alerts

Entry + exit targets

Backtested scenarios with win-rate data

And yes, Symbotic was one of them

Instead of getting buried in endless news feeds, you can zero in on the events that matter most—and act with confidence. That’s why both active traders and long-term investors use LevelFields AI to track defense-related AI announcements and build smarter positions.

Join LevelFields now to be the first to know about events that affect stock prices and uncover unique investment opportunities. Choose from events, view price reactions, and set event alerts with our AI-powered platform. Don't miss out on daily opportunities from 6,300 companies monitored 24/7. Act on facts, not opinions, and let LevelFields help you become a better investor.

AI scans for events proven to impact stock prices, so you don't have to.

LEARN MORE{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}