U.S. stocks gained in early August as Fed shifts, tariff updates, and big-tech capex drove market resilience.

Sectors & Industries

August 11, 2025

Table of Contents

The first full week of August was shaped by political maneuvering, shifting trade positions, and selective sector strength. Equities ended broadly higher, with tech, communications, and financials leading while defensive sectors underperformed. The S&P 500 gained 0.8% and the Nasdaq rose nearly 1%, supported by solid earnings from companies including Motorola Solutions, Akamai, and Block. The tone reflected a mix of optimism over potential rate cuts and caution over ongoing trade and geopolitical uncertainty.

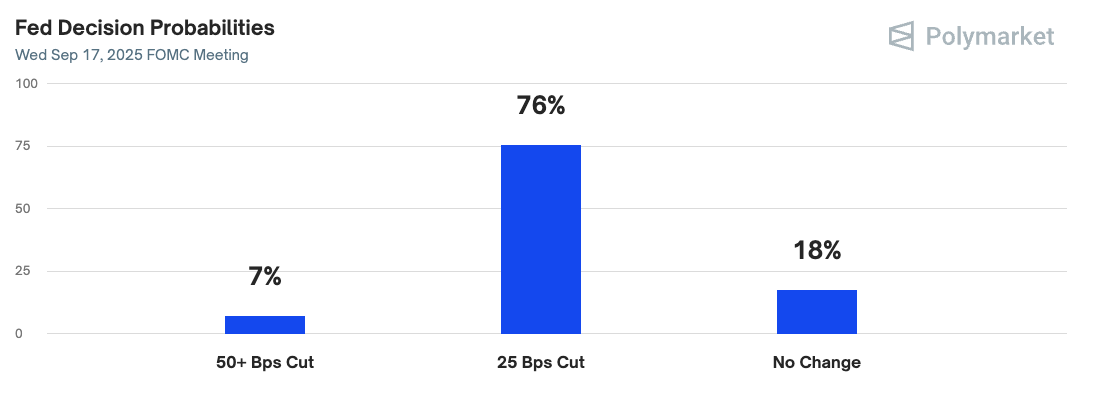

Late Thursday, President Trump named Council of Economic Advisers Chair Miran as the temporary replacement for departing Fed Governor Kugler—giving the administration a voting seat on the FOMC through January. Miran’s dovish policy stance and alignment with Governors Waller and Bowman increased expectations for a possible September rate cut. Yields moved higher at the long end of the curve, with some market participants concerned about the Fed’s perceived independence.

Trade policy developments were active. The U.S. confirmed retroactive refunds for excess tariffs charged to Japan, reiterated that no negotiations with India are planned until current disputes are resolved, and faced reports of Brazil preparing a multi-pronged response to U.S. tariff hikes. Meanwhile, headlines of a potential Trump–Putin agreement to formalize Russian territorial gains in Ukraine briefly sent crude prices lower before a partial recovery on skepticism over Kyiv’s acceptance. Gold prices were volatile after confusion over whether one-kilo bars from Switzerland would be subject to tariffs; the White House later clarified they would not.

With CPI, retail sales, and the U.S.–China tariff deadline ahead next week, recent market moves appeared more like positioning than decisive trend shifts. Market resilience continues to be supported by large-scale capex from mega-cap tech—now exceeding 1% of GDP—and by investor preference for cyclicals over defensives despite rising policy risks. These same drivers—tariff policy, AI adoption, and shifts in Fed dynamics—remain central to market direction into year-end.

Join LevelFields now to be the first to know about events that affect stock prices and uncover unique investment opportunities. Choose from events, view price reactions, and set event alerts with our AI-powered platform. Don't miss out on daily opportunities from 6,300 companies monitored 24/7. Act on facts, not opinions, and let LevelFields help you become a better investor.

AI scans for events proven to impact stock prices, so you don't have to.

LEARN MORE