.png)

Macrosynthesis

TLDR: Markets Buckle After Tariff Shock, Cloud Rate Outlook

Markets reopened Monday still buzzing from Trump’s $4.2T “Big Beautiful Bill”—but the post-holiday rally didn’t last long. What followed was a dose of trade anxiety. On Truth Social, Trump published formal tariff threat letters to Japan and South Korea, confirming 25%–40% duties set to hit Aug. 1. By midweek, that list had grown to include copper (50%), Canada (35%), and rumors of similar moves on pharma and autos. Traders, who just days earlier had been relieved by the tariff delay to August, suddenly found themselves repricing risk—again.

Stocks stumbled as momentum cracked and Fed speak turned hawkish. Rate-cut hopes, which had been clinging to soft private payrolls and low inflation, faded after several FOMC members signaled caution. Reports late in the week that Jerome Powell may consider stepping down only added to the policy fog. Meanwhile, earnings season kicked off with Delta Airlines offering a rare dose of optimism—booking strength and upward guidance—though broader expectations for Q2 remain tepid.

Across asset classes, the story was different. Bitcoin broke above $118K, silver surged past $38 for the first time since 2011, and copper hit record highs as traders scrambled to front-run tariffs. Oil climbed on expectations of a Trump “Russia speech” and second-half supply distortions, while bond yields rose on the long end, steepening the curve. Even gold caught a bid, extending its rebound off the 50DMA. If last quarter was the melt-up, this one might be the volatility.

Last week marked the collision of Trump’s Big Beautiful Bill with his reloaded trade war. Add a hawkish Fed and fading rate-cut euphoria, and Q3 is shaping up to be anything but quiet.

Tariff Blitz Returns

Trump’s latest tariff push brings trade threats near “Liberation Day” levels, targeting over two dozen countries with sweeping hikes: 30% blanket tariffs on all imports from Mexico and the EU, 35% on Canada, and a 50% levy on copper. Brazil, Japan, South Korea, and others are also in the crosshairs after the failure of Trump’s “90 deals in 90 days” initiative. While markets remain relatively calm—seeing this as typical “TACO trade” behavior (Trump Always Chickens Out)—the scale and breadth are much wider than before.

Copper tariffs are particularly significant for U.S. equities. They squeeze margins for companies like Vertiv (VRT), which relies heavily on copper for power and cooling infrastructure in data centers, and for EV makers, where copper is critical to batteries, motors, and wiring harnesses. Meanwhile, a 30% tariff on Mexican imports would sharply raise costs on fruits, vegetables, and auto parts, hitting both grocery prices and just-in-time manufacturing. Canadian tariffs also raise pressure on aluminum and lumber inputs, adding strain to housing and auto sectors.

Although investors have yet to price in the full risk—treating the threats as negotiating tactics rather than policy—the announced tariffs mirror the initial April levels that spooked markets before being suspended. If these measures are implemented by the August 1 deadline, the calm could quickly break, triggering a broad revaluation across sectors tied to global trade and cheap inputs.

Fed Turns Cautious as Tariff Fog Thickens

The Federal Reserve’s stance is shifting—from patient to concerned. While official policy remains on hold, the tone out of central bank corridors this week suggests that rate cuts are slipping further from view as trade tensions mount. Chicago Fed President Austan Goolsbee warned that Trump’s rolling tariff shocks have created “messy” conditions for interpreting the economic data, with rising business anxiety around inflation that hasn’t yet shown up in the numbers. His message was clear: the Fed can’t chart a path forward if every six weeks it’s bracing for a new supply shock. Meanwhile, Governor Christopher Waller—considered a leading candidate to replace Jerome Powell—reaffirmed his call for balance sheet reduction but stopped short of joining the broader hawkish pivot, reiterating his belief that the fed funds rate remains too tight. Still, his dovish minority view is losing traction.

The latest dot plot showed a split FOMC, with a growing bloc favoring no cuts in 2025. And Powell? Though silent this week, the swirl of resignation rumors and growing speculation about his replacement have only heightened the political pressure on the institution. With Trump publicly attacking the Fed for costing the U.S. “$900 billion a year” in interest and insiders like Kevin Hassett and Scott Bessent jockeying for control, the stakes are no longer just about rates—they’re about credibility. For now, the Fed is signaling it will stay put, watching the trade situation evolve before risking a move that could either inflame inflation or appear politically coerced. But the clock is ticking, and as one strategist put it, the longer the Fed waits, the harder it will be to act without market turbulence..

The Issue of Easing at the Top

Calls for interest rate cuts have intensified in recent weeks—even as equity markets hover near record highs and the economy shows signs of resilience. President Trump has publicly advocated for lower rates, framing them as necessary to support growth amid global uncertainty and tariff-related headwinds. While this may appear at odds with strong market performance, it reflects a broader political and economic debate about the role of monetary policy in today’s environment.

From a policy standpoint, the Federal Reserve faces a complex challenge. Despite a federal funds rate near 5%, many financial indicators suggest that monetary conditions are not especially restrictive. Credit remains accessible, labor markets are tight, and consumption—while under pressure—has remained relatively stable. Inflation has moderated from 2022 highs, not primarily due to demand destruction, but because pandemic-era supply disruptions (in energy, shipping, and semiconductors) have largely unwound.

The key question now is whether growth is genuinely slowing or simply normalizing. Unemployment remains low, wage growth is sticky, and market speculation continues—hardly signs of a credit-constrained economy. In that context, rate cuts could risk overstimulating an already warm system.

This is where policy timing becomes critical. Rate reductions are typically deployed to cushion downturns—not to accelerate markets already pricing in aggressive fiscal stimulus. With substantial tax incentives, tariff revenues, and defense spending already boosting demand, layering on monetary easing could risk reigniting inflation rather than stabilizing the cycle.

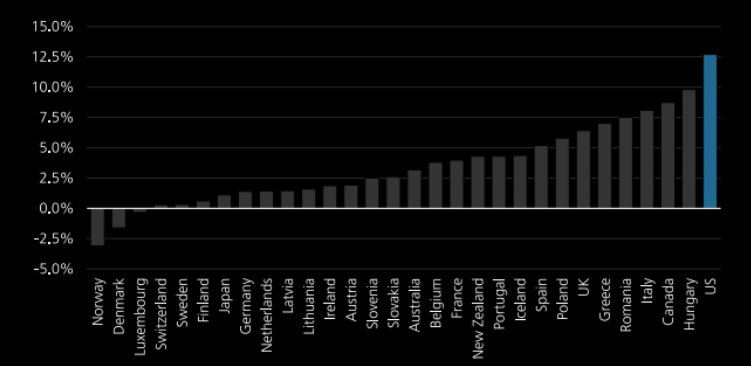

The chart below illustrates why rate policy is drawing scrutiny. U.S. interest payments as a share of GDP now exceed 12.5%—well above global peers. This dynamic adds pressure on policymakers to find ways to reduce borrowing costs. But using interest rate policy to address fiscal burdens carries risks. If cuts are made prematurely, the economy could overheat just as inflation appears to be stabilizing. The data suggests a cautious approach is warranted—even as political and market voices grow louder.

Powell vs. Trump: More Theater Than Threat—But the Stakes Are Real

The public tension between President Trump and Fed Chair Jerome Powell has drawn national attention, but the deeper issue transcends policy disagreements or personalities. What’s at stake is the perceived independence of the Federal Reserve—a cornerstone of U.S. financial credibility.

The Fed was designed to be insulated from short-term political cycles, with leaders appointed for staggered terms and a dual mandate focused on price stability and employment—not electoral outcomes. This structure ensures that interest rate decisions are guided by long-term macroeconomic data rather than shifting political agendas.

But recent headlines—ranging from public criticism to replacement rumors—risk undermining that perception. If markets begin to believe the Fed is steering policy to appease political actors, the consequences could ripple far beyond Washington.

For U.S. equities, the implications would be substantial:

- Valuations could decline as investors price in greater policy volatility and inflation uncertainty.

- Risk premiums would rise, especially in rate-sensitive sectors like tech and REITs.

- Institutional capital could retreat, particularly foreign inflows that depend on confidence in U.S. monetary governance.

- Dollar instability might erode multinational earnings, tightening financial conditions even without Fed action.

Importantly, this risk isn’t partisan. Any future administration—left or right—could be tempted to steer monetary policy toward short-term political goals. That’s why institutional independence is vital: it acts as a guardrail against reactionary policymaking and protects the Fed’s credibility in global markets.

JPMorgan CEO Jamie Dimon recently summed it up: “The Fed’s independence is essential for maintaining economic stability… attempts to influence its decisions are likely to have minimal effect—but the perception of interference could still be damaging.”

While political tension with the Fed is nothing new, efforts to reshape or pressure the institution—especially amid global economic uncertainty—introduce structural risks that markets cannot ignore. The real concern isn’t today’s dot plot or tomorrow’s CPI print. It’s whether the Fed will still be seen as a credible, independent actor when the next real crisis hits.

Last Week's Market Performance

U.S. stocks edged lower from record highs, with the S&P 500 down -0.3%, the Dow -1%, and the Nasdaq -0.1%, as Trump escalated tariff threats—including 50% on copper and up to 200% on pharmaceutical imports.

Markets held near all-time highs, buoyed by Delta’s strong earnings and Nvidia (NVDA) becoming the first company to surpass a $4 trillion market cap.

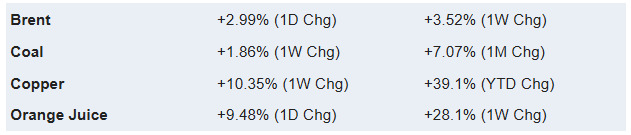

- Commodities: WTI crude surged +3% to $68.45/bbl. Gold rose +0.5% to $3,364/oz. Natural gas fell -2.2%.

- Top Gainers: Delta Air Lines (+11%), Moderna (+10%), PTC (+10%), AES Corp (+9%), Tapestry (+9%)

- Laggards: Fair Isaac (-17%), First Solar (-12%), Datadog (-11%), Autodesk (-11%), ServiceNow (-10%)

- Sectors: Energy (+2.5%) led, followed by Utilities (+0.8%) and Real Estate (+0.6%). Financials (-1.9%) and Consumer Staples (-1.8%) lagged.

- Global: Germany (+2%) and France (+1.7%) outperformed; India (-1.1%) and Japan (-0.6%) declined.

- FX & Crypto: Bitcoin rallied +8.5%, Ethereum +17.9%, XRP +26.5%. USD gained across the board.

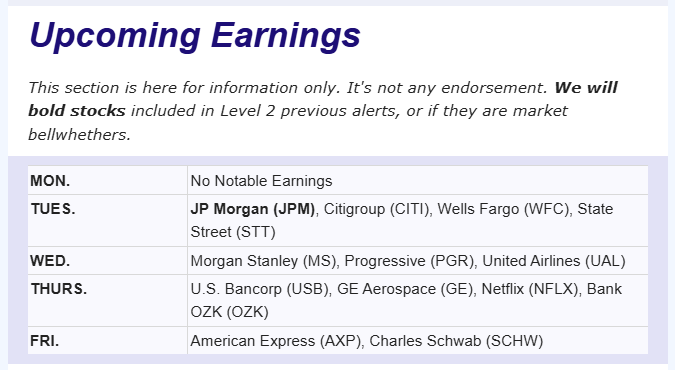

Upcoming Events This Week

Markets face a pivotal week as Trump’s next round of tariff letters—likely including the EU—keeps trade risks elevated. Earnings season ramps up with reports from JPMorgan, Goldman Sachs, Netflix, ASML, and TSMC. On the data front, U.S. CPI is expected to rise while retail sales stall. Europe eyes industrial output and trade data, the UK reports inflation, and China’s Q2 GDP is expected to hold above 5%.

.png)

Company News

LevelFields AI Stock Alerts Last Week

ILPT +14% on Dividend Hike, +20% Weekly Rally

Industrial Logistics Properties Trust (ILPT) surged 14% in a single session and closed the week up nearly 20% after its Board of Trustees announced a fivefold increase to its quarterly dividend—from $0.01 to $0.05 per share. The $0.20 annualized payout signals growing confidence in cash flow stability amid improving industrial REIT fundamentals.

Genius Group (GNS) +12.9% on Buyback, +21% Weekly Gain

GNS jumped 12.86% intraday and over 21% for the week after approving a 20% share repurchase program and confirming it had already bought back 1 million shares. The move comes amid ongoing restructuring efforts and aims to counter dilution concerns while reinforcing management’s long-term outlook.

Earnings Season Kickoff: Tariff Risks Cloud Q2 Outlook Despite AI Optimism

Earnings season begins in full next week with JPMorgan, Goldman Sachs, and Bank of America leading a wave of reports. But expectations have been cut sharply. Since March, projected S&P 500 earnings for Q2 have dropped from $234 to $220 per share—a larger cut than usual. The main reason: growing concern over tariffs. Trump’s recent trade threats, including the now-expired July 7 “pause,” have caused uncertainty for global companies. Analysts warn that rising tariffs could take a real bite out of profits, especially in manufacturing, retail, and other trade-exposed sectors.

Slowing consumer spending is another issue. Since consumer activity drives most company revenue, weaker household demand is putting pressure on earnings. Signs of stress—from slower job growth to rising credit delinquencies—are beginning to show. The energy and materials sectors are already reflecting that, with profits down nearly 20% and 12% from last year, respectively. But tech continues to buck the trend. Companies like Nvidia, Microsoft, and Google are expected to post strong results, thanks to ongoing investment in AI and digital infrastructure, which are still going strong even as the rest of the economy cools.

Investors are reacting accordingly. Many are trimming riskier positions and adding to steady, dividend-paying names like Procter & Gamble, Berkshire Hathaway, and Visa. After a sharp rebound in stocks in June, expectations are high—possibly too high. If companies miss earnings or guide lower for the rest of the year, stocks could drop quickly. That’s why investors will be listening closely not just to the numbers, but to the tone of executive commentary. Any hint of caution from big players like TSMC, Johnson & Johnson, or Netflix could move markets.

Q2 is shaping up as a test of how much longer tech can hold up the market while the rest of the economy slows. Trade policy, interest rates, and weaker consumer demand are all real risks. But strong tech earnings and cautious positioning may still offer support—if the surprises stay mild.

Delta Reinstates Guidance, Premium Demand Lifts Sector

Delta (DAL) soared 12% after reporting Q2 EPS of $2.10 on $15.5B revenue, topping estimates and reinstating full-year guidance of $5.25–$6.25—above the $5.38 consensus but below its prior $7.35+ target. Strength came from a 5% YoY gain in premium travel, now a majority of high-margin revenue, while main cabin sales fell 5%. CEO Ed Bastian cited resilient corporate bookings and loyalty spend despite tariff noise.

The results fueled a sector-wide rebound—United and American each gained 12%, JetBlue 7%—but also underscored a K-shaped travel recovery. Higher-income and business flyers are returning, while budget demand remains weak. Delta plans to cut post-summer capacity to preserve pricing. With 59% of Q2 revenue from premium, cargo, loyalty, and maintenance, Delta’s model stands apart from more price-sensitive rivals.

Vertiv (VRT) -14%: Tariff Hit and AWS Cooling Surprise Shake AI Play

Vertiv stock plunged 14% after two major blows: Trump’s new 50% copper tariff, which threatens input costs, and Amazon’s unveiling of its own in-house liquid cooling system. The copper move could hit Vertiv’s margins if costs can’t be passed on—especially in the crowded AI infrastructure market. Meanwhile, AWS, a key customer, launched custom cooling tech for its GB200 servers, potentially cutting out suppliers like Vertiv. While only 1–2% of revenue is directly at risk, the move signals a broader trend of hyperscalers internalizing infrastructure—undermining Vertiv’s premium valuation.

Drones Surge on Pentagon Shift, Tariffs Add Tailwind

Defense stocks rallied after the Pentagon scrapped sourcing restrictions and fast-tracked U.S. drone procurement. AeroVironment and Kratos jumped 11–12% as the DoD pledged to buy hundreds of U.S.-made systems and integrate drones into combat training by 2026. The move favors domestic players just as 30% tariffs on EU/Mexico and 50% copper duties raise costs for foreign rivals. The twin policy shifts boost near-term demand and onshoring incentives, making U.S. drone makers key beneficiaries—if they can scale profitably.

.png)

Bumble Swipes Left on Employees, Rallies 30%

Tesla's Robotaxi Launch - How it Really Went

Lockheed Martin's Having a Great Year

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai