.png)

Macrosynthesis

TLDR: Markets Flatline as Tariff Threats Meet Strong Data

Markets drifted sideways last week, balancing fresh tariff anxiety with solid economic data and a surge in trading-driven bank earnings. The S&P 500 and Nasdaq posted weekly gains of 0.5% and 1.4%, respectively, while the Dow slipped, dragged down by American Express and a late-week selloff sparked by Trump’s renewed push for a 15–20% minimum tariff on all EU goods ahead of the August 1 deadline. The mixed tone showed a market caught between political noise and resilient fundamentals.

Economic data reports came in strong: housing starts beat expectations, and the University of Michigan consumer sentiment index rose with one-year inflation expectations dropping to a five-month low at 4.4%. Those tailwinds were reinforced by Fed Governor Waller, who reaffirmed his support for a July rate cut, citing early signs of labor market weakness and tame inflation. That commentary helped push Treasury yields lower across the curve and solidified expectations for near-term easing, even as the Fed entered its pre-decision “quiet period,” when officials refrain from public commentary ahead of the July 30 FOMC meeting.

Meanwhile, Wall Street’s largest banks capitalized on the macro churn. Trading revenue at the five biggest lenders surged to a record $71 billion in the first half of 2025, fueled by volatility in equities, FX, and rates markets triggered by tariffs and shifting tax policy. Goldman Sachs reported its best-ever equity trading quarter, while Bank of America and Citigroup posted multi-year highs. Executives from JPMorgan and Morgan Stanley suggested this trading boom may prove sustainable—even as traditional dealmaking remains well below 2021 peaks.

Crypto markets rallied alongside legislative momentum. Congress passed three digital asset bills—including the GENIUS Act and CLARITY Act—sending Ethereum up more than 20% on the week as investors welcomed the clearest regulatory framework yet. With earnings season heating up, Fed policy on pause, and trade risks rising, markets are bracing for a choppier path ahead.

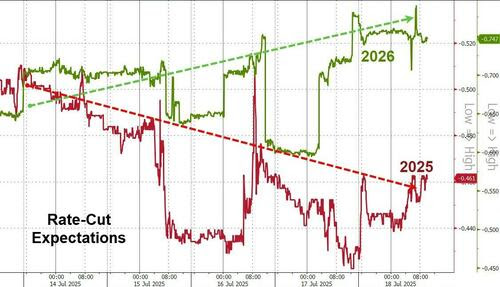

Powell Panic Reversed, but Rate-Cut Hopes Keep Fading

Markets opened the week with a jolt after reports leaked that President Trump was preparing to fire Federal Reserve Chair Jerome Powell. Stocks sold off quickly, the dollar slumped, and bond yields jumped—reflecting fears that the Fed’s independence was under threat. But the selloff was short-lived: Trump later denied any imminent plans to remove Powell, and markets rebounded just as fast, highlighting how fragile confidence remains when it comes to the Fed’s political standing.

Still, the episode deepened skepticism around rate cuts. Fed Governor Waller’s earlier case for a July cut lost traction as strong economic data rolled in: retail sales beat expectations, business sentiment jumped, and wage growth remained firm. Meanwhile, the University of Michigan’s inflation expectations dropped slightly—but stayed well above levels consistent with the Fed’s 2% target. As a result, traders now expect fewer than two rate cuts in 2025, down from nearly four just two months ago.

CPI Comes in Soft, but Tariff Impact Grows Ahead of Fed Decision

June Consumer Price Index (CPI) came in cooler than expected, with core prices up just 0.2%—marking the fifth straight month of tame core inflation. Still, signs of tariff pass-through are beginning to emerge: categories like toys, appliances, and furnishings saw their fastest price increases in years, even as car prices fell.

Markets now overwhelmingly expect the Fed to hold rates steady on July 30, with odds of a September cut rising modestly.

Trump responded by calling for immediate cuts: “Consumer Prices LOW. Bring down the Fed Rate, NOW!!!” But with tariffs still set to rise in August and the Fed’s preferred gauge (core PCE) due July 31, policymakers are unlikely to rush. For now, institutional credibility—not just inflation—is on the line.

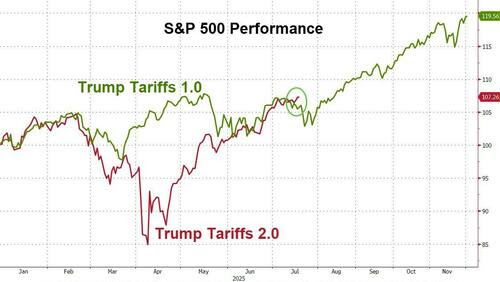

Trump’s Tariff Blitz Sets Countdown in Motion

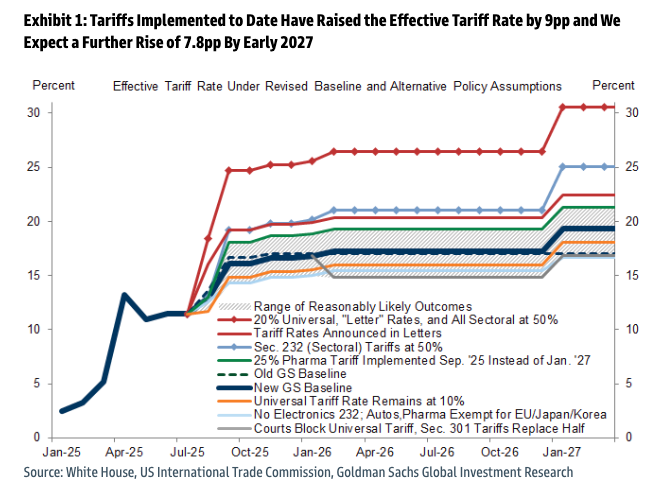

President Trump confirmed this week that formal tariff letters have been sent to over 150 countries, warning of blanket import levies ranging from 10% to 15% starting August 1—unless new deals are secured. Key allies such as the EU, Japan, South Korea, Canada, and Mexico are already on the clock, while talks with India and China are still unresolved. Markets, once expecting a delay, are now beginning to price in real policy risk, as Goldman Sachs raised its effective tariff forecast.

Confidence in a potential China deal took a hit Thursday when the Commerce Department announced a 93.5% anti-dumping duty on Chinese graphite, bringing the effective tariff on this key battery material to 160%. That move signals a tougher stance heading into final negotiations—and poses a direct threat to EV makers, battery manufacturers, and energy storage developers reliant on Chinese inputs.

Graphite alone is expected to add $7 per kilowatt-hour to EV battery costs—roughly $700 extra for a standard 100 kWh battery—wiping out a significant portion of profit margins and undercutting the value of tax credits from the Inflation Reduction Act. If implemented, the tariffs would impact a broad swath of industries—from consumer goods and autos to renewables and semiconductors—raising costs and potentially reigniting inflation just as growth slows. One company seems a potential target of this policy shift: Elon Musk's Tesla. Once the President's bro, Elon's looking a lot more like the foe - and this policy shift could be a shot across the Tesla bow to quiet Musk's anti-Trump posts on X lately.

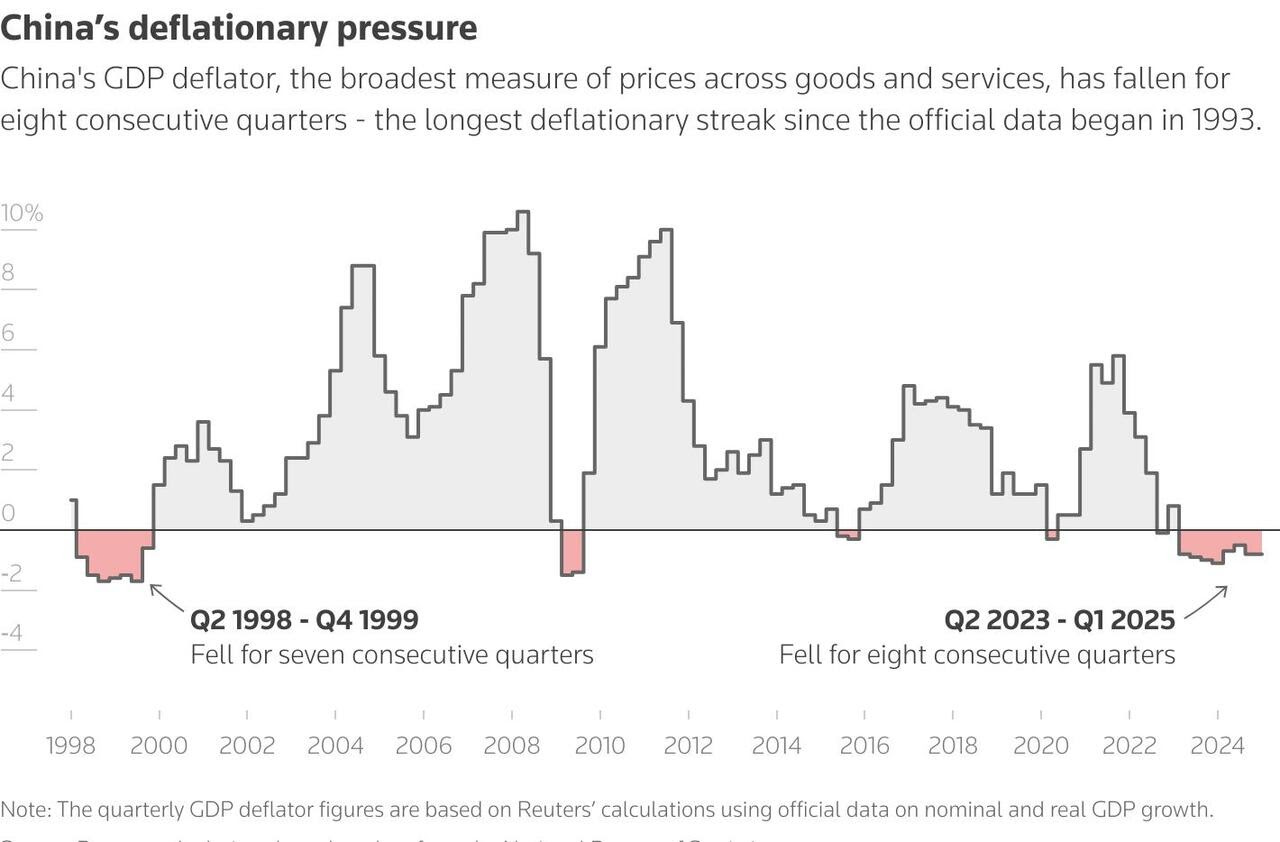

Stagflation Risk Returns—And China Isn’t Helping

Even before Trump’s tariff wave, developed economies were flashing early stagflation signals. In Europe and Japan, growth remains fragile while real interest rates creep higher. The eurozone just posted its third straight month of negative retail sales growth, and Germany’s manufacturing PMI remains in contraction. Japan’s wage growth is stalling, even as energy prices rebound. Central banks are increasingly boxed in—fighting inflation that may soon be tariff-driven while growth stays muted. The global economy is entering Q3 with weaker growth, stickier prices, and rising trade barriers—an environment ripe for policy error.

China’s Collapse Is Reshaping Global Capital Flows

China’s property crisis has metastasized into a broader confidence collapse, with Kyle Bass calling it “the largest macro imbalance in the world.” A slow-motion banking crisis is underway, driven by collapsing collateral, tightening capital controls, and a growing flight to safety. But instead of stimulating aggressively, China is opting for surveillance over stimulus—accelerating capital outflows.

That capital isn’t disappearing; it’s landing in the U.S. U.S. Treasury bonds have seen rising foreign demand because the dollar remains the world’s only deep, liquid refuge. In effect, China’s slowdown is doing the Fed’s job for it—pulling down bond rates as rising demand drives bond yields down.

For investors, the key takeaway is that China is no longer a growth partner but is instead a source of systemic risk. The U.S. may be the relative winner in a capital flight scenario, but deteriorating global demand could start to bite. Markets may be rallying on safe-haven inflows today, but the long-term fallout from a structurally weaker China is just beginning to show.

Bitcoin Gets the Bill: Crypto Surges as Congress Clears Pro-Market Reforms

In a landmark week for digital assets, Congress passed three major bills—the GENIUS Act, the Anti-CBDC Act, and the CLARITY Act—sending them to President Trump’s desk and reigniting a surge across the crypto complex. Bitcoin topped $120,000, Ethereum broke above $3,600, and XRP spiked to a year-to-date high, lifting total crypto market cap back above $4 trillion.

This rally isn’t driven by hype—it’s being written into law. The GENIUS Act establishes a reserve-backed framework for stablecoins, while the CLARITY Act outlines clear boundaries for regulatory oversight between the SEC and CFTC. The Anti-CBDC Act blocks the creation of a government-run digital dollar—shutting down what many view as a direct threat to decentralized currencies. With bipartisan support and direct backing from the Trump administration and Treasury Secretary Scott Bessent, the bills mark the clearest pro-crypto stance yet from Washington.

Catalyst Watch:

Trump is preparing an executive order that would open 401(k) plans to alternative assets like Bitcoin, metals, and private funds—potentially unlocking trillions in long-term demand. The order would direct federal agencies to clear the path for crypto in retirement portfolios, signaling a policy shift that could integrate digital assets into the core of American household savings.

Crypto is being woven into the fabric of U.S. financial policy.

****This chart shows a record-breaking surge in Ethereum ETF inflows, with nearly $727 million added in a single day. The spike, led by iShares ($499M), marks the strongest institutional demand since launch—driven by crypto legislation momentum and growing investor confidence.****

Last Week's Market Performance

The S&P 500 rose +0.6% and the Nasdaq +1.5%, both closing at new record highs, while the Dow slipped -0.1%. Resilient bank earnings and soft inflation data offset growing concerns around tariffs and central bank independence. JPMorgan and Bank of America described the U.S. economy as “resilient,” while Netflix rallied on strong subscriber growth.

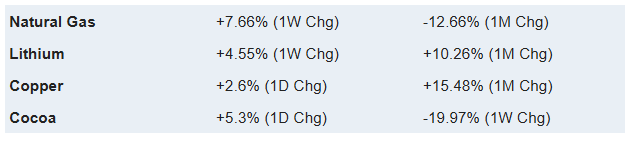

- Commodities: Crude oil fell -1.6% to $67.34/bbl. Gold dipped -0.2% to $3,358/oz. Natural gas surged +7.6%.

- Top Gainers: Invesco (+14%), Warner Bros. Discovery (+9%), Albemarle (+9%), Coinbase (+8%), First Solar (+8%)

- Laggards: Elevance Health (-19%), Waters (-19%), Molina Healthcare (-17%), Centene (-11%), Schlumberger (-11%)

- Sectors: Tech led with +2.1%, followed by Utilities (+1.6%) and Industrials (+0.8%). Healthcare (-2.6%) and Energy (-3.9%) lagged.

- Global: Hong Kong rallied +2.8%, China +0.7%, Japan +0.6%. India (-0.9%) and France (-0.1%) declined.

- FX & Crypto: Ethereum soared +22.2%, XRP +26.2%, Litecoin +10.2%, Bitcoin +1%. The dollar gained vs. EUR (-0.55%) and GBP (-0.68%).

Upcoming Events This Week

Markets will be laser-focused on Q2 earnings this week, with heavyweights including Alphabet, Tesla, IBM, Coca-Cola, T-Mobile, Raytheon, Lockheed Martin, and Blackstone set to report.

On the economic front, key U.S. data includes durable goods orders, PMIs, and home sales, while Fed Chair Jerome Powell speaks Friday. Globally, eyes are on ECB, Turkey, and Russia rate decisions.

.png)

Company News

LevelFields AI Stock Alerts Last Week

Victory Capital (VCTR) +9.8% on S&P 600 Inclusion

Victory Capital Holdings rallied nearly 10% after S&P Dow Jones Indices announced the stock will be added to the S&P SmallCap 600. Index inclusion often sparks buying from funds tracking the benchmark, and the move reflects improving fundamentals and market capitalization strength.

The Trade Desk (TTD) +14.7% on S&P 500 Promotion

The Trade Desk soared almost 15% on news it will join the S&P 500. The upgrade boosts institutional demand and validates the ad-tech firm’s scale and profitability. Investors are betting the inclusion will drive sustained inflows and momentum as passive funds rebalance.

China Targets EV Price Wars

China is cracking down on price-cutting in its electric vehicle sector as deflation risks rise and industrial profits shrink. At a State Council meeting led by Premier Li Qiang, officials vowed to shift automakers away from unsustainable discounts and toward higher quality, innovation, and better financial discipline.

EV prices have plunged since 2023, dragging down consumer inflation and raising alarms over knock-on effects in upstream industries like steel and battery materials. Cars have now weighed on China’s CPI for three consecutive years.

Stabilized pricing would support Tesla’s margins, which have been hit by aggressive discounting in China. But with competition still fierce and policy possibly favoring domestic firms, Tesla’s pricing power remains fragile in its second-largest market.

Netflix Lifts Forecast as Revenue and Cash Flow Surge

Netflix topped Q2 estimates and raised its full-year revenue and free cash flow guidance, driven by strong subscriber growth, higher pricing, and momentum in ad sales. Revenue climbed 16% YoY to $11.08 billion, narrowly beating expectations, while net income rose to $3.1 billion, or $7.19 per share. Free cash flow jumped 91% YoY to $2.3 billion, prompting an upward revision to the 2025 target range of $8–8.5 billion. Netflix credited currency tailwinds, solid member retention, and growing advertising revenue—but warned that H2 margins will dip due to heavier content and marketing spend.

While subscriber figures were withheld again, upcoming content includes major releases like Stranger Things, Wednesday Season 2, and Happy Gilmore 2. Shares dipped ~5% on Friday as investors digested the margin forecast despite the strong topline beat.

.png)

How this Unknown Stock Rose 1,000%

Turning $10,000 into a $63,000 Profit

Investors Ditching Big Banks for AI-powered Wealth Managers

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai