.png)

L2 Weekly Stock Market News Analysis

October 5th, 2025

TLDR:

- The government shutdown continued into the weekend, halting key economic reports and raising fears that the blackout could delay the Fed’s long-anticipated rate cuts. With no jobs or inflation data to guide decisions, investors worry the central bank may hold off on easing—risking a pullback if confidence fades.

- Private indicators offered little reassurance. The ADP jobs report showed slowing hiring, and the ISM services index hovered near stagnation—both hinting that the economy is losing steam. But without official confirmation from government data, markets remain in limbo.

- Overseas, the U.S. unveiled a 20-point Gaza ceasefire plan that drew rare global support, with leaders from Israel, Arab nations, and the EU praising the framework. Hamas agreed in principle to release hostages under U.S.-brokered terms, while Israel began initial troop withdrawals from Gaza City—the most significant progress toward peace in over two years.

- Gold neared record highs at $3,875 an ounce, extending a seven-week rally as investors sought safety amid fiscal uncertainty and geopolitical risks. The metal has now gained nearly 50% year-to-date—on pace for its strongest performance since 1979.

Government Shutdown Begins: Markets Lose Their Compass

The government shutdown that began this week has sent markets lower — not just because of federal furloughs, but because it’s cut off the nation’s economic data pipeline at a critical moment. On Friday, stocks fell sharply after the White House confirmed that the Bureau of Labor Statistics (BLS) and the Bureau of Economic Analysis (BEA) would suspend all major economic releases, including the September jobs report, inflation data, and GDP updates.

This announcement landed just as new data showed that America’s job market is already in trouble. Hiring has slowed across nearly every major sector — from professional services and manufacturing to retail and construction. More than a quarter of job seekers have been unemployed for over six months, and underemployment (people stuck in part-time or low-paying roles) has climbed to its highest level in nearly four years.

Fed Chair Jerome Powell has called this a “low-hire, low-fire” labor market — one where companies are holding onto workers but not adding new ones. He’s warned that if layoffs begin to rise, unemployment could “very quickly” climb further. That’s why the Fed’s focus has shifted toward supporting jobs and easing conditions later this year.

But now, with the shutdown halting BLS and BEA operations, the Fed has no data to confirm what’s happening in real time. With no jobs report, no inflation print, and no spending data, policymakers are effectively flying blind heading into their October 28–29 meeting.

This comes at the worst possible moment. Markets had already priced in multiple rate cuts for late 2025 based on signs of a weakening job market. Without fresh data, the Fed is likely to pause those plans, leaving rates higher for longer — a shift that could trigger a short-term selloff as investors unwind their bets on easy policy.

When the Fed’s blind, investors fall back on instinct:

- Gold and silver rallied as traders moved into safe havens.

- Biotech, real estate, and small-cap growth stocks — all dependent on lower borrowing costs — tumbled.

- Utilities and consumer staples held up better, offering predictable cash flow and steady demand.

If the shutdown extends into mid or late October, inflation reports like CPI and PCE will also be delayed, leaving the Fed with little visibility until November. That means rate cuts could slip into 2026, keeping borrowing costs high for businesses, homeowners, and consumers.

Why Credit Downgrades Matter More Than Shutdowns

Most government shutdowns don’t cause lasting damage. The stock market often holds steady or even rises, and the economy usually recovers once the government reopens. That’s because the U.S. keeps paying its debts, and most federal spending resumes quickly afterward.

The bigger risk is a credit-rating downgrade — which becomes more likely when shutdowns drag on and political divisions deepen. Repeated standoffs over budgets and the debt limit signal to investors and rating agencies that Washington is struggling to manage its finances responsibly.

That perception matters. If confidence erodes, the U.S. could face another downgrade like those seen in 2011 (S&P), 2023 (Fitch), and 2025 (Moody’s)—each of which caused spikes in borrowing costs and shaken markets:

- 2011 – S&P downgrade: Stocks plunged over 6% in one day as investors demanded higher yields on U.S. debt.

- 2023 – Fitch downgrade: Treasury yields climbed as investors priced in greater fiscal risk, raising costs for mortgages and business loans.

- 2025 – Moody’s downgrade: Cited rising debt and interest burdens, pushing long-term yields higher and hurting sectors dependent on cheap financing like real estate and tech.

Today’s conditions make another downgrade possible. The federal deficit remains near 6% of GDP, and debt is projected to reach around 127% of GDP within five years. Combined with ongoing political gridlock and tensions between the White House and the Federal Reserve, these factors threaten the stability that underpins America’s top-tier credit rating.

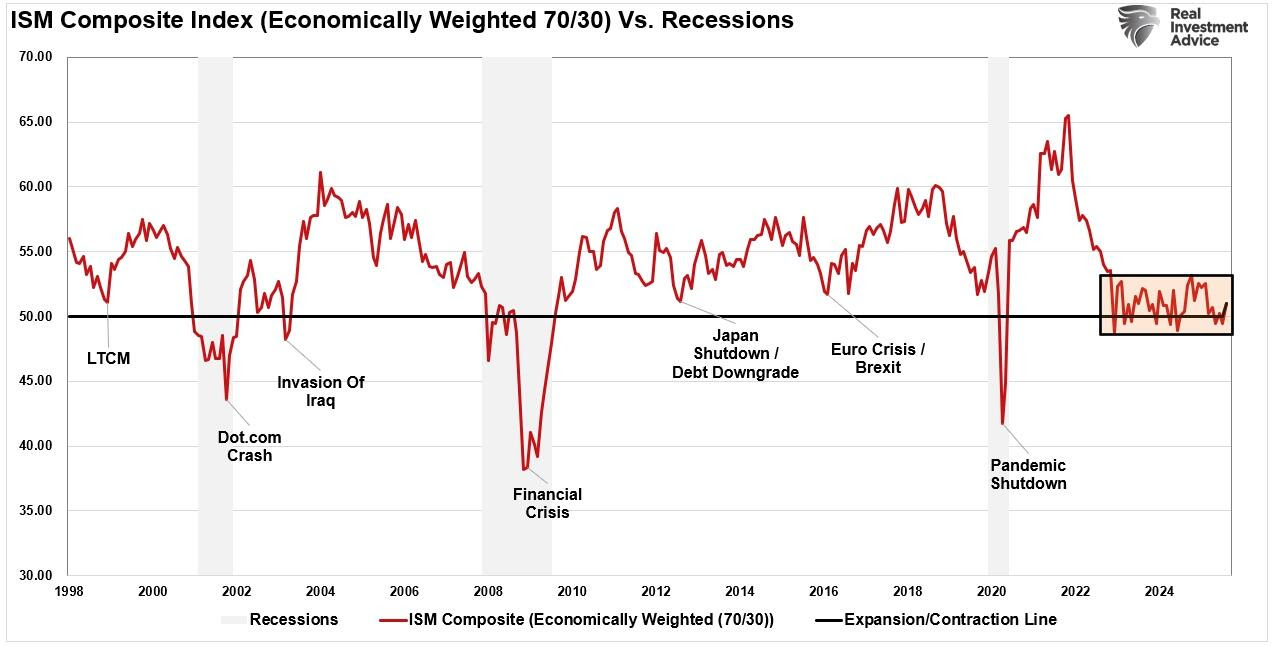

****The ISM index shows how U.S. business activity rises above 50 in growth and falls below 50 in recessions. It’s been stuck near 50 since 2022 — signaling a weak, stagnant economy that’s barely avoiding contraction.****

The Recession That Never Came — Or Just Hasn’t Shown Up Yet

For nearly three years, experts have warned that a recession was right around the corner. The signs all pointed that way — rapid rate hikes, an inverted yield curve (when short-term interest rates rise above long-term ones, a classic signal that investors expect slower growth ahead), weak manufacturing, and high inflation. Normally, that mix ends in a downturn.

Yet here we are, late 2025, with the economy still growing and unemployment still low. The question isn’t whether those warnings were wrong — it’s why the crash hasn’t come yet and what happens when the temporary supports fade.

Why the U.S. Has Stayed Afloat

The U.S. has avoided recession so far because it’s been running on policy spending and AI investment, not broad-based strength.

- Government support — Massive federal spending and subsidies kept demand steady even as borrowing costs rose.

- AI boom — A large share of GDP growth has come from companies building data centers, servers, and power systems to run artificial intelligence. This wave of construction and tech investment has masked weakness elsewhere in the economy.

- Consumer credit — Households kept spending by dipping into savings and taking on more debt, even as wage growth slowed.

Why the Next Phase Could Be Tougher

If a recession hasn’t hit yet, it might just be delayed rather than avoided. The economy could shift from fast growth to slow, uneven stagnation — still growing, but not enough to feel it.

The problem: when the next slowdown comes, AI could speed up job losses.

- Companies already use AI to automate administrative, customer service, and data tasks — through platforms like ServiceNow (NOW), UiPath (PATH), Automatic Data Processing (ADP), and Palantir (PLTR).

- If business slows, firms are more likely to replace workers with software than rehire them later.

- That means the next recession could bring a new wave of job displacement that hits faster and cuts deeper than before.

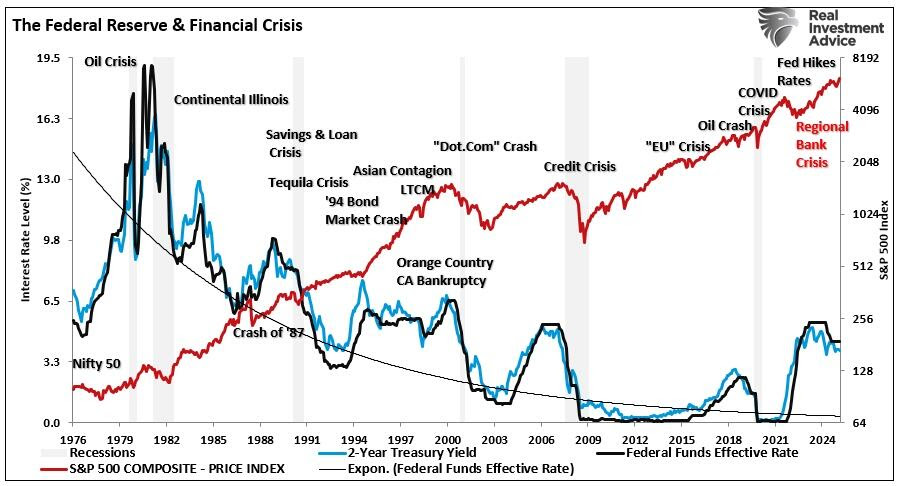

**** This chart above — The Federal Reserve & Financial Crisis — visualizes nearly 50 years of monetary tightening and the market shocks that followed. It highlights a consistent pattern: every major Fed rate-hike cycle eventually triggers a financial or economic crisis.****

How to Think About It as an Investor

This isn’t a “panic” moment — it’s a time to be smart and selective.

- Gold and silver — Safe havens when the dollar weakens or inflation returns.

- Utilities and healthcare — Steady businesses with reliable demand.

- AI infrastructure — Focus on the “builders,” not just the headline tech names:

- Cooling and power: Vertiv (VRT), Eaton (ETN)

- Grid upgrades: Quanta (PWR), GE Vernova (GEV)

- Nuclear power: BWX Technologies (BWXT), Centrus (LEU), Constellation Energy (CEG)

Last Week's Stock Market Performance

The Health Care sector emerged as the standout performer with a robust gain of 6.88%, showing a steady upward trajectory throughout the period. Utilities (XLU) followed with a solid increase of 2.42%, while Industrials (XLI) and Materials (XLB) posted modest advances of 1.20% and 1.15%, respectively. Real Estate (XLRE) and Consumer Staples (XLP) experienced slight upticks of 0.48% and 0.09%. In contrast, several sectors faced declines: Financials (XLF) slipped by 0.26%, Consumer Discretionary (XLY) by 0.77%, Communication Services (XLC) by 1.51%, Technology (XLK) by 2.00%, and Energy (XLE) suffered the steepest drop at 3.35%.

Among industries, clean tech, biotech, materials, and solar stocks rallied while oil drillers and regional banks sold off, alongside homebuilders.

Upcoming Events This Week

Markets this week are focused on the government shutdown, which is holding up key reports that investors use to gauge the economy’s health. Without data like trade numbers or jobless claims, it’s harder to see where growth or inflation are heading. The Fed’s meeting minutes will still be released and could hint at future rate cuts. Consumer confidence data from Michigan will also show how people are feeling about jobs and prices. Overseas, central banks in Europe and New Zealand are updating their policy outlooks, and fresh data from Europe and emerging markets will help gauge how global demand is holding up—all important for U.S. companies that depend on exports and global growth.

.png)

Company News

LevelFields AI Stock Alerts Last Week

Taysha Gene Therapies (TSHA) +53% on FDA Breakthrough News

Taysha Gene Therapies surged 53% in a single day after announcing that the FDA granted Breakthrough Therapy Designation for its experimental treatment TSHA-102 in Rett Syndrome, a rare neurological disorder. The designation speeds up development and review, signaling strong confidence in the therapy’s potential. Investors saw it as a major validation of Taysha’s platform and pipeline, sending shares sharply higher.

FICO (FICO) +21% on Credit Score Shakeup

Fair Isaac Corp. surged more than 21% last week after announcing it will begin selling FICO credit scores directly to mortgage resellers, cutting out middlemen like Equifax (EFX) and TransUnion (TRU).

The move allows mortgage lenders and brokers to calculate and distribute scores themselves—reducing costs and adding price transparency to the mortgage process. Investors saw it as a major power shift in consumer credit data, sending FICO shares up 18% in a day while Equifax and TransUnion each fell over 8%.

Analysts called the change a “big win” for FICO, which gains new recurring revenue and tighter control over score distribution. It also comes as Fannie Mae and Freddie Mac move toward accepting more credit models like VantageScore, setting up a new competitive era in how creditworthiness is measured.

Lithium Americas (LAC) — U.S. Takes Equity Stake in Thacker Pass Mine

The U.S. government has taken an equity stake in Lithium Americas (LAC) as part of a $2.26 billion Department of Energy loan supporting construction of the Thacker Pass lithium mine in Nevada — the largest planned lithium project in the Western Hemisphere.

The project’s Phase 1 output of 40,000 metric tons per year will supply enough lithium for roughly 800,000 EVs. GM holds a 38% stake with exclusive rights to Phase 1 production, while Washington’s new position gives it direct exposure to future revenue.

The move marks a major step in the U.S. push to onshore critical mineral supply chains and reduce reliance on China, following July’s Pentagon investment in MP Materials. By taking equity rather than issuing only loans, the government is signaling it wants a lasting role in the nation’s clean-energy resource base.

.png)

The Greatest Trades of All Time!

How Warren Buffet Used Events to Make Fortunes

How Are Robots Being Used Today for Business?

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai