Analysts see Cava’s restaurant margins aligning with Chipotle’s, fueling optimism for scalable growth across new store openings.

Sectors & Industries

July 22, 2025

Table of Contents

A decade ago, Chipotle Mexican Grill was the unrivaled darling of fast-casual dining – a pioneer that proved customers would line up for customizable burritos made with fresh ingredients. Today, a new contender, Cava, is drawing comparisons to Chipotle’s early days. Cava, a Mediterranean-inspired chain, has surged in popularity with its build-your-own bowls and pitas, leading some to dub it the “Chipotle of Mediterranean”.

In 2023, Cava went public and saw its stock skyrocket amid investor excitement. By mid-2025, the two companies stand in stark contrast: one is a seasoned giant with nearly 4,000 restaurants across multiple countries, the other a rising star with a few hundred locations in the U.S. This feature will compare Cava and Chipotle’s financial performance, stock momentum, business strategies, and expansion plans – highlighting why Chipotle remains ahead and what challenges Cava faces in closing the gap.

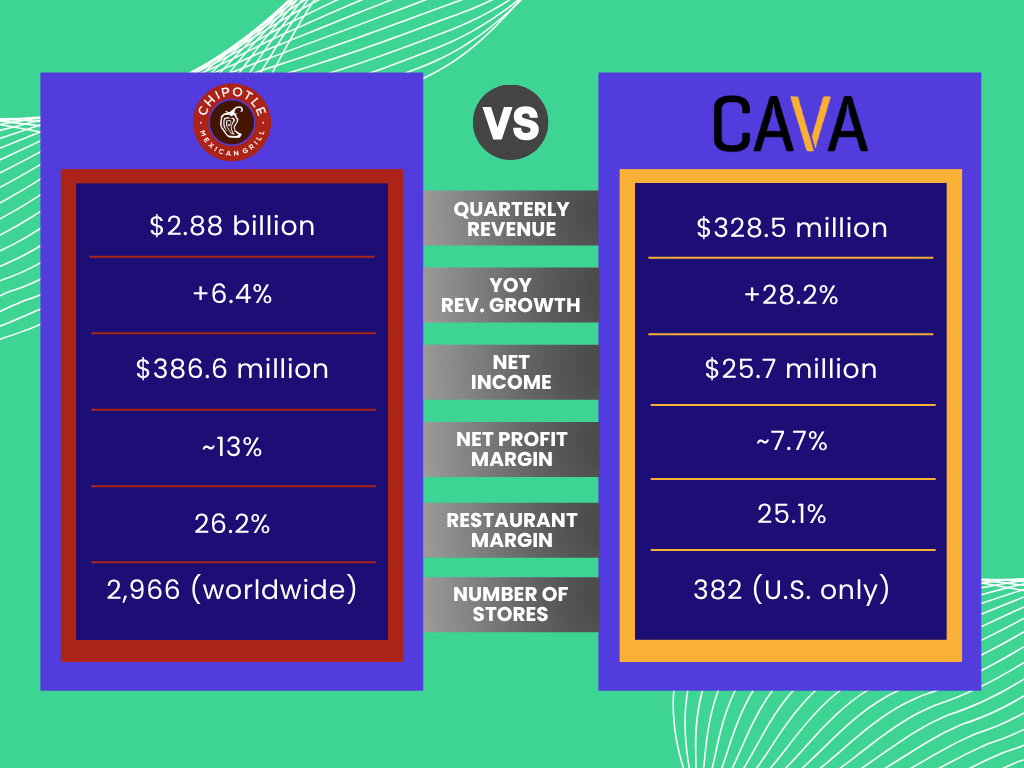

When it comes to quarterly finances, Chipotle, $CMG dwarfs Cava in sheer size, but Cava, $CAVA is growing at a blistering pace. In the first quarter of 2025, Chipotle’s revenue reached $2.9 billion, up 6.4% year-over-year. Cava’s Q1 revenue was much smaller at $328.5 million, but it jumped 28.2% from the prior year – a growth rate over four times Chipotle’s. Chipotle’s scale gives it a significant advantage in absolute profit: Q1 net income was $386.6 million for Chipotle, whereas Cava earned $25.7 million. However, Cava more than doubled its bottom line from a year earlier (net income up 115%), showing improving economics as it expands.

Despite the gap in earnings, Cava’s profitability metrics are rapidly approaching Chipotle’s. Chipotle’s net profit margin in Q1 2025 stood around 13%, reflecting its mature efficiency. Cava’s net margin was about 7.7% – roughly half of Chipotle’s – but notably higher than Cava’s margin a year ago. In fact, excluding a one-time tax benefit, Cava’s underlying margin has been in the mid-single digits, indicating there is still room to improve to reach Chipotle’s level. On a restaurant-operating basis, the two are surprisingly close: Chipotle’s restaurant-level operating margin was 26.2% in Q1 (down slightly from 27.5% a year prior), while Cava’s restaurant-level profit margin was 25.1% (essentially flat year-over-year). This means that at the store level, Cava’s unit economics “are virtually identical to Chipotle’s,” as one analyst noted, underpinning optimism that Cava can scale successfully.

Both companies faced cost pressures in early 2025, but their approaches differed. Chipotle cited higher food inflation (especially avocados, dairy, and chicken) and wage increases as headwinds that slightly dented its restaurant margins. Its operating margin still ticked up to 16.7% thanks to some menu price hikes and cost controls. Cava, by contrast, has prided itself on not leaning heavily on price increases. CFO Tricia Tolivar explained that Cava’s strategy of keeping price hikes below the inflation rate helped drive more customer traffic. In Q1, Cava saw same-store guest traffic jump 7.5%, an impressive feat in an industry where many peers saw traffic stagnate. This traffic growth, combined with modest menu price upticks, fueled a 10.8% surge in comparable sales for Cava.

By comparison, Chipotle’s comparable restaurant sales fell 0.4% in Q1 as transactions declined slightly – a sign that even industry leaders are not immune to consumer spending shifts. Chipotle’s CEO (as of 2025) Scott Boatwright acknowledged the “slowdown in consumer spending” and weather challenges impacting Q1, but emphasized that Chipotle is doubling down on execution and innovation to reignite growth. Indeed, Chipotle’s management expressed confidence in returning to positive traffic growth by the second half of 2025.

To put the financial matchup in perspective, here’s a side-by-side look at some key metrics from the first quarter of 2025:

The table highlights Chipotle’s dominance in scale – roughly 10 times the annual sales of Cava and a market value an order of magnitude larger. Yet Cava’s double-digit growth rates and improving margins illustrate why it’s capturing investor attention. As CEO Brett Schulman noted, Cava’s trailing twelve-month revenue has now surpassed $1 billion for the first time, a milestone that signals Mediterranean cuisine’s rise as what he calls “the next large-scale cultural cuisine category”. For Chipotle, posting $9+ billion in yearly sales is business as usual – but for Cava, hitting $1 billion validates its concept and encourages further expansion.

On Wall Street, the incumbent Chipotle and the upstart Cava have both been stock market darlings, though for different reasons. Chipotle’s shares have delivered steady gains on the back of reliable earnings growth and a strong brand. In 2024, Chipotle’s stock climbed over 40% (figures adjusted for a 50-for-1 stock split in mid-2024), reflecting investor confidence in the company’s post-pandemic performance and digital initiatives. By early 2025, Chipotle’s market capitalization hovered around $75–80 billion, firmly establishing it as one of the world’s most valuable restaurant companies. Chipotle has even been returning cash to shareholders, repurchasing over $550 million of stock in Q1 2025 alone – a sign of management’s confidence in the business.

Cava’s stock story, meanwhile, has been one of meteoric rises and high expectations. After its June 2023 IPO, Cava’s share price surged, at one point more than doubling from its IPO price as enthusiastic investors piled into the “next Chipotle.” In fact, by late 2024, Cava’s stock was up about 188% year-to-date, giving the young company a market cap in the ballpark of $14 billion. That valuation implied a price-to-sales multiple nearly twice that of Chipotle’s (Cava trading around 15× sales vs. Chipotle’s 8×) – a clear sign that investors were banking on rapid growth. Such a rich valuation came with volatility: Cava’s shares have been prone to big swings as the market digests each earnings report and growth outlook. By mid-2025, Cava’s market cap had settled closer to ~$10–11 billion, after some of the initial euphoria moderated. Even so, Wall Street sentiment remains broadly optimistic. KeyBanc Capital Markets initiated coverage of Cava with an “Overweight” rating and a $100 price target, explicitly comparing Cava’s long-term unit expansion opportunity to Chipotle’s trajectory. Several analysts have drawn parallels between Cava’s unit economics and margins and those of Chipotle, suggesting Cava could mature into a similarly profitable enterprise as it grows.

It’s not all rosy for Cava’s stock, though. Skeptics point out that Chipotle is a proven entity with a 30-year track record, whereas Cava is still navigating the transition from niche regional player to national chain. Any misstep – a quarter of slowing comps, cost inflation, or difficulty expanding into new markets – could deflate Cava’s high-flying valuation. Cava’s own outlook has been somewhat conservative; in its latest guidance, the company maintained a measured growth plan rather than the kind of hyper-aggressive expansion some investors might crave. This prudence may temper short-term stock gains, but could build credibility if Cava consistently meets its targets. By contrast, Chipotle’s guidance for 2025 called for low-single-digit comparable sales growth and 315–345 new restaurant openings (about 8% unit growth) – ambitious yet reasonable goals for a company of its size. Chipotle’s stability and cash generation make it attractive to long-term investors, even if its days of 20%-plus annual growth are in the past. As Nasdaq’s analysis put it, “Based on financial metrics, Chipotle has the better value, while Cava has more upside” potential as a growth stock.

Investor sentiment can also be gauged by the companies’ followings and leadership moves. Chipotle boasts a massive base of loyal customers and over 33 million loyalty program members as of mid-2024, which not only drives repeat business but also gives the company a deep well of consumer data. Cava’s Rewards program, while growing fast, had about 4.8 million members in the same period – impressive for a newer brand but a fraction of Chipotle’s reach. Cava’s executives argue that they are just scratching the surface of their addressable market; many Americans still haven’t tried Cava, which means plenty of runway if they can win over new converts. The stock market’s bulls seem willing to bet that Cava’s “growth monster” story has legs. The coming years will reveal whether Cava can justify the hype and convert high expectations into lasting shareholder value, or whether Chipotle’s seasoned, steady approach will continue to outshine the up-and-comer.

Beyond the balance sheet and stock tickers, Chipotle and Cava differ in how they operate and strategize for growth. Both are fast-casual concepts built on a similar template – a focused menu, an assembly-line service model for customized meals, and an emphasis on fresh ingredients – but they have taken distinct paths in scaling up.

Chipotle’s business model is famously straightforward: all its restaurants are company-owned, not franchised, ensuring tight control over quality and customer experience. From its start in 1993, Chipotle expanded organically, one burrito shop at a time (aside from a pivotal early investment from McDonald’s that provided growth capital in the early 2000s). The company has stayed largely single-brand focused; attempts at diversification like ShopHouse Southeast Asian Kitchen or Pizzeria Locale were limited experiments that Chipotle eventually shelved to refocus on the core brand.

This singular focus has paid dividends – Chipotle built a robust supply chain and cultivated a reputation for “food with integrity,” sourcing responsibly and preparing food without artificial additives. Over the years Chipotle has also been a pioneer in digital ordering and loyalty. Its mobile app and online ordering system are highly evolved, contributing 35–40% of revenue in recent quarters. Chipotle has introduced “Chipotlane” drive-thru pickup lanes at many new stores for digital order convenience, marrying tech with real estate strategy to boost throughput. And while many restaurant chains turned to franchising for rapid expansion, Chipotle proved it could scale to nearly 4,000 locations under a corporate model – maintaining consistency at the cost of slower expansion than a franchise-fueled approach might allow.

Cava’s model, in some ways, emulates Chipotle’s (no coincidence, as analysts often note). Cava also owns and operates all its restaurants with no franchising, and it similarly emphasizes fresh, customizable offerings – in Cava’s case, build-your-own salads, grain bowls, and pitas with Mediterranean ingredients like hummus, harissa, falafel, and tzatziki. But Cava’s strategic journey has a twist: rather than grow purely store-by-store, Cava leapfrogged its footprint by acquiring a competitor. In 2018, Cava Group purchased Zoës Kitchen, a larger Mediterranean chain with over 250 locations, in a $300 million deal. Over the next few years, Cava converted those Zoës Kitchen eateries into Cava-branded restaurants, instantly expanding its geographic reach beyond its East Coast stronghold.

By the time the last Zoës was converted in 2023, Cava had cemented itself as the largest player in U.S. Mediterranean fast-casual dining. This acquisition-driven growth spurt contrasts with Chipotle’s entirely organic expansion. The benefit for Cava was rapid scale and entry into new markets; the challenge was ensuring those converted stores achieved the same sales volumes as legacy Cava locations. So far, it appears to be working: Cava’s average unit volume (AUV) hit roughly $2.9 million in 2025, up from ~$2.6M a year prior, and CEO Brett Schulman noted that “Cava’s AUV is over $2.6 million in every region” where it operates – indicating strong consumer reception even in new markets. Chipotle’s AUV, for comparison, is in a similar ballpark (around $2.8–$3.0 million), which is remarkable given Chipotle’s broader ubiquity. Essentially, Cava’s restaurants are already generating volumes on par with Chipotle’s average, suggesting the concept travels well.

Another strategic difference lies in menu and innovation. Chipotle has famously kept a focused menu – burritos, bowls, tacos, and salads with a limited set of proteins and toppings – and introduces new items sparingly. When it does, it tends to be a big deal (e.g. a limited-time brisket offering in 2021 drove a bump in transactions). Cava, on the other hand, leans into culinary innovation to fuel buzz. The company frequently rolls out seasonal bowls or new toppings (for example, spicy lamb meatballs or roasted vegetables), and even product extensions like Cava-branded pita chips that became a viral hit. This constant refreshing of the menu keeps customers intrigued and gives Cava material for social media promotion – an important tactic when building brand awareness from a smaller base. Additionally, Cava has a consumer packaged goods (CPG) arm: it sells its proprietary dips and spreads (like hummus, tzatziki, harissa sauce) in grocery stores nationwide.

This not only provides a bit of extra revenue, but it serves as advertising – a shopper might discover Cava’s garlic hummus in Whole Foods and later decide to visit a Cava restaurant. Chipotle has dabbled in retail (limited edition hot sauces or apparel) but not to the extent of maintaining a grocery product line.

From an operations standpoint, both companies prioritize efficiency and customer experience, but their current focuses differ slightly. Chipotle is investing heavily in automation and throughput – testing kitchen robots for prepping avocados and lightening the load on staff, for instance – and doubling down on drive-thru pick-up lanes to increase convenience. Chipotle’s strategy also includes a push into new international markets (with restaurants now open in Canada, the U.K., France, Germany and more) and a long-term goal of 7,000 locations in North America, which implies decades more growth.

Lastly, there’s the question of pricing and value strategy. Chipotle has not been shy about raising prices when needed – it hiked menu prices in 2022 and 2024 to offset wage increases and commodity inflation. Its strong brand helped it do so without losing too many customers, though the recent dip in transactions shows there are limits. Cava, in contrast, has used price very strategically. By keeping its price increases modest (below the rate of inflation), Cava positioned itself as a relative “value” in the healthy fast-casual space. This may have helped it steal traffic from pricier rivals or from customers feeling budget-conscious.

It’s a delicate balance: Cava’s food is not cheap, but management clearly believes that maintaining a few dollars advantage in price vs. something like a Sweetgreen salad bowl helps bring in cost-sensitive diners. Over time, as Cava grows and gains pricing power, it may follow Chipotle’s playbook of gradually upping menu prices to bolster margins – but doing so without alienating customers will be key. In essence, Chipotle can lean on its iconic status to command premium prices, whereas Cava still has to prove its value to each new customer.

Chipotle’s lead over Cava is perhaps most obvious when looking at their footprints. Chipotle operates nearly 3,800 restaurants as of Q1 2025, spread across the United States and eight other countries. Cava, by comparison, has 382 locations as of the same date – about one-tenth the number of Chipotle units – and all of them are in the U.S. (in 26 states plus Washington, D.C.). In other words, Chipotle is everywhere from California to Kuwait, while Cava is still introducing itself to many U.S. regions and has no international presence yet.

Despite the disparity in current scale, Cava is expanding its footprint at a much faster rate. In the first quarter of 2025 alone, Cava opened 15 new restaurants (net), a roughly 4% expansion of its base in just three months. Over the past year, Cava’s unit count is up 18%i. Chipotle opened 57 new restaurants in Q1 2025, which is impressive in absolute number – it added more stores in one quarter than Cava did in a year – but for Chipotle that represents about a 1.5% increase on its much larger base. For full-year plans, Chipotle is targeting ~8–9% unit growth (315–345 new stores in 2025), while Cava originally planned ~15% unit growth in 2024 and has slightly bumped that higher for 2025. In fact, after a strong Q1, Cava raised its openings guidance for 2025 to 64–68 new restaurants (from an initial 62–66).

This will push Cava’s expansion rate near 18% for the year – extraordinary growth, albeit from a smaller base. Cava’s development strategy has been to deepen presence in markets it knows well (such as the East Coast and Texas, inherited from Zoës), while carefully entering new cities. In 2025, Cava has made debut entries into Indianapolis and South Florida, with plans to launch in Detroit and Pittsburgh later in the year. Each new market is a test of how well Cava’s concept resonates outside its core regions. Early signs are encouraging: “The entire cohort of restaurants opened in 2025 is outpacing our expectations,” CFO Tolivar noted. Moreover, brand awareness is spreading – in new markets, an estimated 20–30% of consumers now recognize the Cava brand upon entry, roughly double the awareness level from around the time of the IPO. Greater national visibility (helped by social media buzz around Cava’s menu and a successful IPO raising its profile) should make each successive market launch a bit easier.

Chipotle’s expansion, while slower percentage-wise, is relentless and increasingly international. Having saturated many U.S. metro areas (Chipotle has over 200 locations just in California, for example), the company is moving into smaller towns and aiming to infill suburbs with its Chipotlanes. International growth is still in early innings but being pursued with focus – Chipotle is in Canada and Europe with company-owned stores, and interestingly has licensed a few units in the Middle East (e.g. the first Chipotle in Dubai opened in 2021). Management has declared an ambition to eventually reach 7,000 restaurants in North America alone, almost double its current count, indicating at least a decade more of expansion domestically. That suggests Chipotle sees plenty of demand still untapped, perhaps through penetrating more rural areas or doubling up in dense markets. Cava’s long-term potential store count is not publicly quantified yet, but some analysts project it could be 1,000+ locations if Mediterranean cuisine achieves mainstream popularity akin to Mexican fare. For now, Cava’s focus is the U.S., where it has a wide runway – eventually, international markets could be an opportunity (Mediterranean flavors are broadly appreciated globally), but likely not until the U.S. business is well-established nationwide.

Geographic footprint also impacts each brand’s risk and opportunity. Chipotle’s broad distribution insulates it from regional economic swings – strength in Texas can offset softness in New York, for instance. Cava is more regionally concentrated (with a strong presence around the East Coast and mid-Atlantic, due to its D.C. roots). This concentration means Cava is somewhat more exposed to local economic or demographic shifts. Analysts have noted that Cava’s heavy presence around Washington, D.C., could be a risk if that area’s economy weakens or if key customer segments (e.g. government employees) pull back spending. The flip side is that as Cava expands to the Midwest, West Coast, and South, it diversifies its base and reduces that regional risk. Each new state Cava enters – such as recent moves into Indiana and Florida – not only adds revenue but also serves as a proof point that Cava isn’t just a coastal fad.

In terms of real estate strategy, both companies are zeroing in on drive-thru/digital-friendly formats for new stores. Over 80% of Chipotle’s new units in 2025 will feature Chipotlanes (drive-thru pickup lanes), which have been shown to boost sales and margins by capturing more suburban family business and commuter traffic. Cava, too, has experimented with drive-thru pickup windows and “digital kitchens” dedicated to fulfilling app orders, recognizing the importance of off-premise dining.

Approximately 38% of Cava’s revenue now comes from digital channels (app, web, delivery), actually slightly higher than Chipotle’s 35% digital mix. This underscores how tech-savvy and convenience-oriented both brands’ customer bases are. The growth of digital sales has made it easier for these chains to enter new markets with less advertising – a strong app and loyalty program can induce trial from tech-enabled diners who spot a new location on their feed.

It’s clear that Chipotle holds the high ground in this matchup: a far larger revenue base, higher absolute profits, a ubiquitous presence, and a proven model. Chipotle’s decades-long head start means it enjoys economies of scale in food procurement, technology, and advertising that Cava cannot yet match. For example, Chipotle’s massive purchasing volume for ingredients like chicken and avocados gives it cost advantages (and priority with suppliers) that likely contribute to its superior margins. Its established supply chain and store network also allow Chipotle to be more resilient – it can shift resources around if one region is underperforming or if there’s a food sourcing issue, minimizing system-wide impact. Cava, with a much smaller system, is inherently more vulnerable to disruptions or regional slowdowns. Additionally, Chipotle’s brand is deeply embedded in popular culture; it’s practically synonymous with fast-casual dining. Cava, while trendy, is still building its brand recognition and convincing consumers that Mediterranean bowls deserve as much love (and lunch money) as burrito bowls.

Another factor behind Chipotle’s lead is operational experience. Chipotle navigated growth pains in the past – most notably the food safety crises of 2015, which caused a steep sales decline and forced the chain to overhaul its safety standards. Painful as that episode was, Chipotle emerged stronger and with invaluable lessons in crisis management. Cava has not yet been truly tested by a major controversy or operational crisis on that scale. As Cava grows, it will need to maintain strict food safety and consistency; any slip-up could erode the consumer trust it’s working hard to build. Moreover, scaling from 300+ to thousands of units requires robust systems for hiring, training, and culture. Chipotle benefits from a well-oiled corporate infrastructure and tens of thousands of crew members who know the routines. Cava, at ~11,000 employees, is growing that workforce rapidly – it must ensure the “Cava culture” scales with it, so that service quality and hospitality don’t lag. CEO Schulman often emphasizes “heart, health, and humanity” as core values for Cava, hinting at the importance of culture. Whether those values can remain consistent across hundreds (eventually thousands) of outlets will be a key determinant of Cava’s long-term success.

From a strategic viewpoint, Cava’s biggest challenge is execution: it needs to continue delivering high growth sustainably. Investors are expecting Cava to post strong comps and open new stores briskly for years to come. That means avoiding the pitfalls that have tripped up other fast-casual upstarts (for instance, some analysts recall how salad chain Sweetgreen’s rapid expansion led to widening losses and volatility). Encouragingly, Cava is already profitable and generating positive cash flow, which gives it more leeway to invest in growth from its own coffers. But to truly catch up to Chipotle in scale, Cava might have to consider bold moves – perhaps exploring international markets, launching smaller format stores, or even M&A (acquiring another concept to fuel expansion) down the line. Each of those steps comes with risk. Expanding abroad, for instance, would pit Cava against local tastes and established competitors without the brand recognition it enjoys in the U.S. For now, management appears rightly focused on the domestic opportunity.

Meanwhile, Chipotle is not standing still. Though it is the incumbent, Chipotle still behaves in many ways like a growth company: opening new locations at a steady clip, experimenting with menu items (e.g. plant-based chorizo trials, brisket, cauliflower rice), and leveraging its sizable budget for marketing and tech upgrades. This means Cava is chasing a moving target. If Mediterranean bowls start stealing significant share from burrito bowls, Chipotle could respond with promotions or simply by accelerating its own growth to crowd out competitors. The fast-casual sector is intensely competitive – not just between cuisines, but within them. Chipotle’s primary competitors historically were other Mexican chains and big fast-food names; now it must fend off everything from salad concepts to poké bowl shops to, yes, Mediterranean upstarts. The good news for both Chipotle and Cava is that consumers continue to seek convenient, healthier dining options, and there’s overlap in their customer bases. It’s not uncommon for the same person to grab Chipotle for lunch one day and Cava the next, viewing both as satisfying alternatives to burgers or pizza. In that sense, Cava’s rise doesn’t necessarily come at Chipotle’s expense – the market for fast-casual food may be expanding enough to lift both. But in terms of vying for investor capital and press accolades, the two will be compared side-by-side for the foreseeable future.

Chipotle’s dominance in revenue, profit, and footprint underscores why it is still far ahead of Cava in the fast-casual big leagues. With nearly 4,000 restaurants and decades of brand-building, Chipotle enjoys advantages of scale and a loyal following that are hard to beat. It consistently delivers solid financial results and has proven its resilience through various challenges. Cava, on the other hand, represents the next generation – a fast-growing contender with a fresh spin on healthy, flavorful dining. Cava’s explosive sales growth, improving margins, and successful IPO have put it on the map as Chipotle’s most credible rival in the fast-casual space. It has shown that Mediterranean cuisine can achieve broad appeal in America, and its strategy of steady expansion and menu innovation is yielding results.

Still, the road to truly catching up with Chipotle is long. Cava must navigate the complexities of scaling up: maintaining quality and culture, sustaining its growth rates, and eventually expanding beyond its current geography. Investors are optimistic – perhaps even a bit idealistic – about Cava’s “Chipotle-like” trajectory, as seen in its rich stock valuation and bullish analyst coverage. For readers and potential investors, the key takeaway is that Chipotle offers proven performance and stability, whereas Cava offers high growth potential with corresponding risks. In the coming years, we will likely see Cava inch closer to Chipotle’s level on some metrics (such as unit economics and brand reach), but Chipotle isn’t yielding any ground easily. If anything, Chipotle’s own expansion and innovations may widen the gap unless Cava executes near-flawlessly.

In summary, Chipotle is ahead because of its scale, experience, and strong margins, while Cava’s youth means it has agility and room to grow, but also challenges to overcome. The fast-casual crown is Chipotle’s to lose, but Cava has the opportunity to carve out a significant place in the landscape if it continues on its current path. For consumers, it’s a win-win: two vibrant brands elevating quick-serve dining in different ways. For these companies’ shareholders, it will be fascinating to watch whether Cava can fulfill its promise and one day approach Chipotle’s heights – or whether Chipotle will simply outdistance the field as it expands its empire.

Join LevelFields now to be the first to know about events that affect stock prices and uncover unique investment opportunities. Choose from events, view price reactions, and set event alerts with our AI-powered platform. Don't miss out on daily opportunities from 6,300 companies monitored 24/7. Act on facts, not opinions, and let LevelFields help you become a better investor.

AI scans for events proven to impact stock prices, so you don't have to.

LEARN MORE