.png)

Macrosynthesis

TLDR: Record Highs as Speculation Surges, Trade Deals Ease Tariff Jitters

Markets pushed higher again this week, with the S&P 500 notching its fifth consecutive record close—its longest streak in over a year—fueled by AI momentum, strong earnings, and easing trade tensions ahead of the August 1 tariff deadline. The Dow rose 1.3%, the Nasdaq added 1.2%, and the S&P gained 1.6%, capping a week where bullish sentiment met a speculative undercurrent. President Trump reached new trade agreements with Japan, Indonesia, and the Philippines, while talks with the EU and Canada intensified, helping to wring out some of the geopolitical risk premium.

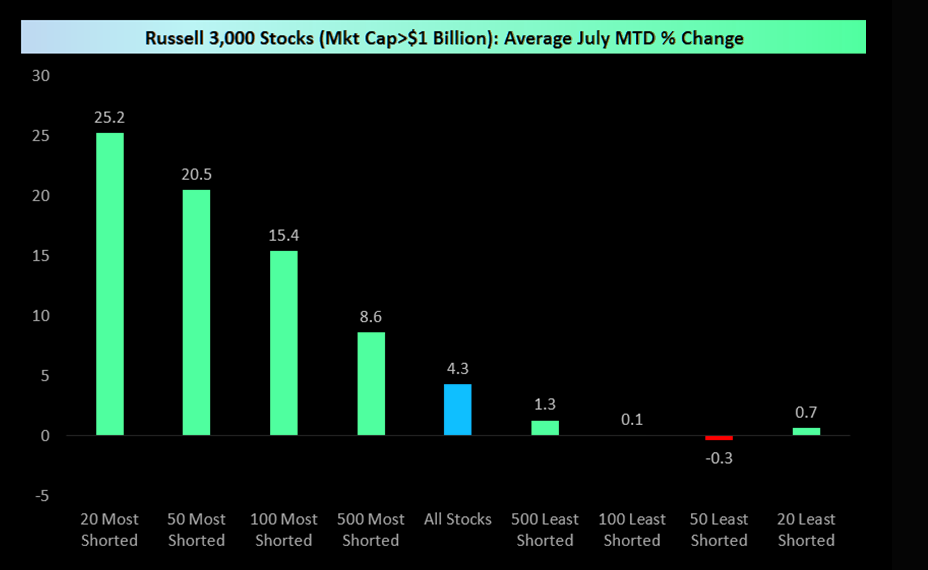

Retail investors leaned in aggressively, driving a sharp rally in heavily shorted stocks and dominating call option volume, while hedge funds quietly de-grossed positions for a seventh straight session. Alphabet’s earnings helped solidify the AI investment theme, but Intel’s disappointing outlook reminded markets that not every tech name rides the same tailwinds. Beneath the surface, cracks emerged: economic data showed sluggish real consumption and softening labor trends, prompting a growing chorus of Fed officials to raise concerns ahead of next week’s FOMC meeting. With Powell under mounting political pressure and mega-cap tech earnings looming, markets are heading into a pivotal week where momentum meets macro.

Japan Bows Low, but the Cracks Show

The U.S.–Japan trade deal landed with fanfare this week, cutting tariffs from 25% to 15% and sending Japanese equities soaring—Toyota posted its best day since 1987, and the Topix neared all-time highs. But beyond the market reaction, the agreement laid bare the deep structural fragility of Japan’s economy. Facing mounting U.S. pressure and reeling from a crushing election loss, Prime Minister Ishiba signed off on sweeping concessions—including tariff relief on autos and agriculture and a highly publicized $550 billion investment pledge. That pledge, notably, comes with a twist: President Trump has broad discretion over how the funds are allocated, a detail that has sparked concern in Tokyo.

Japan’s willingness to concede so quickly reflects just how strained the foundation has become. GDP growth remains anemic at just 0.6% year-over-year, and public debt has ballooned past 230% of GDP. Demographics continue to deteriorate: the population shrank again in 2024, the fertility rate has dropped to 1.14 children per woman, and the government is now offering monthly subsidies and even housing incentives to get families to relocate and reproduce. Meanwhile, Japan’s global financial clout may be weakening. The tariff deal is expected to reduce the country’s trade surplus, which means less money to invest abroad—posing a longer-term headwind for global bond and currency markets.

One casualty could be the yen itself. Long prized for the “yen carry trade”—a strategy where investors borrowed cheaply in yen to invest in higher-yielding assets abroad—the currency is now losing appeal. As rates rise and political risk grows, that reliable stream of global demand for the yen is starting to dry up. At the same time, Japanese bond markets are flashing red: 30-year yields surged to record highs this week, raising fears that the decades-long period of ultra-cheap government borrowing is coming to an end. While the Bank of Japan is now signaling earlier rate hikes, fiscal pressure and political instability are complicating its next move. For now, Japan has secured short-term relief—but at the cost of revealing just how fragile its economic position has become.

Europe Next in Line

While Japan struck a deal, Europe is still holding its breath. On Sunday, European Commission President Ursula von der Leyen is set to meet President Trump at his Turnberry resort in Scotland for what may be the EU’s final shot at avoiding sweeping 30% tariffs on exports to the U.S. Negotiators have spent months trying to craft a compromise, reportedly landing on a proposal for 15% tariffs across most sectors—with carveouts for aviation, medical devices, and some industrial goods. But as with past deals, the outcome now hinges on Trump, who has publicly pegged the odds of an agreement at “50-50.”

The stakes are enormous. Without a deal, the EU is prepared to hit back with matching tariffs on up to €100 billion of U.S. exports, including Boeing aircraft, bourbon, and American-made cars. But retaliation is a blunt tool, and even European officials admit that the real leverage lies with Washington. Beyond tariffs, the two sides are also negotiating over digital trade, defense procurement, and energy partnerships—areas where any concessions could reshape transatlantic relations for years. The EU, like Japan, is learning to navigate a world where access to the U.S. market increasingly comes with strings attached—and the risk of going it alone is rising.

Ukraine’s Internal Crisis Clouds EU Aid

As Europe negotiates tariff relief abroad, it’s facing an unexpected storm at home—this time, from Kyiv. Just as Ukraine was set to receive a major tranche of financial support, President Zelensky stunned Western allies by signing legislation that places Ukraine’s anti-corruption bureau and prosecutorial office under presidential control. The law was rushed through after raids on the bureau’s headquarters, triggering nationwide protests and sharp editorials from outlets like Bloomberg and The Economist, which called the move “sinister” and warned of a dangerous erosion of democratic oversight.

The timing couldn’t be worse. According to Hungarian Prime Minister Viktor Orbán, nearly 20% of the EU’s proposed seven-year budget was earmarked for Ukraine, with another 10–12% dedicated to servicing debt from past aid. The revelation sparked backlash from member states like Germany and has fueled a broader revolt over transparency and fiscal accountability in Brussels. Orbán minced no words: “The EU budget has only one obvious purpose—to bring Ukraine into the EU, and these funds are transferred to Ukraine.”

That backlash is now turning into action. Though not formally announced, the EU has quietly hit pause on additional aid to Kyiv. Officials insist it’s a reassessment, not a reversal—but the shift is clear. Europe’s political calculus has changed, and financial support is no longer guaranteed. With internal governance under scrutiny and battlefield conditions still fluid, Ukraine faces a growing dilemma: without reforms, even its staunchest allies may start to walk. European defense stocks sold off last week in response.

Markets Soar on Earnings… But the Risk-On Fever Is Getting Dangerous

Even as Ukraine aid stalls and EU unity frays, Wall Street is charging ahead—at least on the surface. This earnings season has been one of the best in years: nearly 84% of S&P 500 companies are beating profit expectations, and 79% are topping revenue forecasts. EPS revisions have surged, margins are expanding beyond big tech, and nearly two-thirds of firms are beating by more than a standard deviation. On paper, corporate America is in top shape.

Tech is still leading the charge, with Google’s AI spending spree powering the "gold rush for compute," but there’s a growing sense that markets are ready to differentiate between good AI capex and hype-driven burn rates. Microsoft, Meta, Amazon, and Apple all report next week—if they miss, sentiment could sour quickly.

Meanwhile, the risk-on mania is back. Speculation has roared back to 2021 levels. Call options dominated July volumes, sub-$1 stocks are exploding, and speculative baskets built around meme stocks and AI-adjacent themes are hitting fresh highs. Yet market breadth is weak, hedge funds are net sellers, and momentum has broken down globally. The same kind of pattern preceded major reversals in 2020 and 2022.

There’s still a fundamental bid—buybacks are up, capex is rising, and revenue per employee just hit a record. But real consumption has flatlined for six months, industrials are rallying more on hope than data, and a tariff shock from Trump’s pending EU decision could rattle both earnings and inflation expectations.

As one Goldman strategist put it, next week is a “show-me” moment. Big tech, the Fed, and tariffs all collide—and with positioning stretched and volatility cheap, any disappointment could flip the market from melt-up to meltdown.

Markets Defy Tariff Turbulence as Earnings and AI Power Repricing

The S&P 500 just notched its 13th all-time high this year, propelled by a confluence of strong earnings, resilient labor data, and early signs of economic reacceleration. Weekly initial jobless claims have declined for seven straight weeks, and the U.S. composite PMI is quietly trending higher—evidence that the real economy is picking up steam.

Tariffs, once assumed to be a market breaker, have proven less punishing this time around. While the headline tariff rate now hovers near 17%, the effective rate is closer to 8%, thanks to better cost-sharing across global supply chains. Unlike the 2018–19 cycle—when U.S. consumers absorbed up to 90% of tariff costs—this round has seen domestic companies and foreign exporters shoulder nearly two-thirds of the burden. That’s possible because corporate margins are now 60% higher than during the last trade war, giving firms room to absorb shocks without immediately passing on costs. The result: less inflation, steadier sentiment, and a market less prone to panic.

After a wave of pre-emptive guidance cuts in Q1, companies recalibrated. Q2 earnings have surprised to the upside—with nearly 79% of S&P 500 companies beating estimates, and average earnings surprises running 6–7%. From GM absorbing $1.1 billion in tariffs and still beating forecasts, to J&J slashing tariff exposure and raising guidance, the corporate response has been swift and strategic. Even currency trends are cooperating, with a weaker dollar boosting multinational earnings via favorable FX translation.

The deeper story may be structural. Generative AI is no longer just hype—it’s showing up in profit margins and capital allocation. Microsoft now uses AI to write 30% of internal code, saving $500 million a year. IBM credits AI with a 200bps margin expansion, while J.P. Morgan sees a $1–1.5B annual economic impact from internal AI deployment. The “One Big Beautiful Bill Act” is supercharging this momentum, unlocking a projected $360 billion in hyperscaler capex this year alone—funneling into infrastructure, R&D, and domestic buildouts.

The result is a market narrative that’s materially different from 2018 or even 2022. Companies are stronger, margins are wider, AI is lifting productivity, and the tariff shock—while real—isn’t existential. With EPS revisions hitting their highest level in over three years, consumer sentiment relatively stable, and corporate buybacks rising double digits, investors are leaning into strength. Risks remain, but resilience is winning.

Last Week's Market Performance

Wall Street closed out another strong week, with the S&P 500 rising +1.5% to a record 6,389, notching its 14th all-time high of the year. The Dow gained +1.3%, and the Nasdaq rose +1.0%, fueled by upbeat corporate earnings, a $550B trade deal with Japan, and fresh AI optimism.

Commodities: WTI crude sank -3.2% to $65.16/bbl. Gold fell -0.7% to $3,335/oz. Natural gas plunged -12.8% to $3.11.

Sectors: Materials (+2.4%), Industrials (+2.3%), and Healthcare (+3.4%) led. Tech gained just +0.7%, while Staples lagged (flat).

Top Gainers: West Pharmaceutical (+25%), Lamb Weston (+24%), IQVIA (+24%), TE Connectivity (+16%), Baker Hughes (+16%)

Laggards: Charter Comm. (-19%), Texas Instruments (-15%), Fiserv (-14%), LKQ (-13%), Chipotle (-13%)

Global: Japan surged +4.1% on trade optimism. China +1.7%, Hong Kong +2.3%, UK +1.4%. Germany (-0.3%) and India (-0.4%) fell.

FX & Crypto: Ethereum +4.4%, Litecoin +0.4%, Bitcoin -0.3%, XRP -7.8%. USD fell vs EUR (-1%) and JPY (-0.78%).

Upcoming Events This Week

The upcoming week is packed with market-moving events. Trade talks with the EU take center stage, while major tech firms gear up to report earnings. Central banks in the U.S., Japan, and Canada will announce key policy decisions. On the data front, investors will be watching Q2 GDP, the July jobs report, PCE inflation, and ISM manufacturing closely.

.png)

Company News

LevelFields AI Stock Alerts Last Week

Comfort Systems (FIX) +22.3% on Dividend Hike

Comfort Systems USA surged over 22% after announcing a $0.05 increase to its quarterly dividend, bringing the payout to $0.50 per share. The HVAC and electrical contracting firm’s board highlighted strong performance and confidence in long-term growth, fueling investor enthusiasm.

Bitfarms (BITF) +16.8% on Buyback Approval

Bitfarms jumped nearly 17% after unveiling a major share repurchase program. The Toronto Stock Exchange approved the company’s plan to buy back up to 10% of its public float, signaling management’s confidence and adding buying pressure amid broader crypto sector strength.

Boston Beer Pops as Drinking Moves Home

Boston Beer (SAM) rallied over 7% after delivering a second-quarter earnings beat, posting $5.45 EPS vs. $4.04 expected, even as revenue came in slightly light at $587.95M. Shipments fell 0.8% YoY—driven by weakness in Truly and Sam Adams—but pricing power and favorable product mix kept topline growth positive. The results reflect a broader shift in consumer behavior: with economic uncertainty and high bar tabs keeping people in, more Americans are choosing to drink at home. Founder Jim Koch noted “volumes were pressured across the beer industry” as consumers cut back on nights out, yet Boston Beer still grew share. The company reaffirmed full-year EPS guidance of $8 to $10.50 and raised gross margin forecasts on improved brewery efficiency—making SAM a rare winner in a lower-spending, stay-in economy.

Tesla Earnings Miss as Musk Shifts Focus Beyond EVs

Tesla (TSLA) reported Q2 earnings of $0.40 per share—missing already-lowered estimates—while revenue slid 12% YoY to $22.5B, the steepest decline since 2012. Vehicle deliveries dropped, average selling prices fell, and free cash flow collapsed 90% to $146M. Regulatory credit revenue also dropped sharply, and the company offered no updated guidance on vehicle growth. On the earnings call, Elon Musk acknowledged that Tesla faces “a few rough quarters,” citing the phaseout of U.S. EV tax credits and rising competition as headwinds.

.png)

Flying Taxis Taking Off

Hand-sized Military Drones Crushing It

Tesla's True Value Is From This Technology Fueling Everything

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai