.png)

L1 Weekly Stock Market News Analysis

September 7th, 2025

TLDR:

Markets are heading into September with a volatile mix of weak data, dovish Fed bets, and rising geopolitical risks in the Americas:

- Rate cuts locked in. A soft jobs print pushed unemployment to its highest since 2021, cementing expectations for a September Fed cut — with markets now pricing in three cuts by year-end. Bonds rallied hard, sending yields down 10–15bps on the week, while gold surged to a record $3,600.

- Inflation still sticky. The next CPI report, due on Thursday, looms large. Consensus expects a 0.3% MoM core print — still well above target. If inflation holds hot, it could narrow the Fed’s ability to deliver the deep easing path investors are betting on.

- Tariff turbulence. Trump signaled new semiconductor tariffs “shortly,” though Apple and other firms pledging domestic buildouts may be spared. Meanwhile, the Appeals Court ruling against Trump’s broader tariff program undercuts a key fiscal revenue pillar, raising fresh deficit questions.

- Caribbean escalation. The U.S.–Venezuela standoff intensified after Washington struck a suspected drug boat and deployed F-35s to Puerto Rico. Caracas responded with jet flyovers and militia mobilizations. Beyond narcotics, the U.S. move reflects deeper aims: securing energy supply, countering China and Russia, and reasserting control in the region. Commodities and insurers are now pricing in Caribbean risk premiums.

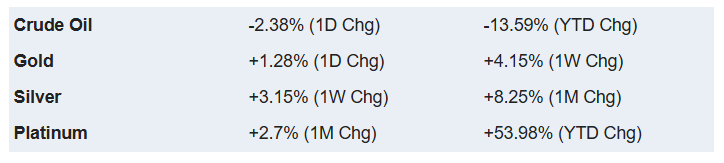

- Safe havens favored. Gold, silver, and Bitcoin all climbed as traders rotated out of stretched equities. Oil sank on OPEC+ production hikes and soft demand signals, leaving energy equities lagging even as defense names rallied on headlines.

September opens with markets betting on aggressive Fed easing, but inflation, tariff uncertainty, and a growing military flashpoint in Latin America mean volatility risks are rising. Investors are rotating toward metals, bonds, and defense as tech leadership begins to show cracks.

Thursday: Labor Market Cracks

The JOLTS report confirmed a turning point: for the first time since 2021, job openings fell below the number of unemployed, showing demand for workers is weakening. The ISM Services Index, which tracks business activity through company surveys, surprised on the upside at 52.0, while the S&P Global Services PMI, another widely watched gauge of service-sector health, slipped to 54.5. Meanwhile, factory orders fell –1.3% m/m. Together, these reports added to the slowdown we highlighted last week.

The Fed is still being pushed to cut into strength, a dynamic we noted previously. Q2 GDP was revised up to 3.3%, the fastest pace in nearly two years, driven by consumer spending and data-center investment. But the Fed has less room to maneuver: its cash buffers are nearly gone, the Treasury is flooding markets with new debt, and political battles over independence are heating up. Cuts here may steady markets in the short run, but risk fueling inflation again over time.

Friday: Job Growth Stalls, Markets Eye 50bps

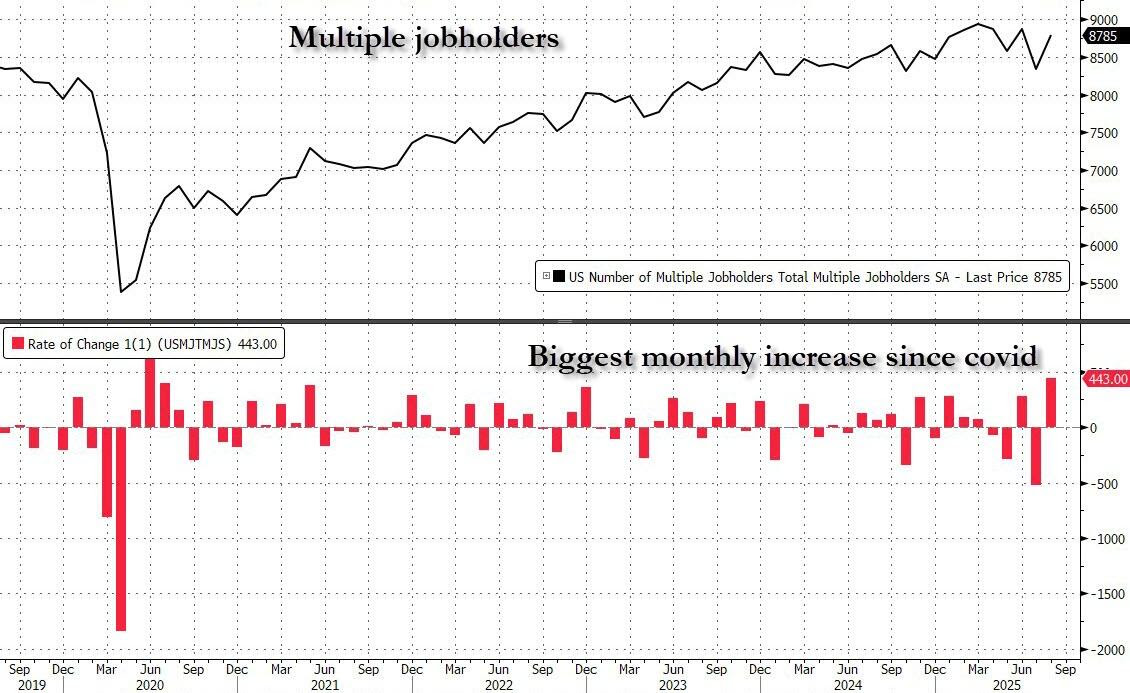

Nonfarm payrolls rose just 22,000 in August, the weakest since 2020. June was revised into negative territory, the unemployment rate climbed to 4.3%, and wage growth slowed to 3.7% y/y. Full-time jobs shrank again, replaced by part-time roles, while multiple jobholders jumped to the highest since COVID. Health care added jobs, but government, manufacturing, and energy all slipped. With revisions leaving almost no net job creation, markets locked in expectations for a September cut — and put 50 bps back on the table.

The debate now turns on size: a smaller cut signals caution, while a larger one would acknowledge how quickly the labor market is losing momentum. Either way, the weak breadth of job growth makes clear the slowdown is spreading across industries.

What It Means for Markets

- If the Fed cuts 50 bps: A surprise could spook markets the economy is eroding too fast and needs a rescue. Investors are taught to rotate into more safe assets like consumer staples, gold, and healthcare when this occurs.

- If the Fed cuts 25 bps: The more likely outcome — gradual easing while growth risks remain. Smallcap stocks and growth stocks tend to outperform, as do companies with lower valuations and strong balance sheets. Gold and silver likely extend their gains as a hedge against the dollar devaluing.

Consensus is that Powell will cut in September. The Fed enters September under pressure to act — and its credibility, not just its liquidity tools, is on the line.

Supreme Court Tariff Showdown

The tariff fight is entering a decisive phase. On Aug. 29, a federal appeals court ruled that President Trump went beyond his authority by using emergency powers (IEEPA) to impose broad tariffs on U.S. imports. The decision is on hold until Oct. 14, giving the administration time to appeal, but it now heads toward a likely showdown at the Supreme Court.

Even if those powers are curbed, tariffs won’t disappear. Congress has long delegated substantial authority to the executive branch. This delegation began in earnest with the Reciprocal Trade Agreements Act of 1934, passed under President Franklin D. Roosevelt, which allowed the White House to negotiate trade deals and adjust tariffs by up to 50% without returning to Capitol Hill for approval. F.D.R. used this authority to ink over 30 bilateral agreements, reshaping global trade amid the Great Depression. The Trade Expansion Act of 1962, under President John F. Kennedy, introduced Section 232, empowering the president to impose tariffs on imports that threaten national security following a Department of Commerce investigation. Similarly, the Trade Act of 1974’s Section 301 authorizes retaliatory measures, including tariffs, against unfair foreign trade practices. And the International Emergency Economic Powers Act of 1977 (I.E.E.P.A.) grants even broader leeway during declared national emergencies to regulate international economic transactions.

Trump’s first term built on this legacy, using Sections 232 and 301, along with I.E.E.P.A., to levy tariffs on steel (25%), aluminum (10%), and vast swaths of Chinese goods—actions that courts largely upheld as within statutory bounds. His successor, Joe Biden, not only retained these tariffs but escalated them in 2024 on Chinese electric vehicle batteries and solar cells, pushing rates over 100% in some cases under the same Section 301 authority.

Ronald Reagan, the conservative icon, invoked Section 301 in the 1980s to hit Japanese motorcycles with a 100% tariff (later scaled back) and semiconductors with similar measures to combat dumping and intellectual property theft. George W. Bush safeguarded the steel industry in 2002 with tariffs up to 30% under the Trade Act’s provisions. Even Barack Obama, hardly a protectionist, imposed up to 35% tariffs on Chinese tires in 2009 to shield domestic manufacturers from surges in imports. So while the basis for the latest tariffs from Trump may not hold up in court, there are myriad other legal bases from which to place them in effect.

Who Stands to Gain or Lose

Potential winners if IEEPA tariffs are curtailed:

- Big-box retailers (Walmart, Amazon): Lower import costs improve margins and pricing power.

- Consumers: Relief in tariff-heavy goods would soften prices in select categories.

- Exporters in ASEAN, Brazil, and India: With fewer blanket tariffs, trade flows could recover.

- Equity markets: A ruling that reins in executive power may be seen as a stabilizing outcome for investors.

Likely losers:

- U.S. bond market: Weaker tariff revenues expand deficits, adding pressure to already heavy Treasury issuance.

- Strategic sectors (chips, EVs, steel, pharmaceuticals): Narrower tariffs remain likely, keeping costs elevated.

- Shipping and logistics firms: More fragmented trade policy means shifting compliance burdens and higher unpredictability.

Geopolitical angle: China could gain indirectly. A weaker U.S. negotiating position and diverted supply chains through ASEAN provide Beijing with breathing room. Some analysts are already floating the idea of a limited trade arrangement — a “Phase 1.5” — to pause escalation in exchange for selective tariff relief.

Last Week's Stock Market Performance

- The S&P 500 and Nasdaq 100 were flat for the week. Communications stocks performed the best, due to Google winning its anti-trust case. Healthcare and consumer staple stocks outperformed other sectors which declined. Goldminers, homebuilders, and solar stocks - all interest rate sensitive - performed the best among the industries while oil drillers and semiconductor stocks sold off the most.

- Gold and Silver ETFs rose 5% last week while Bitcoin was flat and Ethereum fell slightly.

Upcoming Events This Week

Markets face a heavy data slate that could reset rate expectations. In the U.S., the focus is on CPI and PPI inflation prints, along with the annual payroll benchmark revisions after a string of weak jobs data. The University of Michigan sentiment survey will provide an early read on consumer confidence.

Abroad, the ECB is set to hold rates steady while publishing updated forecasts, and Europe’s largest economies — Germany, France, and the UK — release industrial production figures, with the UK also reporting monthly GDP. In Asia, investors will watch for policy signals from Beijing and fresh inflation readings out of China and India.

.png)

Company News

LevelFields AI Stock Alerts Last Week

Arrowhead Pharmaceuticals (ARWR) +20% on $2B Novartis Deal

Arrowhead surged 20% this week after striking a licensing agreement with Novartis worth up to $2 billion for its neuromuscular therapy program. The deal, which includes upfront payments and milestones, positions Arrowhead as a major player in next-generation RNAi therapeutics while giving Novartis expanded exposure to rare disease markets.

vTv Therapeutics (VTVT) +21% on FDA Breakthrough Designation

vTv jumped 21% in a single day after its diabetes drug candidate, Cadisegliatin, received Breakthrough Therapy designation from the FDA. The designation accelerates development and review timelines, underscoring the therapy’s potential to address unmet needs in diabetes treatment. The sharp move reflects investor enthusiasm for regulatory catalysts in small-cap biotech.

Broadcom (AVGO) +9.4% on $10B+ OpenAI Chip Deal & Strong Earnings

Broadcom shares rallied 9.4% to $334.89 after reporting a $10B+ order from OpenAI for custom AI accelerator chips, set to ship in 2026. The deal positions Broadcom as a strategic alternative to Nvidia in AI hardware, with OpenAI aiming to ease supply bottlenecks and tailor processors for its expanding model needs.

For the quarter, revenue rose 22% YoY to nearly $16B, beating expectations ($15.8B), with EPS of $1.69 topping estimates. AI semiconductor sales hit $5.2B and are projected to climb to $6.2B in Q4. Broadcom also guided Q4 revenue to ~$17.4B, above consensus, while CEO Hock Tan extended his leadership through at least 2030.

Culture Meets Earnings: American Eagle (AEO) +26% on Guidance Boost

Last week we noted how cultural flashpoints — from the Sydney Sweeney denim ad to the Travis Kelce collaboration — had already lifted American Eagle shares. This week, earnings confirmed the impact: AEO soared 26% after reinstating full-year guidance well above expectations. Management now projects operating income of $255M–$265M (vs. $176M consensus) with same-store sales set to turn positive in the second half.

Q2 results were mixed — revenue slipped 1% YoY to $1.28B and same-store sales fell 1% — but EPS of $0.45 more than doubled forecasts. The company credited early traction from the Sweeney and Kelce campaigns for boosting engagement and sales momentum heading into fall.

The takeaway: cultural buzz has converted into real financial upside. With campaigns driving customer awareness and management guiding to stronger back-half performance, AEO has shifted from a retail controversy story into one of the quarter’s biggest retail rebound trades.

.png)

Using AI to Spot Dividend Stocks

Top Defense Stocks to Watch in 2026

Scientists Find CBD Helps Alcoholics

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai