.png)

Macrosynthesis

TLDR: Markets Grind Higher on Fed Shuffle, Tariff Chess, and Big-Tech Resilience

The first full week of August was shaped by political maneuvering, shifting trade positions, and selective sector strength. Equities ended broadly higher, with tech, communications, and financials leading while defensive sectors underperformed. The S&P 500 gained 0.8% and the Nasdaq rose nearly 1%, supported by solid earnings from companies including Motorola Solutions, Akamai, and Block. The tone reflected a mix of optimism over potential rate cuts and caution over ongoing trade and geopolitical uncertainty.

Late Thursday, President Trump named Council of Economic Advisers Chair Miran as the temporary replacement for departing Fed Governor Kugler—giving the administration a voting seat on the FOMC through January. Miran’s dovish policy stance and alignment with Governors Waller and Bowman increased expectations for a possible September rate cut. Yields moved higher at the long end of the curve, with some market participants concerned about the Fed’s perceived independence.

Trade policy developments were active. The U.S. confirmed retroactive refunds for excess tariffs charged to Japan, reiterated that no negotiations with India are planned until current disputes are resolved, and faced reports of Brazil preparing a multi-pronged response to U.S. tariff hikes. Meanwhile, headlines of a potential Trump–Putin agreement to formalize Russian territorial gains in Ukraine briefly sent crude prices lower before a partial recovery on skepticism over Kyiv’s acceptance. Gold prices were volatile after confusion over whether one-kilo bars from Switzerland would be subject to tariffs; the White House later clarified they would not.

With CPI, retail sales, and the U.S.–China tariff deadline ahead next week, recent market moves appeared more like positioning than decisive trend shifts. Market resilience continues to be supported by large-scale capex from mega-cap tech—now exceeding 1% of GDP—and by investor preference for cyclicals over defensives despite rising policy risks. These same drivers—tariff policy, AI adoption, and shifts in Fed dynamics—remain central to market direction into year-end.

Fed Power Shift and a Split Market Signal

Markets welcomed President Trump’s appointment of CEA Chair Miran as temporary Fed Governor through January, interpreting his dovish stance as a sign that September rate cuts are more likely. Utilities (XLU) have gained 9% over the past six months on the belief that falling rates will boost high-dividend, rate-sensitive sectors. Gold (GLD), meanwhile, is up 16.65% over the same period, signaling concern that aggressive easing could reignite inflation and undermine the Fed’s credibility. The split reflects a market hedging its bets—allocating capital to both beneficiaries of lower yields and assets that protect against the consequences of cutting too soon.

The push for easier policy is also feeding speculative behavior. Retail trading volumes in options and high-beta equities have picked up, with flows concentrating in AI leaders and other momentum names. The market is in an odd place where companies posting strong growth are either trading flat or popping at the open only to sell off sharply later in the day—often a sign that retail flows are dominating while institutions sit on the sidelines waiting for better entry points or clearer economic data. When that pattern coincides with financial media pushing “valuations are getting out of hand” headlines, it has historically marked a temporary top before a 5-10% pullback.

Robots, AI, and the Long-Term Rate Debate

The same market betting on near-term cuts is also staring at a longer-term question: if AI and robotics deliver the kind of productivity gains their backers promise, will the natural rate of interest start moving higher instead of lower? Historical productivity surges—from steam power to the internet boom—were accompanied by higher rates as capital demand rose. Bloomberg’s base case sees trend growth in advanced economies slowing to around 1.1% by 2050, keeping rates under downward pressure. But in an optimistic scenario where AI, quantum computing, and advanced robotics lift U.S. productivity growth toward 2.4% in the 2030s, the long-term neutral rate could rise by 0.5–0.6 percentage points.

The path matters for investors because it shapes both valuations and sector leadership. A genuine productivity boom would favor capital-intensive industries, infrastructure buildouts, and companies supplying the AI economy—yet it could also sustain higher borrowing costs, pressuring rate-sensitive assets that are thriving under today’s cut expectations. If the technology wave proves more job-displacing than job-creating, productivity gains may not be enough to push rates up meaningfully, while inequality and demand drag could keep policy looser for longer.

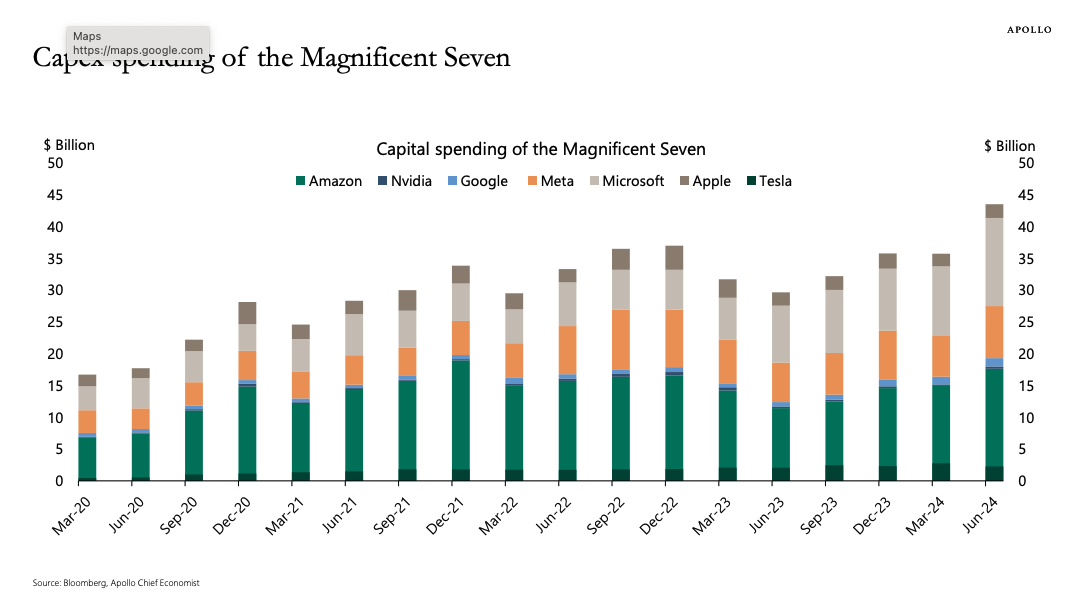

Capex Pressure and the Shift to Private Credit

The scale of AI capex has become so large that even mega-cap balance sheets are looking outside public markets to keep spending. Meta just tapped Pimco and Blue Owl for $29 billion in financing to fund a massive Louisiana data center build—$26 billion in debt and $3 billion in equity—after a hiring spree that poached niche AI talent from competitors at price tags running into the hundreds of millions per head. This comes on top of similar private capital partnerships by Microsoft and Elon Musk’s xAI, proving that the AI race is driving expenditures and borrowing. For investors, the pivot to private credit is a risk that cash burn could eventually outpace returns if revenue growth doesn’t scale fast enough.

From AI Boom to AI Bubble?

In the short run, the market’s AI trade is still the most popular. Since April’s post-selloff rebound, just ten stocks—largely the Mag 7 plus AVGO, ORCL, and PLTR—have driven roughly 80% of S&P 500 gains. That concentration, reinforced by policy tailwinds, has pushed valuations to extremes that rely on uninterrupted capital flows into a handful of names. Hartnett warns the signal for a genuine AI bubble break will be widening tech credit spreads, echoing the 1999 pattern when cash burn fears ended the dot-com melt-up.

Until that stress shows up, momentum could keep running, especially with $2.9 trillion in AI-related capital expenditures projected by 2028. When media headlines shift from celebrating the AI boom to warning that valuations are “getting out of hand,” it’s often the last stage before a sentiment break. For now, both the productivity dream and the bubble risk are in play—a combination that can stretch markets higher in the short term but leaves little room for disappointment during earnings results.

Energy Crunch Fuels Nuclear Revival

The AI infrastructure boom is igniting a nationwide fight over energy policy. Surging power demand from hyperscale data centers, EV adoption, and electrification trends has collided with years of underinvestment in baseload capacity, triggering public backlash in high-demand corridors like the Mid-Atlantic, Northeast, and Arizona. In Tucson, city officials recently killed a $3.6 billion Amazon Web Services data center plan over water and energy concerns, joining 142 grassroots groups across 28 states that have blocked or delayed over $60 billion in similar projects.

Critics argue that past policy choices—retiring reliable fossil fuel plants while over-relying on intermittent renewables—left the U.S. ill-prepared for the AI era’s power needs. The pivot now is clear: momentum is building for nuclear as the clean, scalable baseload solution capable of supporting the decade-long AI buildout without crushing consumers with soaring electricity bills. Energy Secretary Chris Wright has likened the AI arms race with China to “the next Manhattan Project,” urging the securing stable power at scale.

The nuclear push isn’t limited to Earth. NASA just confirmed plans to build a small nuclear reactor on the Moon by the late 2030s to power lunar bases and research stations. With domestic utilities, private capital, and federal agencies now converging on nuclear, the sector is poised for a structural demand surge not seen since the mid-20th century.

The expected demand for nuclear drove massive gains in nuclear startup stocks like SMR and OKLO, both up well over 100% in the past year despite having little to no revenue.

Trump Pushes Russia–Ukraine Talks

President Trump is moving to broker an end to the Russia–Ukraine war, calling it potentially his “greatest deal.” His envoy, Steve Witkoff, met with Vladimir Putin in Moscow, delivering an invitation for face-to-face talks next week. Secretary of State Marco Rubio said the U.S. now has concrete examples of Russia’s demands to end the conflict. Trump has briefed Ukrainian President Zelenskyy and European leaders, aiming to bring Putin and Zelenskyy together for a final agreement.

The proposed meeting is set for August 15 in Alaska — which Russia sold to the U.S. — in what analysts see as both a symbolic and strategic venue. The location hints at broader negotiations over trade routes, resources, and spheres of influence. Trump has suggested the talks could lead to a land-swap arrangement “benefiting both sides,” though Ukraine is opposed to ceding any territory, including Crimea and the Donbas.

European leaders, meeting earlier at Trump’s Scotland resort, reaffirmed that borders cannot be changed by force, but privately, U.S., European, and Ukrainian officials in the UK have discussed potential ceasefire terms. The White House has also delayed a planned tariff ultimatum on Russian goods from August 9 to August 27 to avoid messing up the peace talks.

Defense stocks retreated on the headlines, with Rheinmetall (RNMBY) down 3%, L3Harris (LHX) off 1.5%, and Lockheed Martin (LMT) lower by 1.17%.

Last Week's Market Performance

U.S. equities posted their best week since late June, with the S&P 500 up +2.4% to 6,389, Nasdaq up +3.9% to 21,450, and Dow up +1.3% to 44,176. A sharp rebound from last week’s weak July jobs report, strong tech earnings, and tariff-related relief drove gains, while news of potential Russia–Ukraine peace talks added to risk appetite. Early in the week, Apple’s $100B U.S. investment pledge—stacked on top of its prior $500B commitment—was seen as a move to sidestep future tariff impacts and fueled broad tech momentum. Midweek, Trump’s “Liberation Day” trade measures officially took effect, with additional plans for 100% tariffs on semiconductor imports—but exemptions for domestic manufacturers eased market concerns.

Sectors – Tech (+4.3%), Consumer Discretionary (+3.8%), and Consumer Staples (+3.1%) led the charge, supported by Utilities (+0.4%) and Financials (+0.7%). Energy (-1%) and Healthcare (-0.8%) lagged.

Commodities – WTI crude slid -5.1% to $63.88/bbl, while gold surged +2.7% to $3,491.3/oz. Natural gas fell -3% to $2.99.

FX & Crypto – The USD weakened against the GBP (+1.29%) and EUR (+0.47%), while crypto saw a broad rally: Bitcoin +3.3%, Ethereum +18.9%, XRP +19.3%.

Top S&P 500 Gainers – IDEXX Laboratories (+23%), Palantir (+21%), Arista Networks (+18%), Axon Enterprise (+13%), Micron (+13%).

Top S&P 500 Losers – The Trade Desk (-37%), Gartner (-30%), Fortinet (-24%), Super Micro Computer (-21%), Vertex (-21%).

Global Indices – France +2.6%, Germany +3.2%, Japan +2.5%, China +2.1%, Hong Kong +1.4%, UK +0.3%. India was the lone major laggard (-0.9%).

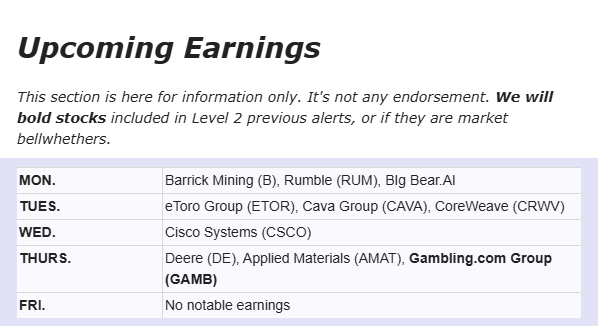

Upcoming Events This Week

Markets will track US–China trade negotiations closely ahead of the August 12 deadline, when tariffs above 100% could take effect. A Trump–Putin meeting aimed at resolving the Ukraine conflict will also draw attention.

In the US, July’s CPI and PPI reports will be the main focus, with inflation expected to hit its highest level in five months. Retail sales, industrial production, and consumer sentiment are also on deck, alongside import/export prices, business inventories, and regional manufacturing surveys. The Fed’s policy outlook will be shaped by Stephen Miran’s confirmation process and upcoming speeches from central bank officials. Q2 earnings season wraps up with results from Cisco, Applied Materials, Deere, and several Chinese ADRs.

.png)

Company News

LevelFields AI Stock Alerts Last Week

Tidewater (TDW) +29% on $500M Buyback

Shares of Tidewater surged 29% after the company’s Board of Directors authorized a new $500 million share repurchase program. Management framed the move as a strong vote of confidence in long-term growth prospects and capital allocation discipline.

Backblaze (BLZE) +24.9% on Buyback Announcement

Backblaze jumped nearly 25% in a single session after unveiling a $10 million share repurchase program. The cloud storage provider’s board cited a compelling valuation and healthy cash position as key drivers behind the decision.

Record U.S. Store Closures in 2025 Signal Deepening Consumer Strain

U.S. retailers are shutting their doors at a pace not seen before, with over 120 million square feet of retail space permanently closed in the first half of 2025. According to Coresight Research, 5,822 closures were announced by June 27—far outpacing the 3,496 seen over the same period last year and on track to break the pandemic-era record.

At Home and Rite Aid together accounted for a significant portion of space lost, while Claire’s announced 18 store closures after filing for Chapter 11—its second bankruptcy since 2018. Big box retailers like Big Lots, Joann Fabrics, Kohl’s, JCPenney, Macy’s, and Party City are also accelerating downsizing as debt burdens rise and in-store traffic drops.

The rapid growth of online platforms like Amazon, Temu, Shein, and TikTok’s social commerce are largely to blame. But struggles among consumers are a concern.

Student loan delinquencies jumped to 12.9% in Q2, up sharply from 8% in March and well above pre-pandemic norms. Continuing jobless claims have climbed to 1.97 million—the highest since late 2021—while U.S. manufacturing activity has contracted for five consecutive months. With the average tariff rate now near 18%, the highest since the 1930s, retailers face rising import costs alongside falling demand.

Moody’s Analytics chief economist Mark Zandi warned that the economy is “on the precipice of recession,” citing flat consumer spending, weakening labor trends, and no near-term relief from the Fed. If these pressures persist, store closures could accelerate, leaving even familiar local retailers at risk of disappearing by 2026.

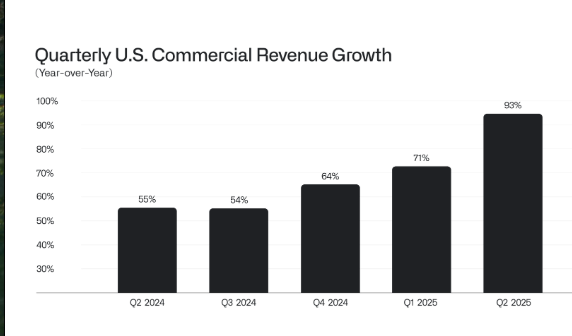

Palantir Delivers Blowout Quarter, Raises Full-Year Outlook

Palantir posted another blockbuster quarter, with Q2 revenue surging 48% YoY to $1.00B, handily beating estimates and marking its 8th straight quarter of accelerating growth. Operating profit more than doubled to $269M, while adjusted operating margin expanded to 46% from 37% a year ago. Free cash flow jumped nearly fourfold to $569M.

Growth was broad-based: U.S. commercial revenue—now the company’s “emerging core”—soared 93% to $306M, while government sales climbed 49%. CEO Alex Karp pointed to three “mega trends” powering demand: custom AI applications, data infrastructure investment, and defense tech modernization.

The company raised its FY25 revenue guidance to $4.14–$4.15B (from $3.89–$3.90B) and now expects adjusted operating profit of $1.91–$1.92B, with free cash flow potentially hitting $2B. Q3 revenue is projected at $1.08–$1.09B, well ahead of consensus.

UBS called the results a “clean beat” with “no cracks in the story,” boosting its price target to $165 from $110, though valuation remains a sticking point at 136x projected 2026 free cash flow. Analysts noted the print strengthens the bullish case for data and AI infrastructure leaders like Snowflake and Databricks.

.png)

Using AI to Spot Dividend Stocks

This Stock is Up 1500%. You've Likely Never Heard of It.

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai