.png)

Macrosynthesis

TLDR: Record Highs as Trump Signs Tax Bill, Eyes Tariff Shock Next Week

Markets closed out June at record highs before the holiday weekend, lifted by Trump signing his $4.2 trillion “Big Beautiful Bill” into law and a stronger-than-expected June jobs report. The U.S. added 147,000 jobs and unemployment ticked down to 4.1%, easing recession fears but weakening the case for near-term rate cuts. Most gains came from public sector hiring, while private hiring remained soft—offering little evidence of broad-based momentum. Meanwhile, Treasury Secretary Bessent confirmed that new tariffs—ranging from 20% to 70%—set to begin rolling out Friday, with full implementation by the July 9 deadline, can be delayed until August 1. Some countries, like Vietnam and the UK, reached last-minute deals, but others including Japan and the EU remain at risk.

So far, only a handful of agreements have been finalized, including partial truces with Vietnam and the UK. Vietnam will face a 20% tariff on general exports and 40% on goods deemed to be re-routed Chinese components. Other nations—Japan, South Korea, the EU—remain in eleventh-hour talks, with some dispatching senior trade envoys to Washington this weekend in hopes of averting punitive rates. Behind the scenes, Treasury Secretary Scott Bessent confirmed that Trump alone will decide whether remaining talks count as “good faith” negotiations, underscoring the centralized, discretionary nature of this new trade doctrine.

The stakes are high. Bloomberg Economics estimates that if reciprocal tariffs are fully implemented at Trump’s proposed levels, average U.S. import duties could rise from 3% to nearly 20%—the highest in modern U.S. history. For now, markets have priced in optimism, buoyed by the perception that Trump’s tax cuts bill offsets some of the growth drag.

Investors who once feared Trump’s tariffs now appear emboldened by the administration’s temporary restraint. The current rally began not because tariffs were working, but because they were paused. The White House is betting that "peace through pressure" will force compliance.

Trump’s Fiscal Bet: Bubble Now, Bill Later

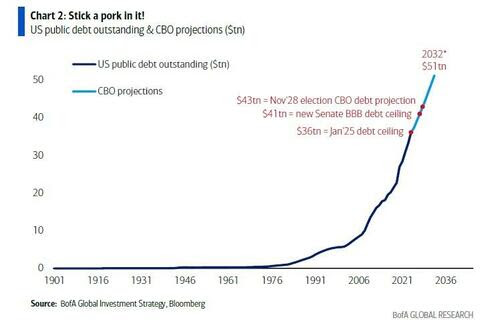

With the “Big Beautiful Bill” now signed into law, the U.S. enters a new phase of fiscal expansion—one defined less by restraint and more by velocity. The bill’s front-loaded tax breaks, defense outlays, and industrial incentives are expected to push the national debt past $50 trillion by 2032. Trump’s strategy, echoed across Wall Street, is clear: spark a demand boom now and deal with inflation or deficits later. As One River’s Eric Peters put it, the administration has “decided to go for broke and pump this economy into a boom to grow our way out of debt.”

Markets, for now, appear to welcome the approach. The dollar has slumped double digits year-to-date, gold just posted its strongest first half since 1979, and global equities ex-U.S. are riding a surge in capital rotation. Behind it all is a coordinated chase for real assets and growth proxies, driven by the view that the U.S. is entering an intentional era of engineered reflation. Whether it’s sustainable—or sets the stage for a more volatile unwind—remains to be seen.

Jobs Report Complicates Fed's Path Forward

The June jobs report gave markets a reality check. With 147,000 jobs added and the unemployment rate dipping to 4.1%, headline numbers beat expectations—but a closer look is warranted. Private payrolls rose by just 74,000, the weakest since last October, and the drop in unemployment was driven largely by workers exiting the labor force. Most of the hiring came from state and local governments, not private industry, reinforcing the narrative of a narrow labor recovery. Still, the data gave the Fed room to stay put. Traders quickly priced out a July rate cut, pushing yields higher and delaying expectations to September or beyond. The takeaway: the labor market isn’t strong enough to trigger hikes, but not weak enough to force cuts. For Powell, that means time to wait—and for markets, more uncertainty.

Trump's Rate Cut Push Meets Labor Reality

President Trump has made clear he wants lower interest rates—and fast. He’s publicly blamed Fed Chair Jerome Powell for “costing the U.S. $900 billion a year” in added interest expenses, citing the $9 trillion in debt coming due for refinancing this year. But the June jobs report makes that campaign harder to justify. A resilient labor market and still-firm wage growth weaken the case for aggressive easing. Even if the Fed were to cut rates as Trump wants, the savings on government debt are not as straightforward as he suggests.

Only a fraction of Treasury debt is short-term and highly sensitive to Fed moves. Meanwhile, cutting too much or too soon—especially under political pressure—risks spooking bond markets, pushing long-term yields higher and undercutting any savings from lower short-term rates. In short, Trump’s fiscal gamble hinges on borrowing costs staying low, but the Fed’s independence—and inflation risk—may stand in the way.

Rate Cuts Aren’t Meant for Booms—But That’s What Markets Want

Rate cuts have historically been used to cushion recessions, not accelerate bull markets. Yet in today’s environment, where growth is slowing but not collapsing, the hope for easier monetary policy is about one thing: liquidity. For equity markets, that means more fuel. Lower interest rates reduce discount rates, expand multiples, and unleash cash into risk assets—especially high-beta names and speculative pockets of the market. In other words, even a hint of a cut is a green light for the next leg of the rally.

Retail investors are already positioned for it. In the first half of 2025, they poured a record $155 billion into U.S. stocks and ETFs, outpacing even the meme-stock mania of 2021. Dip-buying remains relentless, penny stocks dominate volumes, and single-name tech plays like NVDA, TSLA, and PLTR are soaking up capital at a record clip. Even leveraged ETFs and GLD options are seeing outsized retail participation. The sentiment is clear: if the Fed cuts, the market rips.

The Liquidity Trade Is Alive—But Inflation Risk Is, Too

But there's a cost. Liquidity-driven rallies rarely stay contained. If the Fed cuts while fiscal stimulus is still surging, inflation could reaccelerate—especially with tariffs set to push prices higher by late summer. That’s the risk Powell faces: cut too soon and risk a second inflation wave; wait too long and risk tightening into slowdown. For now, markets are betting on the sweet spot—just enough weakness to justify easing, not enough to derail earnings or crush momentum.

In short, rate cuts are no longer about recession insurance. They’re becoming the trigger for the next leg of speculative excess. And as retail leads the charge, the line between reflation and overheating grows thinner by the day.

Last Week's Market Performance

Markets climbed again in a holiday-shortened week, with the S&P 500 rising +1.7% to 6,279, the Nasdaq gaining +1.6%, and the Dow jumping +2.3%—all closing at fresh record highs. Sentiment was fueled by Trump's trade agreement with Vietnam, easing tariff uncertainty, and a stronger-than-expected June jobs report that tempered recession fears without fully reviving rate cut expectations.

Trump’s signing of the “One Big Beautiful Bill” on Friday capped the week, cementing a historic fiscal expansion and pushing risk assets higher. Meanwhile, momentum broadened across sectors: Materials (+3.7%) and Financials (+2.4%) led the way, with Tech (+2.4%) remaining a key driver. Energy rebounded +2.1% despite tariff threats on global metals.

Commodities: WTI oil rose +1.5% to $66.49/bbl. Gold gained +1.8% to $3,346.5/oz. Natural gas tumbled -9.3%.

Top Gainers: Nike (+22%) on upbeat guidance, First Solar (+19%) after strong inflows, Hewlett Packard Enterprise (+16%), Carnival (+14%), Wynn Resorts (+14%)

Laggards: Centene (-38%) and Molina Healthcare (-18%) dragged Healthcare lower amid reimbursement concerns; Palantir (-7%) and Elevance Health (-7%) also declined on rising costs for medical care.

Upcoming Events This Week

Markets will turn their attention to trade policy this week as the U.S. approaches the July 9 tariff snapback deadline. Several key trading partners are racing to finalize agreements or request extensions, with President Trump expected to unveil new tariff rates for roughly a dozen nations starting Monday. Beyond trade, investors will be watching the release of the FOMC minutes for insights into the Fed’s policy stance, while global data flows pick up with inflation prints from China (CPI and PPI), German trade figures, and interest rate decisions from central banks in Australia, South Korea, and New Zealand.

.png)

Company News

LevelFields AI Stock Alerts Last Week

Datadog (DDOG) +14.9% on S&P 500 Inclusion, +17% Weekly Surge

Shares of Datadog surged nearly 15% in a single session and finished the week up around 17% after S&P Dow Jones Indices confirmed DDOG will replace Juniper Networks in the S&P 500 on July 9. This milestone typically triggers automatic inflows as index-tracking funds rebalance, boosting visibility and liquidity. Datadog’s strong revenue growth, profitability, and cloud infrastructure footprint reinforce its appeal in large-cap tech.

Enovix (ENVX) +9.6% on $60M Share Buyback

Enovix jumped 9.6% after announcing a $60 million share repurchase program—representing a meaningful commitment to shareholder return at a time of aggressive scaling. The battery tech firm has been under pressure amid capital intensity and production ramp-up costs, but the buyback signals confidence in its long-term trajectory and financial footing. Management emphasized strategic flexibility and a disciplined capital return framework as core to its next phase of growth.

Big Tech Slips on AI Regulation Surprise

Major tech stocks fell early last week after a key provision in Trump’s “One Big Beautiful Bill” — a 10-year federal ban on state-level AI regulation — was unexpectedly struck down in the Senate by a 99-1 vote. The provision, backed by White House officials and tech-aligned Republicans, aimed to preempt states from enacting their own AI laws, creating a uniform federal standard favorable to companies like Google, Meta, and Microsoft.

The sudden policy reversal spooked investors. With the moratorium scrapped, firms now face a fragmented regulatory landscape, potential legal challenges, and rising compliance costs as states pursue their own AI rules. Despite the bill’s broader windfall for tech — including billions in federal contracts for AI infrastructure — the loss of regulatory certainty triggered a pullback in major AI names, with the Nasdaq lagging the broader market midweek.

Tesla Slides on Sales Miss, Cybertruck Flop, and Musk’s Management Shuffle

Tesla shares fell nearly -3% this week after a barrage of negative developments raised fresh concerns about demand, execution, and leadership stability. The EV giant reported Q2 global deliveries of 384,122—down 13% YoY and marking its second straight quarterly decline. Analysts now expect full-year deliveries to fall 8% in 2025, reinforcing fears that growth has peaked in the core auto segment.

Cybertruck sales were a particular disappointment. Tesla lumped the model into its “other” category (with Model S and X), which saw sales drop -19% QoQ and production fall -52% YoY. With just over 10,000 Cybertruck units delivered in Q2—under 3% of total volume—the long-hyped vehicle is increasingly viewed as a commercial failure, dragging down Tesla’s margins and momentum.

Elon Musk’s decision to personally retake control of U.S. and European sales following the departure of top executive Omead Afshar added to the uncertainty. While senior VP Tom Zhu was handed global manufacturing duties, the shake-up reflects broader strain, particularly in Europe, where Tesla’s registrations plunged -37% YTD amid backlash to Musk’s right-wing political endorsements and repeated political controversies.

The news compounds investor concerns that Musk’s pivot to robotaxis and AI has yet to deliver tangible results. Despite ambitious autonomy goals, execution risks and brand damage remain dominant themes, with analysts warning that Tesla’s valuation premium is increasingly difficult to justify as sales stagnate and internal friction mounts. Adding to the trouble this weekend was Musk's commitment to start a new political party - a venture many consider a fool's errand and investors consider a major distraction from his CEO duties at Tesla.

.png)

Bumble Swipes Left on Employees, Rallies 30%

Tesla's Robotaxi Launch - How it Really Went

Lockheed Martin's Having a Great Year

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai