Nuclear stocks like Cameco, Centrus, and BWXT rallied as AI-driven energy demand spotlights uranium and SMRs as U.S. power backbones.

Sectors & Industries

October 27, 2025

Table of Contents

This week, reports surfaced that Washington may be taking equity stakes in quantum-computing firms, marking another expansion of what’s become the best-performing institutional portfolio in the world.

Every disclosed government holding is now up at least +80%, with two nearing +150%. We’ve tracked this policy shift since early August, and Level 2 members have already captured a series of wins from it.

Level 2 Trade Receipts (Strategic-Reserve Theme):

The Strategic Reserve is the working arm of the administration’s February 2025 plan to build a U.S. sovereign wealth fund—not a single mega-pool, but a decentralized, deal-by-deal approach. The goal is to turn industrial policy into a return-generating portfolio that also secures control of key supply chains.

A large share of recent GDP growth has come from data-center construction, AI infrastructure, and critical-mineral expansion. Data centers now make up nearly 1% of GDP and over 7% of total fixed investment. Meanwhile, automation will replace some jobs, concentrating gains in capital-intensive sectors.

By taking small equity stakes or long-term offtake rights in projects where public funding already reduces risk — from AI data centers to rare earths, lithium, and copper supply chains — the government can build federal assets and capture part of the upside, rather than simply footing the bill for the transition.

This week’s U.S.–Australia critical-minerals deal shows how Washington is using joint investments to build leverage. The agreement backs Alcoa’s gallium project in Western Australia — expected to produce about 100 tons per year, roughly 10% of global supply — and adds access to germanium, another metal China has restricted.

Both are vital for chips, sensors, quantum tech, and defense systems. By co-financing projects and securing long-term offtake, the U.S. strengthens its bargaining power with allies and manufacturers while expanding non-Chinese supply-chain capacity in mining, refining, and advanced manufacturing.

The U.S. is building ownership and long-term supply links across semiconductors, rare earths, lithium, copper, and nuclear fuel to reduce reliance on China, which dominates rare-earth refining and has curbed exports of gallium, germanium, and graphite.

Projects like Trilogy Metals (TMQ), Lithium Americas (LAC), U.S. Antimony (UAMY), and MP Materials (MP) anchor this shift—securing inputs vital for defense, energy, and chip production. If trade tensions escalate, these holdings ensure the U.S. retains direct access to critical materials, protecting both industry and national security.

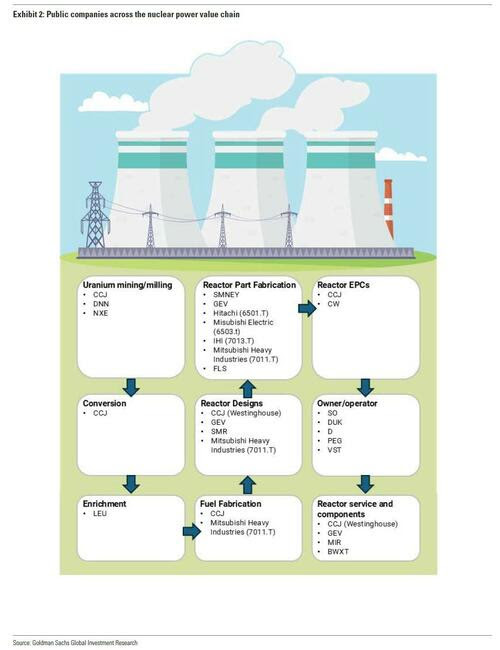

Nuclear stocks rebounded this week as new U.S. sanctions on Russia’s energy sector renewed focus on Moscow’s dominance in uranium enrichment and reactor exports. Russia still controls roughly 44–50% of global enrichment capacity and around 65% of new reactor exports, underscoring how dependent the world remains on a single source for nuclear fuel and technology.

That imbalance is risky at a time when AI data centers are straining the U.S. power grid. Electricity demand is rising at the fastest rate in decades, and grid operators have warned of regional shortages as data-center and semiconductor loads accelerate. In response, policymakers and utilities are increasingly turning back to nuclear power as the most reliable, zero-carbon source of steady energy. Oracle’s plan for a 1-gigawatt small modular reactor (SMR) campus reflects this shift — showing how nuclear is being positioned not just as clean baseload power, but as the foundation for meeting AI-driven electricity needs over the next decade.

A strategic U.S. stake in nuclear or uranium companies would serve two key objectives:

Level 2 members captured this nuclear theme early, securing strong gains across the value chain:

These companies anchor the U.S. nuclear value chain — CCJ and UUUU in uranium mining, LEU in enrichment and fuel fabrication, and BWXT in reactor components and defense systems. Others such as Constellation Energy (CEG), GE Vernova (GEV), Curtiss-Wright (CW), Denison Mines (DNN), and NexGen Energy (NXE) extend the ecosystem through generation, equipment, and mining exposure.

Join LevelFields now to be the first to know about events that affect stock prices and uncover unique investment opportunities. Choose from events, view price reactions, and set event alerts with our AI-powered platform. Don't miss out on daily opportunities from 6,300 companies monitored 24/7. Act on facts, not opinions, and let LevelFields help you become a better investor.

AI scans for events proven to impact stock prices, so you don't have to.

LEARN MORE