Inflation, taxes, and health care are key risks—but disciplined investing keeps a $5M nest egg secure for decades.

Sectors & Industries

October 21, 2025

Table of Contents

Retiring with a nest egg of $5 million puts you well above the average retiree and can in most cases fund a very comfortable retirement. Whether $5 million is “enough” depends on when you retire, how much you spend annually, your lifestyle expectations, and factors like inflation, healthcare costs, and longevity. This report evaluates multiple scenarios – retiring at ages 55, 60, and 65 – and compares modest vs. luxurious spending levels. We also examine how long $5 million could last under different assumptions and how location (high-cost states like California/New York vs. lower-cost states like Texas/Florida) affects retirement comfort. All findings use current 2025 data from credible financial sources.

Exiting the workforce at 55 means planning for a potentially long retirement (30–40+ years). The good news is that $5 million is generally more than sufficient to retire early at 55. Even with no investment growth at all, $5 million could fund about $100,000 per year for 50 years (simply $5,000,000 ÷ 50 years). In reality, a well-invested portfolio should continue to grow in retirement, so withdrawing $100K annually (2% of $5M) is very conservative – likely preserving or even growing the principal. Financial advisors often cite the “4% rule” as a benchmark for 30-year retirement sustainability; under that rule, $5M could support an initial withdrawal of $200,000 per year (4% of $5M), adjusted for inflation thereafter. However, retiring at 55 may warrant a more cautious withdrawal rate (closer to 3%–4%) to account for a longer time horizon. For example, withdrawing $125,000 per year (2.5% of $5M) with no investment growth would stretch the funds 40 years, whereas $200,000 (4%) would exhaust $5M in 25 years if there were truly no growth. In practice, moderate growth can substantially extend these timelines.

Early retirees must bridge gaps in Social Security and Medicare. You cannot claim Social Security at 55 (the earliest is 62), but with $5M “you probably won’t be depending on it” anyway. Medicare health coverage also isn’t available until 65, so an early retiree needs to budget for private health insurance for a decade. Those costs can be high – potentially $10,000+ per year for a 55–64 year-old – and should be factored into the annual spending plan. Despite these challenges, $5 million can allow retirement at 55 virtually anywhere in the country. Even in expensive regions, a $5M portfolio can generate over $100K of annual income with prudent investing, which “should be more than enough to live comfortably on starting at age 55”. The key is to manage spending and withdrawals so the nest egg lasts 40+ years. (We will later discuss strategies like using investment income to avoid drawing down principal too quickly.)

At 60, a $5M nest egg remains more than sufficient for a comfortable retirement for most households. By age 60, the retirement horizon is a bit shorter (possibly 25–35 years), improving the odds that $5M will last. In fact, based on median U.S. cost of living, $5 million is more than enough to retire comfortably at 60 – it “can support many households for decades or more”. Using the 4% guideline, $5M can still provide ~$200K/year initial income, well above what most retirees spend. However, lifestyle choices matter. If you intend to maintain a very high-cost lifestyle – say, keeping a large expensive home, extensive travel, or financially supporting adult children – you might consume more than the typical household and should plan withdrawals accordingly. In extreme cases of lavish spending, $5M could be strained; but for an “average” to upscale lifestyle, it’s ample.

One advantage at 60 is being closer to Social Security (eligible at 62, full benefits by ~67) and Medicare (eligible at 65). But there is still a 5-year healthcare gap to bridge: you’ll likely lose employer health insurance at retirement, and must fund private insurance or COBRA until Medicare kicks in at 65. This can add a significant cost. For instance, Fidelity Investments estimates that an average 65-year-old retiring in 2024 will spend about $165,000 on healthcare in retirement (out-of-pocket for Medicare premiums, co-pays, etc.). If you retire at 60 instead, that figure could be higher to account for additional years of coverage before Medicare. It’s wise to set aside a portion of the $5M for these medical costs. Another consideration is long-term care planning: wealthy retirees won’t qualify for Medicaid, so one might use part of the portfolio for long-term care insurance or reserve funds for nursing care (which can cost $70K–$100K per year in later life). $5M affords the flexibility to plan for such expenses.

Despite these costs, $5M at 60 can easily sustain a well-off retirement. To illustrate the income potential of $5M: if invested in a conservative instrument like U.S. Treasurys yielding ~3.5%, it could generate $175,000 per year in interest alone without touching principal. Many retirees will use a balanced portfolio – e.g. a mix of stocks and bonds – which historically might yield on the order of 6–8% annually. Even a simple high-yield savings account around 4% APY would produce $200K/year on $5M. In other words, at age 60 you could feasibly live off the investment returns and preserve much of the $5M for decades. For example, one could annuitize $5M – converting it to a lifetime income stream. A 60-year-old purchasing a single-life annuity with $5M might receive on the order of $27,000 per month (≈$332,000 per year) guaranteed for life. That is an extremely comfortable income (though annuitizing would forfeit the principal in exchange for that guarantee). Alternatively, investing in an S&P 500 index fund (historically ~10% annual returns) could theoretically produce ~$500K in returns in a good year on $5M (though with high volatility). The bottom line at 60 is that $5 million can generate far more income than most retirees live on – the median household income for 65+ in 2023 was about $54,700, and $5M can easily produce several times that each year. The main question is making sure your spending needs (drawn from the portfolio) are aligned with a sustainable strategy so the money lasts your lifetime.

Age 65 is a traditional retirement age and, unsurprisingly, $5M by 65 is typically more than enough to retire very comfortably. At 65, you have immediate access to Medicare, and the planning horizon (life expectancy) might be ~20–30 years. If you have $5 million at 65, it should be more than enough to retire, provided you manage it according to your health, lifestyle, and spending habits. In fact, many Americans retire with far less. Again using the 4% rule as a yardstick: $5M can yield ~$200K/year of inflation-adjusted income for 30 years with high success probability. Most retirees do not need anywhere near $200K annually – a common guideline is that you might require ~80% of your pre-retirement income to maintain the same standard of living. So if you earned, say, $150K/year before, you might target ~$120K/year spending in retirement. $5M can easily support that level (120K is only a 2.4% withdrawal).

Where $5M at 65 might fall short is if someone has very expensive goals – for example, maintaining multiple homes, continuous luxury travel, or leaving a large inheritance (which means living on even less of the principal). But for almost any reasonable lifestyle, $5M provides a generous cushion. It allows for a balanced investment portfolio focused on capital preservation and income. A typical asset allocation at 65 might be roughly 40–50% in bonds/fixed income, 35–45% in equities (stocks), and the remainder in cash or alternative assets for diversification. With $5M, such a portfolio can be structured to produce significant current income (through interest and dividends) and moderate growth to beat inflation. For instance, a mix of investment-grade bonds, dividend stocks, and REITs could yield a few percent in income per year, reducing how much principal you need to withdraw.

At 65, you can also draw Social Security if you haven’t already. While Social Security benefits are a “nice bonus”, a $5M-retiree will find that those benefits are a relatively small portion of their income. Nonetheless, every bit helps with longevity. More importantly, healthcare costs will rise with age – even with Medicare. Premiums for Medicare Part B, Part D, and any supplemental plans, plus copays and services not covered by Medicare, must be budgeted. As noted, a single 65-year-old might expect $165K in healthcare expenses over their retirement (and that’s before considering long-term care). With $5M, covering these costs is very feasible, but they underscore the need to allocate funds for medical needs. Don’t overlook long-term care in particular – the likelihood of needing some assisted living or nursing care increases in your 80s or 90s. Typical nursing home costs can exceed $100,000 per year, so many advisors suggest earmarking a portion of savings or insurance for that possibility. Fortunately, a $5M portfolio can absorb even these large expenses if planned for (for example, by keeping a cash reserve or dedicated investment for potential long-term care). Overall, at age 65 a $5 million nest egg provides a comfortable margin: it can fund a very comfortable lifestyle and has the capacity to handle surprises like medical or dental bills, home repairs, or helping family, as long as withdrawals are kept within a sustainable range.

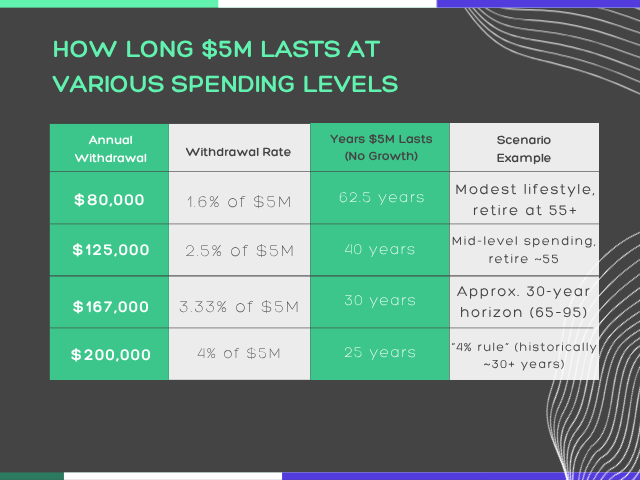

In all three scenarios – retiring at 55, 60, or 65 – a $5,000,000 portfolio can provide a comfortable retirement income. The earlier you retire, the longer the money needs to last, so early retirees should plan on somewhat lower initial withdrawal rates to avoid outliving their savings. Conversely, retiring later shortens the distribution period, allowing for higher withdrawals or more legacy leftover. The table below summarizes how long $5M could last under different withdrawal scenarios, to highlight the impact of retirement age and spending level:

Table: How long $5M lasts at various spending levels (assuming zero real growth). In practice, even moderate investment returns can extend these durations. A 4% initial withdrawal ($200K) has a high probability of lasting 30 years or more when invested in a balanced portfolio, while very low withdrawals (1–2%) could potentially allow the principal to last indefinitely or even grow.

Lifestyle expectations play a huge role in determining if $5 million is “enough” for you. Annual spending in retirement can range widely – one retiree might live modestly on $60–$80K per year, while another spends $200K+ on luxury travel and fine dining. Let’s consider three broad lifestyle levels:

With $5,000,000 saved, even the high end of these budgets is within reach, but the sustainability and trade-offs differ:

This level of spending is easily supported by a $5M portfolio. $80K is just a 1.6% withdrawal rate, which is extremely low – likely the portfolio will continue to grow because typical investment returns will exceed 1.6%. For context, a 3–4% withdrawal is often considered “safe” for long-term retirement. At 1.6%, $5M could theoretically support 60+ years of withdrawals even with no portfolio growth. In practical terms, $80K/year is above the U.S. median household income and can afford a comfortable life in most areas. On that budget, one might have a paid-off home, travel occasionally, and cover all necessities with room for leisure.

If investing the $5M in ultra-safe assets, even a 3.5% bond yield would generate ~$175K interest, far exceeding an $80K need. So at a modest spending level, $5M is more than enough – your money should last not only your lifetime but potentially leave a substantial legacy. In fact, the risk here might be being too conservative and underspending; many with such wealth find they can increase their lifestyle or gifting and still not dent the principal much.

This range equates to withdrawing ~2.5%–3% of $5M annually. Most financial planners would consider that a very sustainable withdrawal rate. At 3% ($150K/year), the 30-year survival odds of the portfolio are excellent – historically, a 3% inflation-adjusted withdrawal had a near-100% success rate for 30+ year retirements in the Trinity study data. Even if markets underperform, 3% leaves room for adjustment. With moderate investment growth (say 5% average returns), a 3% draw would allow the principal to keep pace with inflation or only slowly decline.

A $120K–$150K budget affords an upscale life: for example, $10K a month could cover an expensive mortgage or property taxes, two cars, travel, hobbies, and healthcare with ease in most regions. Day-to-day comfort would not be an issue – recall that the median retiree household spends under $60K/year, so $120K+ is roughly double the typical retiree spending. At this spending level, $5M should last well beyond 30 years absent catastrophic economic events. To be prudent, one would still monitor investments and possibly dial back spending if the portfolio hits a rough patch early (sequence-of-returns risk), but overall, $5M can comfortably fund $150K/year for life in most scenarios. Many advisors would even say you’re underspending relative to what $5M could potentially allow.

$200,000 per year is a high-end retirement lifestyle – $16,667 per month is far above what even affluent retirees usually spend. This level might include luxury travel, vacation homes, costly hobbies (yachting, country club memberships, etc.), and generous gifting. $200K is a 4% withdrawal rate from $5M, hitting that classic rule-of-thumb threshold. Historically, the 4% rule suggests a high likelihood that $5M could sustain $200K (inflation-adjusted) for at least 30 years. In fact, 4% was based on worst-case market sequences – many times the portfolio lasts much longer or even grows. However, 4% is not foolproof, especially if markets underperform or if you expect to live significantly more than 30 years. For example, a 65-year-old has a decent chance of living 30 years (to 95) – 4% should cover that. But a 55-year-old planning for 40+ years might want to be a bit under 4% to be safe (maybe 3.5%–3.8% initial). It’s also important to note that large annual spending may not be uniform every single year – you might spend more in the early “active” retirement years (on travel and lifestyle) and less later if you slow down.

Very late in life healthcare or long-term care can spike expenses again. With $5M, drawing $200K still leaves a big cushion for such spikes, but it means you are more reliant on investment growth to replenish what you withdraw. If your portfolio averages ~4% real returns, you’ll roughly maintain your purchasing power at a 4% withdrawal. If returns fall below that, you’d gradually erode principal. In practice, many retirees adjust spending dynamically – e.g. trimming the budget after market downturns – to ensure the nest egg endures. Bottom line: $200K/year is generally sustainable on $5M, but it’s near the upper limit for a lifetime payout. If you truly wanted to spend beyond $200K (say $250K or $300K yearly), then $5M might eventually be depleted unless you have extraordinary investment gains.

One should also consider inflation in lifestyle planning. All the withdrawal figures above ($80K, $150K, $200K) are in today’s dollars. Over a long retirement, costs will rise. For example, at a modest 3% inflation, prices double in about 24 years. Historical data shows that from 2012 to 2022, expenses for 65+ households rose ~43% (due in part to inflation). So if you retire at 60 and start with a $150K budget, by age 84 you might need around $300K/year to have the same purchasing power, assuming inflation trends hold. The 4% rule accounts for inflation by upping withdrawals annually, but it was tested on past U.S. market performance. If future inflation is higher or market returns lower, adjustments might be needed.

The key point: plan for your spending to increase over time in nominal dollars, and ensure your investment strategy provides growth (through equities, for instance) to keep up. Retirees with $5M are actually in a good position to combat inflation – you have a large capital base that can be partially invested in assets that historically outpace inflation (stocks, real estate, TIPS, etc.). Many affluent retirees will even find their net worth keeps growing after retirement if they stick to a moderate withdrawal, effectively creating an ever larger buffer against longevity and inflation risk.

Inflation Risk: Inflation is the gradual erosion of purchasing power, and it’s a critical factor for a long retirement. Even moderate inflation can significantly reduce the real value of a fixed income over decades. For instance, $1 in 2012 was equivalent to about $1.31 by the end of 2022 due to cumulative inflation. In practical terms, what $100,000 bought a decade ago requires $131,000 today. If you retire around 2025 and live into the 2050s, you must anticipate that a comfortable $120K annual budget now might need perhaps $200K+ per year in later retirement just to maintain the same lifestyle. This is why retirees with substantial assets like $5M usually keep a healthy allocation to growth-oriented investments (e.g. equities) even in retirement. While bonds and fixed income provide stability and income, they might not keep pace with high inflation. Stocks, real estate, and other real assets historically generate returns above inflation over the long run, acting as an inflation hedge. For example, a diversified stock index has averaged ~10% per year historically (though future returns can vary), far outpacing inflation. Having a portion of $5M in equities means your portfolio’s value and the income it generates can grow over time, offsetting rising living costs.

From a planning perspective, using a lower initial withdrawal rate (like 3% instead of 4%) builds in more cushion for inflation. If inflation turns out higher, you have some wiggle room to absorb bigger cost-of-living adjustments. It’s also wise to include inflation-protected securities for essential expenses. Treasury Inflation-Protected Securities (TIPS) or inflation-indexed annuities, for instance, adjust payouts with inflation and can guarantee that a core part of your income keeps up with prices. Some retirees choose to front-load their retirement fun (traveling more in the early years) and assume they will naturally spend less later on – to some extent this can counteract inflation because discretionary spending might drop as one ages. However, one must be careful, as healthcare expenses often rise in very old age (a potentially inflationary component).

Longevity Risk: This is the risk of outliving your money – essentially, living longer than your financial plan expected. While everyone hopes for a long life, longevity risk means your savings might need to sustain not just an average lifespan but a potentially exceptional lifespan. For a 65-year-old couple today, there is a reasonable probability one spouse lives into their 90s. If you retire at 55, you might be looking at a 40-year retirement or more. With $5M, the longevity risk is mitigated by the sheer size of the portfolio, but it’s still crucial to manage withdrawals. The 4% rule was designed for ~30 years; if you need to plan for 40+ years, many experts suggest using a slightly lower withdrawal (maybe ~3.5% or less) to be safe. In our earlier table, note that a 2.5% rate ($125K/yr) could theoretically last 40 years even with zero growth – that’s a conservative target an early retiree might use, knowing the portfolio will likely earn something and thus last much longer.

For those highly concerned about longevity, annuities can be a useful tool. We mentioned that at age 60, $5M could buy an annuity paying over $330K per year for life. While most retirees wouldn’t annuitize everything, you could annuitize a portion of your $5M to cover essential expenses no matter how long you live. For example, putting $1M into an immediate annuity might give a 65-year-old on the order of $60K/year guaranteed for life (exact amount depends on interest rates and survivor options). That, combined with Social Security, can form a longevity-protected income floor for basics like housing, food, and healthcare. The rest of the portfolio can remain invested for growth and extra discretionary spending. Another approach to handle longevity is to use a “bucket strategy” – e.g., earmark certain amounts for different phases of retirement (active years, later years, etc.), or keep a reserve that you don’t touch until age 85+.

It’s also important to periodically review your plan as you age. If you reach 80 and have, say, $3M of the $5M left, you can likely increase your spending if desired (because the remaining years are fewer). Conversely, if markets performed poorly early on and by 70 you’ve used a large chunk, you may need to adjust down. Regular check-ins with a financial planner or using retirement planning software to simulate to age 95 or 100 can help ensure you won’t unexpectedly run out of money. Overall, $5 million provides a very large buffer against longevity risk – far more than most people have – but prudent withdrawal management and possibly insurance products can further ensure the money lasts no matter how long you live.

Healthcare is a major wildcard in retirement planning, and even a $5M portfolio can be dented by significant medical expenses if not anticipated. There are a few components to consider: regular healthcare premiums and out-of-pocket costs, and long-term care.

Once you reach 65, Medicare will cover a substantial portion of doctor and hospital bills, but it’s not free. In 2025, the standard Medicare Part B premium (medical insurance) is around $165–$170 per month, and most retirees also buy a Part D prescription plan and/or a supplemental “Medigap” or Medicare Advantage plan. Fidelity’s research estimates that an average 65-year-old retiring now will need about $165,000 in total to cover their healthcare expenses during retirement (for a single retiree). For a married couple, that would be roughly double (around $300K+). These figures include premiums, co-pays, and other out-of-pocket costs over the remaining lifetime. With a $5M fund, allocating $300K for a couple’s medical costs is very feasible – it represents only 6% of the portfolio. It’s wise to set aside or mentally account for this “healthcare bucket” so that these necessary costs don’t disrupt your lifestyle budget.

If you retire early (before 65), as discussed, you’ll need interim coverage. This could mean private insurance or marketplace plans which, at age 55–64, might cost anywhere from $8,000 to $15,000 per year per person for comprehensive coverage (varying by location and subsidies). Ten years of such premiums for a couple could easily be $150K. Again, $5M can handle it, but it’s a significant expense to plan for in the early retirement budget. Some early retirees opt for higher deductible plans and use savings for any big expenses, or they might bridge the gap with COBRA from a former employer for 18 months, etc. The key is not to overlook these costs – health insurance can be one of the largest expenses in your 50s/60s until Medicare eligibility.

Medicare at 65 greatly reduces costs but doesn’t eliminate them. You still pay premiums and things like dental, hearing, vision, and many long-term care needs are not covered by Medicare. It’s prudent with $5M to also consider self-insuring for certain health costs – for instance, having an emergency fund segment of the portfolio for unexpected medical procedures or experimental treatments that insurance won’t cover. In retirement, healthcare inflation has often been higher than general inflation, meaning the cost of medical services tends to rise faster. This is another reason your portfolio should maintain some growth assets – to outpace the high inflation in healthcare.

Long-Term Care (LTC): Long-term care refers to extended assistance with daily living activities due to chronic illness, disability, or cognitive impairment (e.g., Alzheimer’s). This can be provided at home with aides, in assisted living facilities, or in nursing homes. It is expensive and often not covered by Medicare (Medicare only covers brief rehabilitative stays, not custodial long-term care). Many retirees will eventually need some LTC – estimates suggest that over half of people over 65 will require some long-term care during their lifetimes, at least for a period. The costs in 2025 for long-term care services are substantial: a private room in a nursing home costs on the order of $10,000–$12,000 per month (national average ~$111,000 per year for a semi-private room) and assisted living facilities average around $70,000+ per year. Even in-home care can run $20–$30 per hour for home health aides, which adds up if daily care is needed.

For a high net-worth household with $5M, there are generally two ways to handle LTC risk:

Long-term care insurance premiums are quite high at older ages and insurers have tightened benefits. Still, some 55-65 year-olds with millions in assets use these policies to protect their estate/children’s inheritance from a worst-case LTC scenario. Others decide that with $5M, they can afford, say, a 3-year nursing home stay costing $300K without wiping out their finances. If married, one consideration is protecting the healthy spouse – you wouldn’t want one spouse’s prolonged care needs to impoverish the other. With $5M, that is less of a concern, but it could still significantly draw down the portfolio. For instance, if from age 85–90 you needed care at $100K/year, that’s $500K total – a sizable but manageable chunk of $5M (10%).

It’s recommended to plan for long-term care in advance: perhaps earmark $500K of the $5M in a conservative investment or trust as the “LTC fund.” If you never need expensive care, that money can go to heirs or be used for other purposes in your late 90s. If you do need it, you have it available. Another strategy is downsizing your home in old age and using home equity to fund care. Many retirees with expensive homes plan to sell the house and move to a care facility, effectively using the house value (which could be substantial in CA or NY) to cover those costs. Overall, healthcare and LTC are areas where high-cost surprises can occur, but a $5M portfolio has the capacity to absorb them with proper planning. As one advisor notes, for a high-net-worth retiree, Medicare will cover the bulk of standard healthcare after 65, but long-term care requires proactive planning since you likely won’t qualify for Medicaid. With $5M, you have the flexibility to choose high-quality care options when needed, which is a key aspect of retiring “comfortably.”

The cost of living varies dramatically across the United States. $5 million provides a comfortable retirement in virtually any state, but in high-cost areas your money will be consumed faster if you try to maintain the same lifestyle as in a low-cost area. Let’s compare what retirement might look like in a high-cost state like California or New York versus a lower-cost state like Texas or Florida.

A good starting point is the average expenses for a retired person by state. According to 2024 data, the most expensive states for retirees in terms of annual cost of living are Hawaii, California, New Jersey, New York, and Massachusetts. In California, an average retiree’s expenses are about $56,600 per year (roughly $4,716 per month). New York isn’t far behind, at around $52,200 per year for a retiree. By contrast, several Sunbelt and Southern states are much cheaper. Florida’s retiree cost of living is roughly $42,550 per year ($3,546 per month), and Texas’s is about $43,770 per year ($3,648 per month). Some states are even lower – e.g. West Virginia, Mississippi, and Arkansas have average retirement costs in the low-$30Ks annually.

What drives these differences? Housing is a major factor – in California or New York metro areas, housing (whether owning with property taxes or renting) is far more expensive than in Texas or Florida. Other costs like groceries, services, and taxes also play a role. The table below shows a monthly expense breakdown for California vs. Florida for a typical retiree:

.png)

Table: Average monthly retirement expenses in a high-cost state (California) vs. a lower-cost state (Florida). Housing and other costs are much higher in CA, resulting in about a 30% higher annual budget needed for the same lifestyle. Data source: 2024 analysis of BLS and Census data.

From the above, a retiree in California spends ~$14,000 more per year than a retiree in Florida for the same basket of goods and services. That’s a 33% increase. If you as a $5M retiree plan to live in a high-cost city (e.g. San Francisco, New York City), you should anticipate needing a higher annual withdrawal for a given lifestyle. For example, if you desire a comfortable middle-class retirement lifestyle that costs $100,000/year in Florida, that same lifestyle might cost on the order of $130,000/year in coastal California when you factor in housing and taxes. Fortunately, $5M can cover either case; the difference is that in California you’d withdraw a larger chunk of your portfolio each year. Over 20–30 years, that extra ~$30K/year could sum to an additional $600K–$900K drawn from the portfolio.

State and Local Taxes: Another crucial aspect is taxes, which vary by location. Some states have no state income tax – notably Florida, Texas, Nevada, Tennessee, and a few others – which is very favorable for retirees drawing income from investments. Other states fully tax retirement income (like 401k withdrawals, pension income, etc.) at their normal rates. California, for instance, has a state income tax ranging from 1% up to 13.3% on high incomes (the top rate would apply if your taxable income is in the millions, but even $200K withdrawals would fall in a high bracket around 9–10%). New York State (and City) also impose high taxes. On the other hand, Texas and Florida impose 0% state income tax on retirement income. This means if you withdraw, say, $200K from your IRA or investments in Florida, you pay no state tax – whereas in California that same $200K might incur around $20K of state tax. Over decades, living in a high-tax state can chip away at your funds or require a higher gross withdrawal to net the same spending money. High property and sales taxes in some areas also increase cost of living for homeowners and consumers.

Lifestyle differences by location: Beyond raw cost numbers, consider what “comfortable” means in each place. In a high-cost city, $100K/year might feel just adequate – e.g., $4K/month for rent or home costs, $2K for other living expenses, $2K for travel/entertainment, etc. In a low-cost area, $100K could afford a larger home, more travel, or simply result in more surplus each month. Many retirees from expensive regions choose to relocate specifically to stretch their retirement dollars (a practice sometimes called geoarbitrage). With $5M, relocation isn’t necessary to afford retirement, but it might allow for a more lavish lifestyle or preserve more of your principal. For instance, a retiree with $5M in California might need to be somewhat “careful” with a $150K budget (given high housing costs), whereas the same person in Texas or Florida could likely spend less and invest more of their money, or conversely afford a higher standard of discretionary spending for the same budget.

It’s also worth noting that quality of life factors come into play. High-cost areas often have higher-priced entertainment, dining, and activities – if those are important to you, you’ll spend more. However, they may also offer amenities (cultural institutions, accessible healthcare facilities, etc.) that some retirees value. Low-cost states might trade off some conveniences (e.g., you might drive more, or have fewer high-end restaurants) but offer savings. Personal preferences will dictate where you want to live, but from a purely financial lens, $5M will go further in a low-cost state. As one analysis pointed out, states like Texas, Florida, and Arizona are roughly in the middle for retiree costs (only ~0–10% above the national average), whereas New York, California, Massachusetts are ~20–30% above average. Over a long retirement, that difference can add up – potentially requiring hundreds of thousands more from your portfolio if you stay in a pricey area.

For example, imagine a 30-year retirement in which living in California costs you an extra $15K/year compared to a cheaper state. Over 30 years, that’s $450,000 more withdrawn (not even counting investment opportunity cost on that money). $5M certainly can handle that, but it might mean the difference between ending retirement with $3M left versus $2.5M left. Some high-net-worth retirees solve this by becoming “snowbirds” – spending half the year in a low-cost state or tax-free state (or even abroad in a low-cost country) to reduce expenses, while still enjoying part of the year in a preferred high-cost location. Even spending 6+ months in Florida can establish residency for tax purposes, eliminating state income tax on withdrawals, which is a strategy used by many affluent New Yorkers and Californians in retirement.

In summary, $5M gives you the freedom to retire in a high-cost state if that’s where you want to be – you can afford it. The SmartAsset analysis we cited earlier notes that with $5M “you can plan on retiring almost anywhere” in comfort. Just be mindful that in extremely high-cost cities you’ll spend more for the same lifestyle, so you may need to “be more careful with your money” or accept a higher burn rate on your portfolio. If maximizing the longevity of your $5M or the surplus you leave behind is a priority, choosing a more tax-friendly, lower-cost area will certainly help. On the other hand, if living in (say) San Francisco or Manhattan is a key part of your dream retirement, $5M can make it happen – you just might use up more of your funds enjoying the perks of those locales. The good news is that in any average U.S. location, $5M is well above what’s needed for comfort: many states only require ~$1–2 million in lifetime savings to support an average retirement lifestyle, so $5M is several times that benchmark. Whether you are in California or Texas, $5M puts you in an elite category of retirees and affords a lot of flexibility.

Taking into account all the above factors – age, spending, inflation, healthcare, and location – how long will $5 million actually last in retirement? The answer is: likely for the rest of your life, and potentially with money left over, if managed prudently. Here’s a recap of key points on longevity of the $5M portfolio under different conditions:

With $5 million, the biggest risks aren’t just market averages—they’re events that can change the risk/return calculus on specific holdings: CEO exits, FDA rulings, billion-dollar contracts, guidance cuts, credit downgrades, buybacks, activist campaigns, and more. That’s where LevelFields AI is useful alongside your core retirement plan.

What LevelFields does

Why it pairs well with a $5M retirement plan

Human-plus-AI workflow

Quick example: You hold a defense contractor for dividend income. LevelFields flags a newly awarded multi-year DoD contract and shows how similar awards historically affected price and volatility. With your advisor, you might (a) hold for growth, (b) write a covered call to boost income, or (c) rebalance if the position’s weight jumped.

In conclusion, $5 million is generally enough to retire very comfortably in the United States, across a variety of scenarios. It can fund a luxurious standard of living in most places, or an extremely lavish one in more affordable places. The wealth level is high enough to withstand market fluctuations, provide for rising costs, and cover unforeseen expenses like medical needs, as long as prudent financial practices (diversification, reasonable withdrawal rates, periodic plan reviews) are in place. Whether retiring at 55, 60, or 65, $5M can be structured to last your lifetime – even if you live to 95 or 100 – particularly by following a sustainable withdrawal strategy (around 3–4% initial rate, with adjustments). High inflation or high spending can shorten the longevity of the portfolio, but with $5M you have considerable buffer to adjust and still not run out of money.

Finally, consider consulting with a financial advisor to tailor a plan to your exact situation. They can run Monte Carlo simulations using your desired retirement age, spending level, asset allocation, and location to quantify the probability of $5M lasting to age 90, 95, 100, etc. Most likely, the probability will be very high. As one financial expert put it, with $5M “the only question is how much you plan on spending or what lifestyle you’d like post-retirement” – the money itself is sufficient as long as you align your spending with your goals and invest for the long run. In other words, $5 million can absolutely buy a comfortable retirement in America, and with wise management, you’ll have both financial security and peace of mind for the decades ahead.

Join LevelFields now to be the first to know about events that affect stock prices and uncover unique investment opportunities. Choose from events, view price reactions, and set event alerts with our AI-powered platform. Don't miss out on daily opportunities from 6,300 companies monitored 24/7. Act on facts, not opinions, and let LevelFields help you become a better investor.

AI scans for events proven to impact stock prices, so you don't have to.

LEARN MORE