.png)

L1 Weekly Stock Market News Analysis

August 24th, 2025

TLDR:

Markets surged after Powell signaled a dovish pivot, sending Treasury yields lower, the dollar tumbling, and gold, crypto, and equities higher. Small caps led gains, while mega-cap tech lagged. At the same time, the U.S. government confirmed a 10% equity stake in Intel, cementing its industrial sovereignty playbook. Geopolitically, Trump met Putin in Alaska, then followed up with Zelensky and European leaders at the White House, where talks focused on security guarantees for Ukraine and the prospect of arranging a direct Zelensky-Putin meeting, possibly followed by a trilateral summit with Trump. Investors now face a landscape where Fed easing, U.S. nationalization of strategic firms, and tentative peace negotiations in Europe are converging to drive both volatility and risk appetite.

Powell’s Jackson Hole Pivot

Fed Chair Jerome Powell used Jackson Hole to set the stage for a policy shift. He left the door open to a rate cut at the Sept. 16–17 FOMC meeting, noting that “the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.”

The speech painted a split-screen economy:

- Labor: Powell said the job market is in a “curious kind of balance,” with both supply and demand for workers slowing. That balance, he warned, carries rising downside risks to employment.

- Inflation: Tariffs are expected to create a “one-time” upward shift in prices, but near-term risks remain tilted to the upside.

- Policy: The Fed quietly scrapped its old framework of targeting inflation “averaging 2%” and only responding to employment “shortfalls.” The new framework is looser, giving the Fed more discretion to move as risks evolve.

Markets heard one thing: Powell is preparing to ease. Treasuries ripped higher with the 2Y yield down 12bps, the dollar broke below key technical levels, gold and Bitcoin rallied back above support, and small caps surged more than 3% on the week. The Dow hit fresh record highs, even as mega-cap tech closed lower.

The Cycle: Debt, Easy Money, and Debasement

Powell framed it as balance of risks—but in practice, it’s the familiar loop:

More Debt → Easy Money (Inflate Your Way Out) → Currency Debasement → Asset Price Inflation.

With U.S. debt north of $35T, rising borrowing costs threaten both growth and solvency. The Fed’s “careful” pivot is less about inflation victory and more about keeping debt service sustainable. Lower rates relieve the Treasury’s load, but at the cost of debasing the currency. That debasement shows up immediately in asset prices—gold, Bitcoin, equities—because investors know the playbook: liquidity first, discipline later.

This cycle rewards asset owners while hollowing out purchasing power. It explains why the Nasdaq trades at 145% of M2 money supply, above dot-com peaks, and why speculation keeps reappearing in meme stocks and crypto. Powell may have spoken of “careful” adjustments, but the market reaction underscored the truth: once again, the U.S. is preparing to inflate its way out of a debt trap.

From Hawkish Minutes to Dovish Powell

What made Powell’s Jackson Hole pivot even more striking is how sharply it contrasted with the FOMC minutes released just 48 hours earlier. Those minutes revealed a Fed still dominated by inflation fears. A majority of participants judged the upside risk to inflation greater than the downside risk to employment, with tariffs flagged as a slow-burn inflationary driver that could keep prices elevated well beyond initial expectations.

Officials highlighted that:

- Rates “may not be far above neutral”—the level of interest that neither stimulates nor restrains the economy—implying the Fed has little cushion left to lean against inflation without tipping growth into contraction.

- Most members expected tariff costs to flow through to consumers, with only modest absorption by foreign exporters.

- Several participants warned of asset valuations already “at the upper end of historical ranges,” suggesting financial instability risks were on the radar.

- Concerns were raised that inflation expectations could “become unanchored” if tariff effects persisted.

In short, the minutes framed inflation as the bigger threat and downplayed employment weakness. Powell, just days later, flipped the emphasis—acknowledging that downside risks to jobs are rising, inflation risks remain, but the “balance of risks” justified opening the door to cuts.

Last Week's Market Performance

Markets swung sharply but closed mixed as Powell’s dovish Jackson Hole comments sparked a late-week rally. The S&P 500 and Dow managed gains, while the Nasdaq slipped on tech weakness. Retail earnings disappointed, with Walmart and Target sliding, but Powell’s signal that downside risks to jobs are rising helped offset losses.

Performance:

- Indices: Dow +1.5%, S&P 500 +0.3%, Nasdaq -0.6%, Russell 2000 +3.4%.

- Sectors: Energy (+2.8%), Real Estate (+2.4%), and Financials (+2.1%) led, while Tech (-1.6%), Telecom (-0.9%), and Consumer Staples (+0.3%) lagged.

- Global: China (+3.5%) outperformed; Japan (-1.7%) fell; Europe posted modest gains.

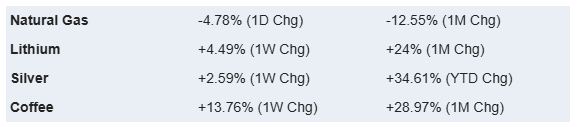

- Commodities: Oil +1.4%, Gold +1.1%, Nat Gas -7.5%.

- FX & Crypto: USD softened; Ethereum (+7.2%) outpaced Bitcoin (-1.3%).

Notables: Dayforce (+31%), Paramount Skydance (+17%), and EPAM (+11%) topped S&P gainers, while Palantir (-10%), Intuit (-8%), and AMD (-5%) were among the biggest losers.

Upcoming Events This Week

Next week’s spotlight stays on the global rates picture as investors test whether Powell’s dovish turn at Jackson Hole has legs. In the U.S., attention will center on personal income, spending, and the PCE inflation gauge, alongside revised Q2 GDP. Markets will also digest durable goods orders for tariff impact, housing and consumer confidence data, and regional Fed indexes.

On the corporate front, Nvidia’s earnings will serve as a key read on AI sentiment after chip stocks lagged broader markets. Abroad, Canada and India release GDP prints, China posts its official PMI, and Japan delivers its end-of-month data slate. In Europe, ECB meeting minutes and fresh inflation numbers from major economies could shape expectations on whether more rate cuts are in play.

.png)

Company News

LevelFields AI Stock Alerts Last Week

Incannex Healthcare (IXHL) +28% on $20M Buyback

IXHL surged 28% in a single session after authorizing a $20 million share repurchase program, signaling management’s confidence in the company’s outlook and capital position.

Rotation Signals: From Tech Titans to Defensive Growth

This week showcased a market in transition. Nvidia and Palantir (down 20% at one point) dragged the Nasdaq to its worst stretch since April, raising questions about whether the AI trade has peaked—at least temporarily. Palantir, still up over 100% year-to-date, became the poster child of the unwind. Nvidia’s stumble carried similar weight, given its role as the market’s single biggest capex barometer.

In contrast, money flowed into small caps, healthcare, and consumer staples—areas that had lagged all year but historically shine when the Fed transitions from hiking to easing. Small caps benefit from falling borrowing costs and greater domestic demand sensitivity. Healthcare and staples, meanwhile, provide earnings stability with room for multiple expansion as real yields decline. Industrials and financials also began to stir, hinting at a broader rebalancing beneath the surface.

Still, the rotation is messy. After Powell’s dovish tone at Jackson Hole, momentum and meme stocks ripped higher into Friday’s close. Opendoor (OPEN), down nearly 20% earlier in the week, finished with a +40% single-day surge, ending deep in the green. The move echoed the retail-driven squeezes of spring, reminding investors that liquidity and speculation haven’t left the system—they’ve just shifted targets.

Taken together, the tape shows two competing dynamics: a slow migration out of overstretched megacaps toward sectors that historically thrive in easing cycles, and a retail frenzy that continues to chase high-beta growth names. If rate cuts arrive in September, expect the rotation into small caps, healthcare, and cyclicals to deepen—but don’t expect the speculative chase to vanish. The two can coexist, fueling volatility at both ends of the market.

Nvidia Earnings: The AI Boom’s Litmus Test

The sector rotation narrative now collides with a crucial event: Nvidia’s earnings this Wednesday. After a choppy week where Nvidia logged its sharpest decline since April, the company faces perhaps the most consequential report of the year—not just for itself, but for the entire AI trade.

Nvidia’s stock has nearly doubled since April, riding the wave of hyperscaler capex pledges from Microsoft, Alphabet, Amazon, and Meta. That surge has left the stock commanding 7.9% of the S&P 500’s weight, meaning any post-earnings swing reverberates through the entire index. Options markets are pricing a ±6% move, which translates to nearly a 0.8% swing in the S&P 500—greater than what traders are bracing for around payrolls or inflation data.

The stakes are simple: if Nvidia beats and guides higher, the AI bull market may regain its footing after weeks of fatigue. A miss—or even “just fine” results—could puncture the AI premium that has carried the Nasdaq to extremes. In that sense, Nvidia’s report is less about one company and more about whether the AI narrative can still justify record multiples in a market hungry for growth catalysts.

.png)

Using AI to Spot Dividend Stocks

Look What Stocks Harvard Univ. is Buying

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai