.png)

L1 Weekly Stock Market News Analysis

December 21st, 2025

TLDR:

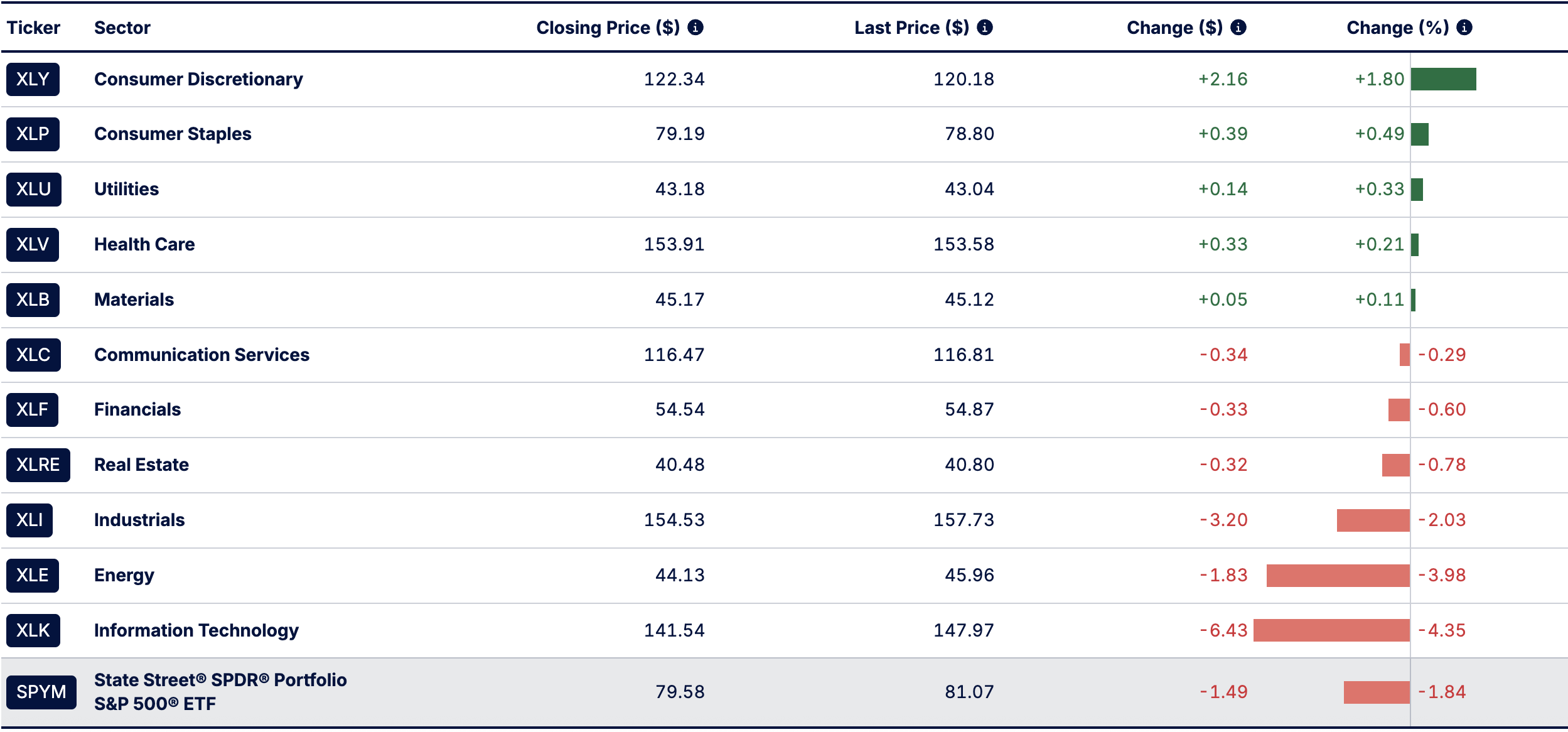

Markets steadied toward the end of the week, but leadership shifted beneath the surface. Defensive and consumer-oriented sectors held up best, with Consumer Discretionary (XLY), Consumer Staples (XLP), Utilities (XLU), Health Care (XLV), and Materials (XLB) all finishing modestly higher. In contrast, areas more exposed to heavy capital spending and longer-dated growth lagged, led by Technology (XLK), Energy (XLE), Industrials (XLI), Financials (XLF), and Real Estate (XLRE), highlighting growing selectivity rather than a broad risk-on move.

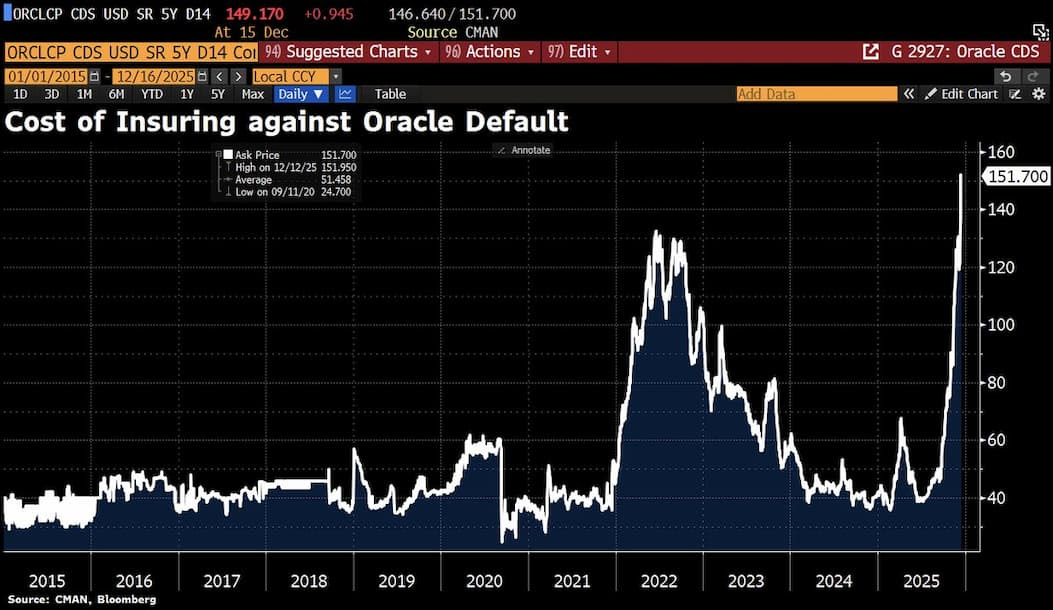

That caution was reinforced by developments in AI infrastructure later in the week. Oracle disclosed delays in some of its largest AI-related data-center projects, pushing portions of the OpenAI-linked buildout further into the future. Demand hasn’t disappeared, but the timeline shift sharpened investor focus on financing risk — especially as Oracle carries over $100 billion in debt and large long-term lease commitments.

Credit markets responded quickly. The cost of insuring Oracle’s debt rose to its highest level since 2009, with current pricing implying roughly a 15% probability of default. That doesn’t signal an imminent failure, but it does mark a meaningful shift in how lenders are viewing the risk. AI data centers require enormous upfront spending, while much of the revenue arrives years later, creating a gap between cash going out today and cash coming in tomorrow.

Taken together, the week’s action suggests markets aren’t questioning whether AI demand exists — they’re questioning how it’s financed, and which sectors and companies can absorb tighter credit conditions without strain.

Holiday Liquidity Thins, Volatility Speaks Louder

As markets move deeper into the Christmas holiday period, trading volumes thin sharply. Institutional desks scale back activity, portfolio managers lock books, and liquidity fades. In that environment, price action becomes increasingly driven by retail flows and short-term positioning, making markets far more sensitive to headlines than they would be during heavier trading periods.

That dynamic was evident this week. Early in the week, the S&P 500 was down more than 1.5% and the Nasdaq-100 (QQQ) fell nearly 2%, as selling accelerated during low-volume sessions. By week’s end, both indexes recovered much of those losses and finished roughly flat.

That rebound, however, should not be read as the underlying issue being resolved. In thin holiday markets, relatively small flows can push prices sharply in either direction, making short-term moves — up or down — poor indicators of whether a narrative has truly turned.

In other words, the week’s price action reflected liquidity conditions, not a clean verdict on the deeper concerns investors are still digesting.

Oracle Was the Early Warning — and Financing Pressures Are Becoming Visible

In last week’s newsletter, we noted that Oracle disclosed delays in some of its largest AI-related data center projects, pushing portions of the buildout tied to OpenAI from 2027 to 2028. The company cited labor and material constraints, but the practical implication was straightforward: timelines for major AI infrastructure projects are stretching.

That matters because AI data-center construction has been one of the largest sources of new private investment in the U.S. this year, accounting for a significant share of incremental economic growth at a time when other areas of spending have slowed. When project timelines move out, even modest delays can ripple through construction activity, equipment orders, and related supply chains.

What Happened With Blue Owl

Oracle had been in discussions with Blue Owl Capital to help finance a $10 billion data center in Michigan intended to support OpenAI workloads. In arrangements like this, a private-credit investor typically funds construction and then leases the facility back to the technology company over many years, allowing the company to avoid paying the full cost upfront while taking on long-term lease obligations instead.

As Oracle’s debt levels increased and its AI spending commitments grew, lenders involved in the discussions pushed for stricter repayment terms and more conservative deal structures. According to people familiar with the talks, the revised terms reduced the project’s attractiveness for Blue Owl, which ultimately chose not to move forward under those conditions.

Oracle has since said the project itself remains on track and that another financing partner may step in. That remains possible. But the market reaction focused less on the fate of a single facility and more on the changing cost and availability of financing for large AI infrastructure projects.

Credit Markets Are Now Asking the Same Question

Concerns that first surfaced in the stock market are now showing up more clearly among lenders.

The cost of insuring Oracle’s debt against default has climbed to its highest level since 2009. Based on current credit-market pricing, investors are now assigning roughly a 15% probability that Oracle could default on its debt — a meaningful change in how the company’s risk is being viewed.

Oracle carries over $100 billion in debt, along with long-term lease commitments that extend well into the next decade. At the same time, many of its largest AI-related contracts are structured to deliver most of their revenue years in the future, not immediately.

Put simply, Oracle is spending large amounts of cash today while much of the expected payoff comes later. That timing mismatch — and the growing risk it creates — is what credit markets are now focused on.

Markets Stabilized Later in the Week — But Financing Questions Remain

Later in the week, markets stabilized as a series of announcements reassured investors that AI demand and strategic relevance remain strong, even as financing pressures persist.

Oracle shares rebounded after the company confirmed binding agreements to lead a new U.S. joint venture for TikTok. The deal gives Oracle a central role in securing TikTok’s U.S. data, operating its cloud infrastructure, and overseeing algorithm governance under a majority-American ownership structure. That announcement removed a long-running regulatory overhang and reinforced Oracle’s importance as a trusted infrastructure partner for large, sensitive platforms.

At roughly the same time, CoreWeave announced that it had joined the federal government’s “Genesis Mission,” a major U.S. initiative designed to accelerate scientific discovery, energy innovation, and national security through artificial intelligence.

These headlines helped ease near-term anxiety in thin holiday markets. But they addressed demand and strategic relevance, not the growing question of how AI infrastructure is being financed.

What the Genesis Mission Is

The Genesis Mission was established by executive order earlier this fall and is best understood as a coordinated national effort to embed AI into the core of U.S. scientific and energy research.

At its core, the program aims to:

- Link Department of Energy national laboratories, federal supercomputers, and decades of government research data

- Provide researchers with large-scale AI computing power

- Shorten timelines for breakthroughs in areas like energy, materials science, manufacturing, health, and national security

Rather than building everything in-house, the government is partnering with private companies that already operate advanced AI infrastructure. Firms like CoreWeave, Nvidia, Microsoft, Amazon, Google, and others are contributing cloud platforms, hardware, and technical expertise to support these workloads.

For companies like CoreWeave, participation signals:

- Long-term relevance to national priorities

- Potentially steady demand from public-sector and research customers

- Deeper integration into government and defense-adjacent projects

In short, the Genesis Mission strengthens the strategic case for AI infrastructure and reinforces that the U.S. government views advanced computing as essential to economic and national security goals.

Why Credit Markets Are Still Cautious

Even with policy support and strong demand signals, credit markets are becoming more cautious about how AI infrastructure is being financed — especially for companies operating at massive scale.

The chart below shows CoreWeave’s credit default swap (CDS) spread, which measures how much investors are paying to insure against the company defaulting on its debt. As that line has risen, it indicates that lenders believe CoreWeave’s risk of default is increasing.

The concern is straightforward:

- AI data centers require enormous upfront spending

- Much of the revenue arrives years in the future

- That creates a gap between cash going out today and cash coming in later

Even companies with strong customer demand, government partnerships, and strategic importance are not immune to that timing mismatch. The market is not questioning whether AI will be used or whether these platforms are valuable. It is questioning how much debt the system can safely support while the infrastructure is still being built.

AI is moving from a story about growth potential into a capital-intensive construction phase, where financing terms, leverage, and cash-flow timing matter far more.

That tension — long-term demand versus near-term financing pressure — is what investors are now grappling with as the year comes to a close.

What This Means for Positioning

The message from markets isn’t “AI is over.” It’s that balance sheets and financing discipline now matter as the cycle matures. That calls for a more selective, barbell-style approach.

Be Careful With Leverage-Heavy AI Infrastructure

- Oracle (ORCL) and CoreWeave (CRWV) remain strategically important, but rising default risk and tighter credit conditions make them tradeable, not foundational positions here.

- These are names to trim into strength, hedge, or wait for better entry points, not chase after rebounds driven by thin liquidity.

Prefer AI Exposure With Cleaner Balance Sheets

AI beneficiaries with stronger cash generation and less financing risk remain the higher-quality way to stay involved in the theme:- NVIDIA (NVDA)

- Microsoft (MSFT)

- Amazon (AMZN)

These firms benefit from AI demand without relying on aggressive, debt-heavy infrastructure buildouts to survive.

Barbell With Yield, Dividends, and Real Assets

If inflation continues to cool and yields drift lower, income and duration regain relevance — especially as equity sentiment runs hot.

- High-dividend and dividend-growth stocks offer ballast if volatility returns. This is where tracking recent dividend increases matters most — companies raising payouts are signaling confidence in cash flow.

- Utilities & defensives: NextEra Energy (NEE), Duke Energy (DUK)

- Energy & cash-flow names: Exxon Mobil (XOM), Chevron (CVX)

- Industrials with pricing power: Caterpillar (CAT)

- Real assets and commodities remain effective hedges if financing stress reappears:

- Copper & materials: Freeport-McMoRan (FCX)

- Uranium / energy security: Cameco (CCJ)

Respect the Setup

With record inflows into passive equity ETFs like Vanguard S&P 500 ETF (VOO) and iShares Core S&P 500 ETF (IVV), sentiment is elevated. That favors buying pullbacks, not chasing upside — especially in names tied to heavy capital spending.

Last's Weeks Sector Winners & Losers

Sector performance showed a clear defensive tilt rather than broad risk-on leadership. Consumer Discretionary (XLY) led on the upside, rising +1.80%, followed by modest gains in Consumer Staples (XLP), Utilities (XLU), Health Care (XLV), and Materials (XLB) — signaling selective positioning rather than aggressive cyclical exposure. These moves suggest investors favored areas with steadier cash flows and pricing power amid ongoing uncertainty around growth and financing conditions.

On the downside, Information Technology (XLK) was the clear laggard, falling -4.35%, reflecting continued pressure tied to AI spending scrutiny and capital intensity concerns. Energy (XLE) also underperformed sharply, down nearly -4%, while Industrials (XLI) declined -2.03%, reinforcing that capital-heavy sectors struggled as financing questions resurfaced. Financials (XLF), Real Estate (XLRE), and Communication Services (XLC) also finished lower, pointing to a market that remained cautious rather than broadly risk-seeking despite late-week stabilization.

Upcoming Events This Week

Markets will be quieter with early closes on Dec. 24 and a full shutdown on Dec. 25, but several key data points are still on deck. In the U.S., focus is on durable goods orders, the second estimate of Q3 GDP (expected to confirm ~3.2% growth), corporate profits, industrial production, and Conference Board consumer confidence, along with regional Fed indicators.

Internationally, Canada releases monthly GDP and the BoC’s summary of deliberations; Europe reports EU new car registrations; and Asia-Pacific features RBA and BoJ minutes, plus Japan’s housing starts, unemployment, industrial production, and retail sales.

Company News

LevelFields AI Stock Alerts Last Week

DBVT +25% on Breakthrough Therapy Validation

DBV Technologies (DBVT) jumped roughly 25% after reporting a successful Phase 3 trial for its Viaskin Peanut patch in children with peanut allergies. Nearly 47% of treated patients met responder criteria vs. ~15% on placebo, a statistically significant result in a large global study. With FDA Breakthrough Therapy Designation already in place, the company plans to submit its BLA in H1 2026, accelerating the regulatory path. The move reflects how, in a selective market, clear clinical milestones still unlock sharp upside, even amid broader risk scrutiny.

RKLB +17% on Billion-Dollar Defense Contract

Rocket Lab (RKLB) surged ~17% after winning an $816M prime contract from the U.S. Space Force to build missile-tracking satellites for the Tranche 3 program, with total potential capture approaching $1B including follow-on subsystem work. The award reinforces Rocket Lab’s position as a vertically integrated defense-space prime, benefiting from government-backed demand that is less sensitive to financing cycles. In contrast to leveraged AI infrastructure builds, this rally highlights investor preference for revenue-backed growth tied to national security spending.

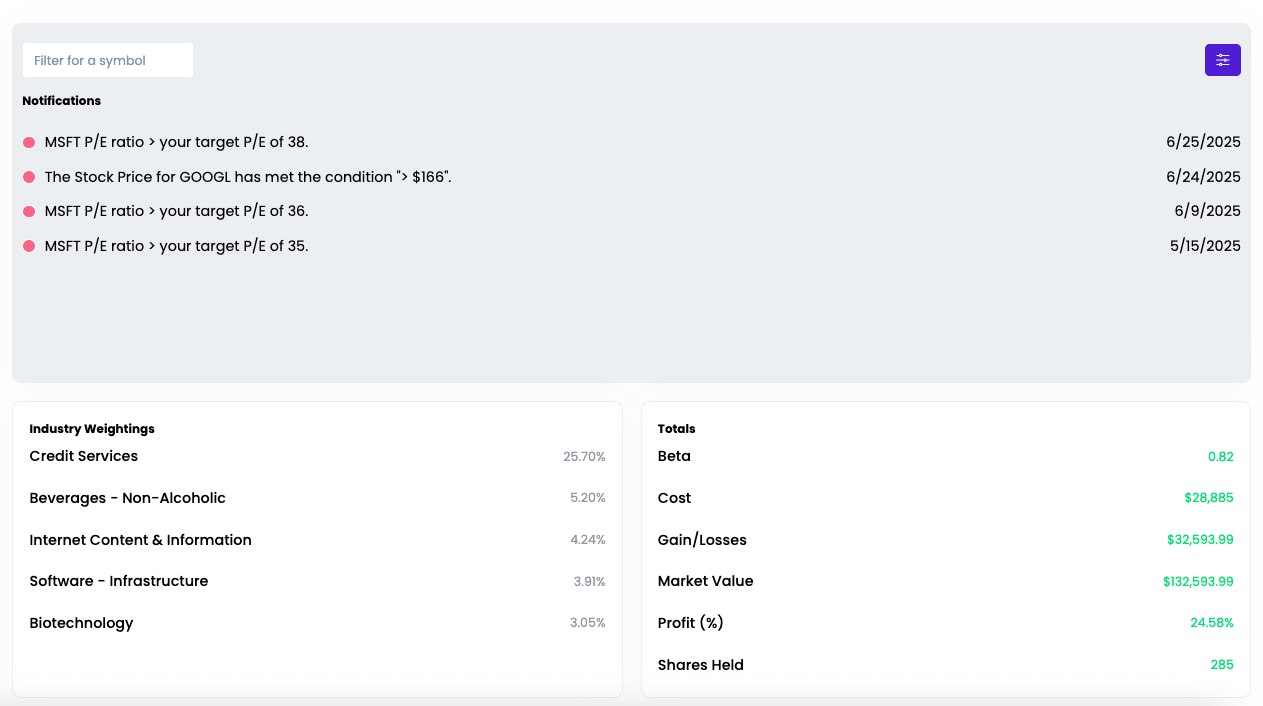

Introducing the LevelFields Portfolio Tracker

We’ve just launched the new LevelFields Portfolio platform — a centralized dashboard built for active investors and wealth managers to track their trades, organize trade ideas, and monitor real or prospective portfolios.

We've replaced Excel and Google Sheets trade tracking with software that updates as prices and valuations of stocks change, so you don't lose money by missing great entry and exit points.

You can sign up for free!

What it does:

- Lets you add both real positions and idea-stage trades into one unified portfolio.

- Tracks allocation, profit/loss, KPIs, P/E, price targets, and thesis notes in one place.

- Allows you to set real-time alerts on valuation changes, price moves, and price targets using bulk editing (e.g. one alert for all holdings).

- Lets you toggle any ticker between “Idea → Holding → Closed” while preserving the original trade thesis and exit notes.

- Designed for traders, advisors, and fund managers who need a live, organized view of positions + rationale, not just a static spreadsheet of tickers.

- Import CSV file of existing ideas, notes, and portfolio holdings for a quick start

- Keep track of reasons you bought and sold to analyze your performance and for compliance

- Design your own model portfolios based on allocations, sector, and industry

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai