.png)

L1 Weekly Stock Market News Analysis

August 31st, 2025

TLDR:

Funds are shifting into the seasonal rebalancing phase, with money rotating out of tech after Nvidia’s record earnings failed to spark another leg higher. We’re also heading into September — historically one of the weakest months for equities — just as macro risks are stacking up:

- Fed cuts next month? Markets now see an 85% chance of a September rate cut, but those cuts would arrive in a hot economy: Q2 GDP was revised up to 3.3%, the strongest in nearly two years, while inflation data remains sticky. That tension raises doubts about the Fed’s credibility.

- Tariffs under fire. On Friday, Trump’s tariff program — once projected to raise $500B+ a year and offset his tax cuts — was labeled illegal by an Appeals Court. If struck down, deficits would widen, U.S. credit standing could weaken, and Washington would lose a key fiscal pillar.

- Shutdown risk rising. Federal funding expires September 30. Trump is testing the limits of executive power with a “pocket rescission” that cancels $5B in foreign aid without Congress. Lawmakers warn the move is unconstitutional, and the standoff could tip into a shutdown if no deal is reached.

- Safe havens bid. Gold and silver surged Friday as investors hedged against Fed doubts, fiscal chaos, and inflation risk. The latest PPI print confirmed persistent price pressures, reinforcing demand for metals as a hedge while AI enthusiasm shows signs of entering a digestion phase.

In short: the growth story remains centered on AI, but September brings headwinds. Asset managers are rebalancing capital out of tech and into safer assets. Markets are entering a phase where AI leadership is being tested against rising macro and fiscal risks.

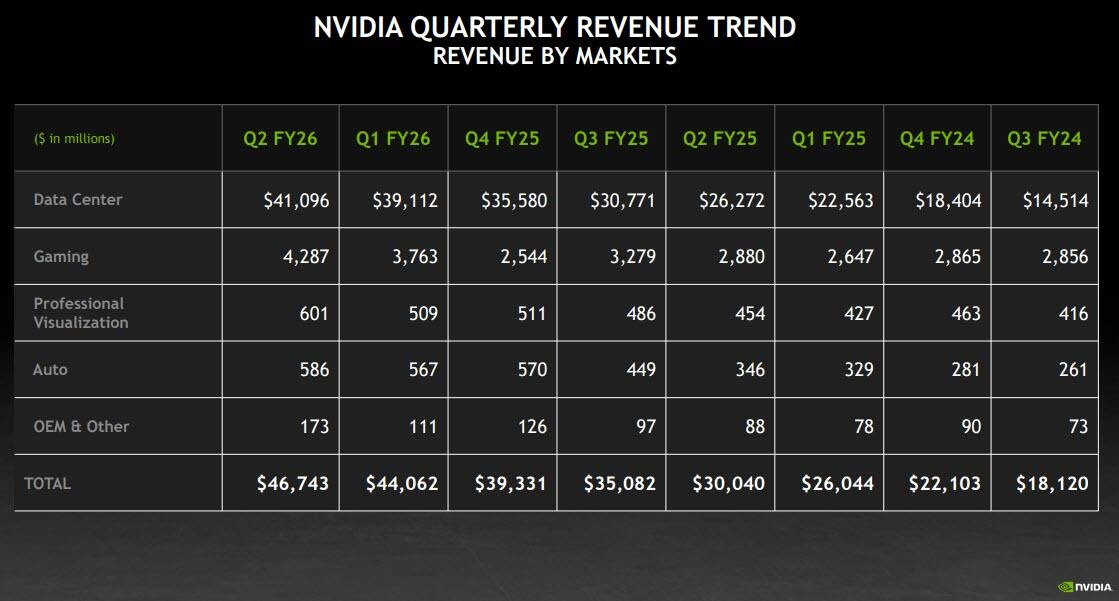

Nvidia Earnings: Record Growth, But Stock Slips

Nvidia once again delivered record-shattering earnings, reaffirming its dominance at the center of the AI revolution. Revenue surged 56% year-over-year to $46.7B, EPS came in at $1.05 versus $1.00 expected, and gaming revenues jumped nearly 50%. Blackwell architecture is ramping quickly, hyperscalers remain half of Nvidia’s data center business, and Wall Street analysts lined up to lift targets—JPMorgan to $215, Truist to $228, KeyBanc to $230.

And yet, the stock fell nearly –5% post-earnings, even after a new $60B buyback authorization. The disconnect captures the market’s anxiety: investors now wonder if the AI capex arms race is showing early signs of fatigue.

Capex Arms Race: The First Signs of Digestion

For the second straight quarter, Nvidia’s data center division—its growth engine—missed expectations despite rising 56% YoY. Inventories and receivables jumped, pointing to possible overbuild as hyperscalers front-load orders. The pattern is familiar: the dot-com fiber boom, the shale surge—periods when spending raced ahead of sustainable demand.

That risk is magnified by the sheer scale of current commitments: tech’s megacaps are set to spend roughly $320B on AI and data centers this year, with about half of that flowing directly to Nvidia. Wall Street’s expectations now demand near-perfection. After two years of triple-digit growth, Nvidia is valued at $4T, makes up 7.5% of the S&P 500, and every earnings print dictates sentiment on the entire AI trade. Even OpenAI’s Sam Altman has warned investors may be “overexcited,” calling parts of AI a potential bubble phase.

CEO Jensen Huang insists demand for Blackwell is “extraordinary,” and long-term the trajectory is intact. But in the near term, investors fear an AI digestion phase—a pause before the next leap. Those worries are amplified by competition: Alibaba’s new inference chip, announced Friday (BABA +13%), shows how quickly rivals are moving to fill the U.S. export void and chip away at Nvidia’s dominance.

The bigger takeaway: the AI trade may be losing its safe-haven status. For months, investors leaned on Nvidia and its peers as the reliable “big return” hedge against macro volatility. But with growth expectations stretched and signs of spending fatigue emerging, that reliability is being questioned—just as the spotlight shifts to the Fed’s own fragility.

Fed Fragility: Cutting Into Strength

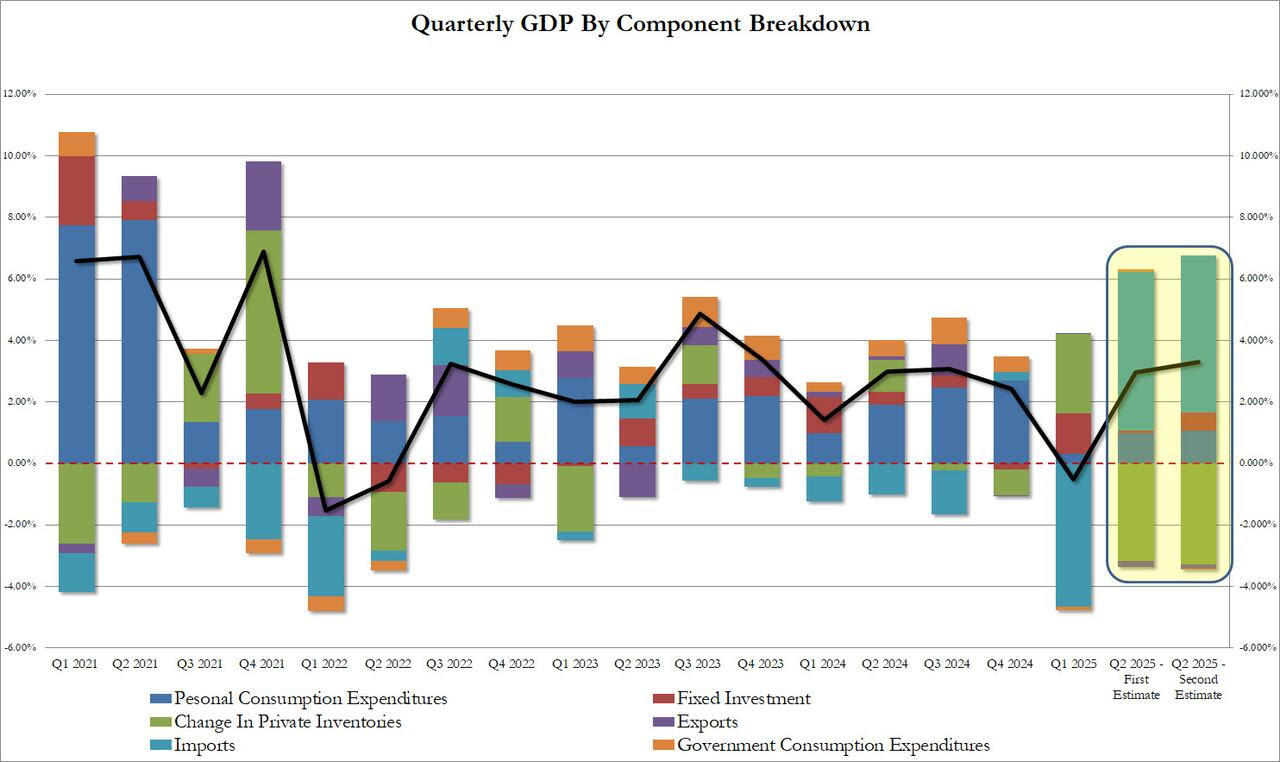

Alongside Nvidia’s blockbuster results, the Fed dominated headlines as markets priced an 85% chance of a September rate cut, with more cuts expected by spring. The catch is that these cuts are colliding with a hot economy: Q2 GDP was revised up to 3.3%, the strongest in nearly two years, powered by consumer spending and a surge in data center investment.

Here’s the situation:

- The Fed’s reverse repo facility, which had served as a huge cash buffer for money markets, is now nearly empty. With that cushion gone, there’s much less slack in the system to keep short-term funding stable if stress flares.

- At the same time, the Treasury is refilling its own cash balance and flooding the market with new bills, which soaks up liquidity and makes funding conditions even tighter.

- Political risk has entered the picture: Trump fired Fed Governor Lisa Cook on Monday, triggering a courtroom showdown Friday. Cook’s lawyers called it a political purge to tilt the Fed, while the White House pointed to mortgage fraud allegations. Either way, the fight reinforced fears that the Fed’s independence is eroding just as its credibility is being tested.

Put together, it leaves the Fed in a bind. Powell is under pressure to cut rates even though growth is strong and inflation risks remain. The added perception of political interference only deepens investor doubts. For markets, rate cuts now look less like a safety net and more like fuel for future inflation — and long-term bond yields ($TBT up 1.78% Friday) are where that unease is showing up.

Tariff Chaos, Fiscal Strain, and Global Spillovers

On Friday, the tariff saga escalated. Treasury Secretary Scott Bessent warned that striking down Trump’s global tariffs would cause a “dangerous diplomatic embarrassment,” undoing months of trade negotiations. He and other cabinet officials urged the appeals court to delay any ruling until the Supreme Court weighs in.

The timing is critical. Just days earlier, Bessent said tariff revenues could top $500B annually, possibly near $1T, making them the key offset to Trump’s tax cuts. The CBO estimated tariffs could shrink deficits by $4T over ten years, plugging the $3.4T hole created by the tax bill. If the courts invalidate the tariff regime, that revenue disappears — and the fiscal framework for Trump’s “tariffs + tax relief” strategy collapses.

The announcement landed just after futures closed Friday, leaving markets to stew over the weekend. The implications are twofold: deficits would widen further and Washington would lose the fiscal space to fund industrial policy or sustain tax relief. Layered on top is the risk of a government shutdown on September 30, as Trump’s use of a “pocket rescission” to cancel $5B in foreign aid has already triggered a new budget standoff with Congress.

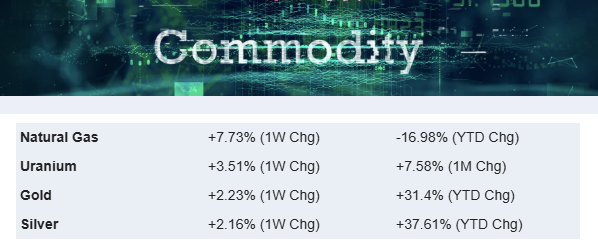

Safe Havens Surge: Gold and Silver Flash Green

By Friday, the market’s response was clear: investors rotated into hard assets. Gold ($GLD) and silver ($SLV) spiked sharply, marking their strongest weekly performance since June. The drivers are layered:

- Fed credibility crisis.

- Tariff reversal undermining fiscal anchors.

- Rising inflation expectations.

- AI volatility raising fears of an overextended trade.

Bitcoin, notably, traded lower against equities—suggesting crypto is not yet reclaiming its “digital gold” role. Instead, traditional metals are reasserting themselves as the hedge of choice.

Last Week's Stock Market Performance

Markets ended the week little changed after two sharp down days bookended a midweek rally. The S&P 500 (-0.1%) notched its 19th and 20th record closes before fading late, while the Dow (-0.2%) and Nasdaq (-0.2%) also slipped. Semiconductors dragged after Nvidia’s cautious revenue outlook.

Weekly Sector and Index Performance

- Indices: Dow –0.2%, S&P 500 –0.1%, Nasdaq –0.2%, Russell 2000 +0.1%, VIX +8% to 15.36

- Sectors: Energy (+2.5%) led; Consumer Staples (–1.7%) and Utilities (–2.1%) lagged

- Global: China (+0.8%) outperformed; Europe broadly weaker (France –3.3%, Germany –1.9%)

- FX & Crypto: EUR/USD –0.26%, Bitcoin –6%, Ethereum –8.9%

- Notables: Wynn Resorts (+11%), Deckers (+10%), Autodesk (+8%) topped gainers; Keurig Dr Pepper (–17%), Hormel (–13%), Moderna (–11%) led losers

Upcoming Events This Week

In a shortened week, the spotlight is on the August jobs report, the last labor release before the Fed’s September meeting. Consensus expects just 78k payrolls added, unemployment edging up to 4.3% (a near four-year high), and wage growth steady at 0.3%. The ADP report, JOLTS, and Challenger layoffs will offer additional context. Beyond labor, the ISM PMIs will update on manufacturing contraction and services expansion, while the trade balance will be watched for tariff effects. On earnings, Broadcom and Salesforce could sway sentiment around the tech sector.

Company News

LevelFields AI Stock Alerts Last Week

Trip.com (TCOM) +13.6% on $5B Buyback

Trip.com jumped 13.55% this week after its board authorized a new $5 billion share repurchase program covering both ordinary shares and ADSs. The move underscores confidence in the company’s long-term outlook and capital position, marking one of the largest buyback programs among Chinese travel platforms.

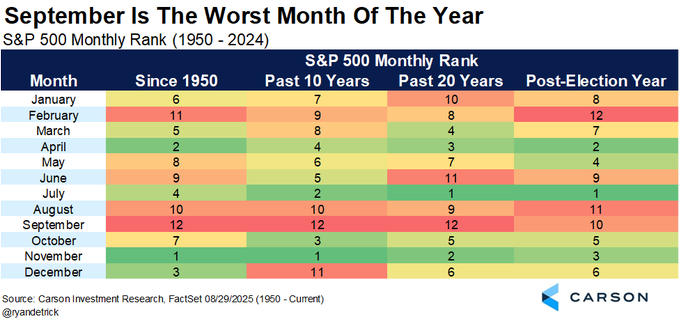

September Seasonality: Caution Ahead

September has long carried a reputation as the market’s weakest month. Since 1927, the S&P 500 has posted negative returns 56% of the time, with an average decline of –1.2%. Unlike October, which often sparks rebounds, September’s drag reflects a mix of structural headwinds: quarter-end tax payments and Treasury issuance draining liquidity, mutual fund and pension rebalancing, and a tendency for investors to reduce risk ahead of earnings season.

This year those seasonal pressures collide with unusually narrow market breadth and record hedge fund crowding in megacaps. Positioning is stretched, while short interest in volatility is near extremes—leaving the tape vulnerable to a sharp reversal if a catalyst emerges.

Historically, defensive groups like healthcare ($XLV), consumer staples ($XLP), and utilities ($XLU) have held up best in September, while small caps ($IWM) and select cyclicals ($XLI) sometimes outperform once the Fed signals easing. For tactical traders, volatility hedges ($VIX)—such as VIX call spreads or index put spreads—tend to offer cheap insurance when the VIX sits near cycle lows.

The takeaway: September is rarely a month to chase highs. A defensive tilt, paired with selective exposure to sectors that benefit from falling rates, has historically outperformed. October often resets the stage—but first comes a seasonal test of discipline.

Culture Wars Spill Into Markets: Cracker Barrel & American Eagle in Focus

Cracker Barrel (CBRL) became a political flashpoint this week, with shares jumping nearly 10% after President Trump weighed in Tuesday morning, urging the company to restore its classic “old timer” logo after replacing it to be more "inclusive." Management quickly complied, scrapping the modern redesign that had sparked backlash from conservatives. The reversal underscored how fast cultural controversies—and Trump’s direct involvement—can move consumer-facing stocks.

American Eagle (AEO) also saw a boost, with shares up as much as 6.1% midweek following its pivot from the Sydney Sweeney campaign backlash to a splashy new collaboration with NFL star Travis Kelce. The AE x Tru Kolors line dropped just after Kelce’s engagement to Taylor Swift, driving visibility and investor interest ahead of next week’s earnings.

The takeaway: political endorsements and cultural flashpoints are now market catalysts, sparking rallies in retail names long before fundamentals catch up.

.png)

Using AI to Spot Dividend Stocks

Top AI Healthcare Stocks to Watch in 2026

Scientists Find CBD Helps Alcoholics

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai