.png)

Macrosynthesis

TLDR: Big Tech Rallies Midweek, But July Closes With Jobs Miss, Tariffs, and Market Turbulence

The final week of July played out in two acts. Midweek, Meta and Microsoft delivered blockbuster earnings—Meta soared 11%, Microsoft gained 4%—after beating expectations and reaffirming aggressive AI spending. Their results lifted tech and chip stocks, fueling a brief wave of optimism across the market.

The Federal Reserve kept interest rates unchanged for the fifth straight meeting, pointing to slowing growth and elevated uncertainty. Chair Jerome Powell projected cautious confidence in the economy’s resilience, downplaying tariff effects and suggesting the labor market remained solid.

But by Friday, that confidence looked misplaced. The July jobs report showed just 73,000 new positions added—well below expectations—with steep downward revisions to prior months. Treasury yields fell, and the odds of a September rate cut jumped above 80%. The same day, the White House announced sweeping new tariffs of up to 41% on imports from Canada, India, and Taiwan, reviving trade risk at a precarious moment.

The pharmaceutical sector also came under fire after President Trump demanded 17 major drugmakers—including Eli Lilly, Pfizer, and Novo Nordisk—cut U.S. prices to match those overseas. While Eli Lilly held steady, broader pharma stocks declined amid fears of heightened policy pressure.

What began as a strong week for tech ended with a jolt across jobs, trade, and regulatory fronts—casting doubt on the stability Powell suggested and setting a more volatile tone heading into August.

Frozen Federal Interest Rates, Fragile Confidence

The Federal Reserve held interest rates steady at 4.25%–4.5% for a fifth straight meeting, but this time, the decision revealed a divided front and growing uncertainty. Two voting members—Governors Waller and Bowman—broke ranks and called for an immediate cut, marking the first dual-governor dissent since 1993. It was a subtle but historic sign of rising internal disagreement about how much longer the Fed can afford to hold the line.

The official statement reflected that tension. The Fed dropped language describing the economy as growing at a “solid pace,” instead noting that growth had “moderated” in the first half of the year. The word “diminished” was also stripped from its assessment of uncertainty, leaving only that “elevated” risks remain. These redline edits signaled a shift—not toward panic, but away from the quiet confidence of earlier meetings.

Chair Jerome Powell struck a cautious tone in his press conference, insisting the Fed remained data-dependent and would not overreact to tariff risks. But the market heard a dovish drift. Traders raised the odds of a September cut to over 80% as yields dropped and expectations adjusted. The disconnect was clear: while Powell emphasized stability, both the bond market and parts of the Fed itself are increasingly betting on a pivot.

Meanwhile, the broader economic picture isn’t offering much clarity. Growth metrics have firmed, but inflation has softened significantly—leaving the Fed caught between outdated fears of overheating and a new reality of political instability, fragile consumer confidence, and fiscal strain.

This week’s Fed decision may not have moved rates, but it moved the debate. And just two days later, the labor market data would move it further.

Jobs Report Crumbles as Native Shift Reshapes Labor Market

Friday’s July jobs report wasn’t just weak—it marked a structural break. Payrolls rose by only 73,000, far below expectations and revised May and June figures wiped out 258,000 prior jobs. The three-month average now sits at just +35,000—the lowest streak since COVID—and nowhere near the 100–150K monthly gains historically needed to keep unemployment flat.

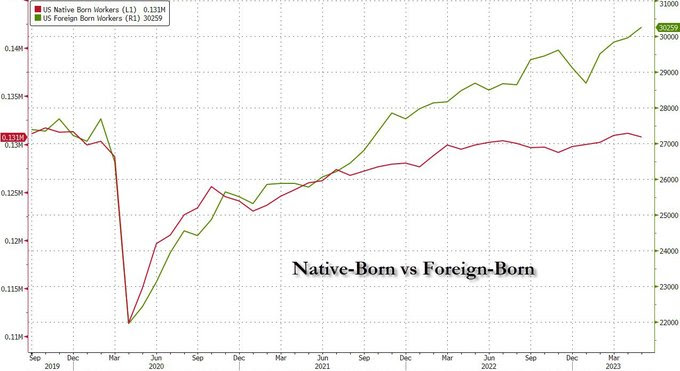

The details were worse under the hood. Full-time jobs fell by 440,000, part-time jobs surged by 237,000, and the household survey showed a 260,000 employment loss. Labor force participation declined to 62.2%, and minority unemployment rates rose to the highest since 2021. Despite these signs of softening demand, wages rose 3.9% YoY, lifted in part by the replacement of low-wage workers with higher-paid domestic hires.

What’s behind the shift? Data now shows that foreign-born employment declined for the fourth month in a row—down 467,000 in July alone—while native-born employment rose by 383,000. Since Trump took office, foreign-born employment has declined in five of the past six months, while native-born workers have gained ground nearly every month. This appears to be the result of a targeted policy shift: a quiet but sweeping removal of undocumented workers from payrolls.

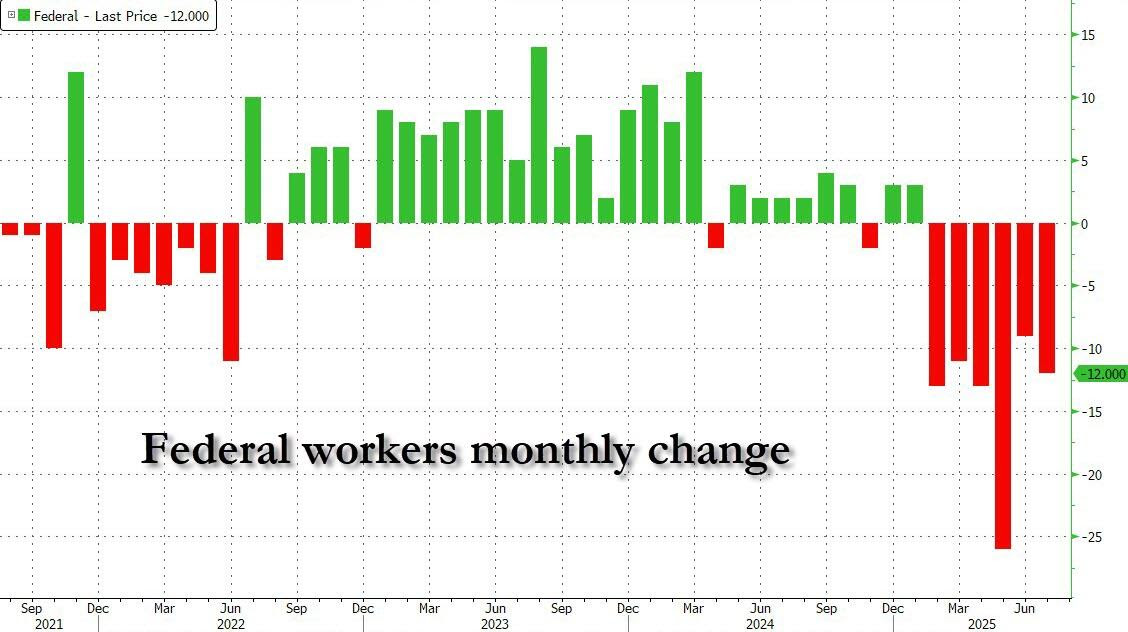

The result is a shrinking labor supply—especially in lower-wage sectors—paired with upward pressure on wages. Fewer workers, higher average pay, and more jobs concentrated in sectors like healthcare and social assistance. Federal government employment, meanwhile, declined for a sixth straight month, continuing its post-inauguration downsizing trend.

Markets quickly priced in a Fed response. Treasury yields fell 10–12bps, and odds for a September rate cut surged. Analysts flagged the steep revisions as the key catalyst, noting that Powell’s midweek confidence in the labor market now appears badly outdated. Trump didn’t wait to weigh in—he fired the BLS Commissioner within hours of the report and blamed the numbers on internal sabotage designed to weaken his position ahead of the election.

Utilities outperformed sharply on the news, as falling yields boosted the relative appeal of their high dividend payouts and defensive cash flows. With investors rotating into rate-sensitive sectors, the group benefited from both falling borrowing costs and rising demand for stability. Gold also jumped, gaining on the drop in real yields and renewed expectations for monetary easing. The precious metal continues to serve as a hedge against policy volatility and economic uncertainty, especially with political risk heating up into the fall.

The labor market is changing—and quickly. The purge of undocumented workers is reducing labor supply and lifting wage averages - a key promise by the Trump administration. But it's also creating frictions across sectors reliant on low-cost labor. What’s emerging is a labor market tighter, pricier, and more domestically sourced—and one that could force the Fed’s hand sooner than expected to try and boost jobs growth.

Labor Demand Is Vanishing—AI and Deglobalization Are Accelerating the Shift

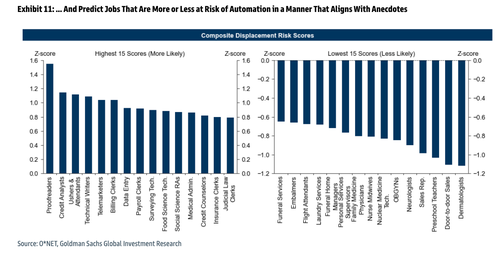

This week’s jobs report wasn’t just weak—it may be the early signal of something deeper: a turning point in labor demand. As full-time employment contracts and firms pull back hiring, we may be watching the front edge of AI-driven displacement arrive in real time. Goldman Sachs now estimates that hundreds of job categories, from credit analysts to customer service reps, are at heightened risk of automation as generative AI becomes cheaper, faster, and more capable.

Traditionally, global firms outsourced labor to cheaper markets to cut costs. But that model is breaking down. With rising tariffs and geopolitical fragmentation, the incentive to offshore is weakening—making domestic automation even more attractive. AI becomes the new cheap labor. Unlike human workers, it doesn’t require visas, wage negotiations, sick days or health insurance—and it doesn’t strike (yet).

While AI is often celebrated for its productivity gains and deflationary pull, the mechanism is sobering: fewer people earning wages means less aggregate demand. Fewer buyers equals less pricing power—goods get cheaper not because supply improves, but because demand erodes. This is how deflationary stabilization through automation can mask economic fragility.

The IMF estimates that 60% of jobs in advanced economies are exposed to AI. In the U.S., that exposure now coincides with a sharp native-born hiring spike, a plunge in foreign-born employment, and broad employer reluctance to invest in headcount. The result? A labor market that looks tight only on the surface, while silently absorbing a profound shift in who—and what—does the work.

And that backdrop leads straight into tariffs—because as the U.S. and its trading partners escalate protectionist moves, AI becomes not just a labor solution, but a strategic imperative. The only way to offset higher prices caused by tariffs, is to cut costs internally. There are two ways to do that: fire people and increase productivity through AI.

Tariffs Take Center Stage in a New Era of Strategic Trade

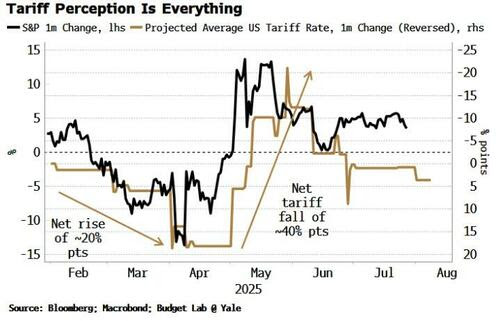

The world isn’t re-globalizing—it’s re-aligning. As artificial intelligence accelerates corporate automation, governments are reshaping the rules of trade to reflect geopolitical loyalties, not economic efficiency. Tariffs, once seen as market-disrupting shocks, are now embedded features of the global economy—and markets have stopped flinching.

Despite a steady rise in effective tariff rates this year, the S&P 500 has barely blinked. At the start of 2025, stocks reacted sharply to projected tariff hikes. But by July, that relationship collapsed. When tariff projections fell 40 points in May and June, equities rallied—even though the actual tariff load remained high. The takeaway? Investors now care more about avoiding worst-case scenarios than about the cumulative cost. Short-term relief, not structural impact, is what moves markets.

That dynamic was on full display with President Trump’s late-July trade deal with the EU. Days before a planned 30–50% tariff wall was set to trigger, the two sides agreed to a 15% baseline on most goods. Steel and aluminum tariffs remain at 50%, but Europe pledged over $750B in U.S. energy purchases (including nuclear reactors/ OKLO jumped on the news) and a wide-ranging commitment to American military equipment—turning trade into a security alliance. Whether those numbers are real or symbolic doesn’t seem to matter to markets right now.

Meanwhile, the U.S. and China extended their tariff freeze for another 90 days. The Stockholm meetings may yield little substance, but the extension itself delays escalation. For investors, another short-term win.

The picture is less stable elsewhere. India and Russia remain outside Trump’s new trade framework and now face 25% tariffs starting August 1. On Truth Social, Trump called India a “dead economy” and accused officials of rigging jobs data to hurt his campaign. Delhi responded with defiance and no sign of compromise. Analysts warn of a $10 billion export hit and rising strain on U.S.–India ties, once seen as a counterweight to China.

U.S. firms with major India exposure—Apple, GE, Dell, Cisco, and Boeing—now face potential disruption. Apple produces over 7% of iPhones in India, while Boeing relies on Indian-made components. Tech leaders like Microsoft, Amazon, and Google operate large R&D and support hubs in the country.

In parallel, Trump has threatened a 10% surcharge on BRICS nations pursuing de-dollarization, signaling a broader trade fragmentation. With each new deal or penalty, the message becomes clearer: access to the U.S. market now depends on strategic alignment—military, monetary, and energy-based.

Last Week's Market Performance

Wall Street posted its worst week since May, with the S&P 500 falling -2.4% to 6,238, the Dow down -2.9% to 43,589, and the Nasdaq slipping -2.2% to 20,650. Weaker-than-expected July jobs data, sticky inflation, and Trump’s renewed attacks on the Bureau of Labor Statistics fueled volatility. Core PCE rose 2.8% YoY, prompting the Fed to hold rates and signal patience. September rate cut odds surged back above 80% after Friday’s weak payrolls report.

Macro & Trade: Trump reimposed tariffs on several trade partners, reigniting trade war fears. His claims that the jobs data was “rigged” to hurt Republicans added political instability to an already fragile macro backdrop.

Sectors: Utilities (+1.5%) were the lone gainer. Materials (-5.4%), Consumer Discretionary (-4.5%), and Healthcare (-3.9%) led declines. Financials (-3.8%) and Industrials (-3.4%) also sold off.

Commodities: WTI crude rallied +3.3% to $67.33/bbl. Gold edged up +0.6% to $3,413.8/oz. Natural gas slipped -0.9% to $3.08.

FX & Crypto: The USD strengthened vs EUR (-1.33%) and GBP (-1.18%). Crypto struggled: Bitcoin -3.4%, Ethereum -5.7%, XRP -5.8%.

Top Gainers: Generac (+23%), Teradyne (+16%), eBay (+13%), Corning (+12%), Western Digital (+11%)

Laggards: Align Tech (-34%), Eastman Chem (-25%), Baxter (-25%), Coinbase (-20%), Moderna (-19%)

Global Indices: France -3.7%, Hong Kong -3.5%, Germany -3.3%. Japan -1.6%, China -0.9%, India -1.1%, UK -0.6%

Volatility: The VIX surged +36.5% to 20.38 as markets reeled from macro shocks and Trump-fueled uncertainty.

Upcoming Events This Week

Markets remain focused on Trump’s August 1 tariffs and Fed rate expectations following the weak jobs report. Major earnings are due from Disney, Palantir, AMD, McDonald’s, and Eli Lilly. Key U.S. data include ISM Services PMI, trade balance, factory orders, and Q2 productivity. Globally, central bank decisions (UK, India, Mexico) and inflation, trade, and GDP data from China, the Eurozone, Canada, and Southeast Asia will shape sentiment.

.png)

Company News

LevelFields AI Stock Alerts Last Week

Arena Group (AREN) +8.2% on Buyback Announcement

Shares of media company Arena Group jumped over 8% after its board approved a 3 million-share repurchase program. CEO Paul Edmondson cited undervaluation relative to peers and emphasized confidence in the company’s improving operational performance. Management highlighted a P/E below 11x versus 30x+ for the Russell 2000, suggesting room for rerating.

Silicon Motion (SIMO) +8.2% on Strong Q2 and Buyback

Silicon Motion rose 8.2% after reporting a 19% sequential revenue increase and announcing a buyback. Growth in SSD controller and smartphone-related chip sales drove the upside, with CEO Wallace Kou pointing to rising demand for AI-at-the-edge and diversified end markets. Non-GAAP EPS climbed to $0.69, beating estimates.

Consumer Stocks Fade Despite Earnings Beats

Roughly two-thirds of S&P 500 companies have reported Q2 earnings—with 83% beating profit estimates and earnings surprising by 8.3%. But despite those strong numbers, a surprising trend is unfolding: consumer-facing stocks are selling off even after positive results. Goldman Sachs analyst Scott Feiler highlighted the pattern Friday, noting that even quality names are fading post-earnings, with many continuing to decline in the days following.

Examples span both discretionary and staples: Philip Morris, Hershey, and Starbucks all fell after their results, while surprise beats from names like Deckers, PepsiCo, and Tractor Supply failed to hold their initial gains. In several cases, stocks opened sharply higher on earnings but ended the day flat or negative, often continuing to sell off for multiple sessions.

Feiler attributes the pattern partly to profit-taking in a cautious market, but it also reflects investor skepticism about consumer resilience and spending durability—even with signs of improved July trends and optimism tied to recent tax cuts. Only a few stocks—like Wingstop, Hilton, and housing-related names such as Builders FirstSource—have held their gains.

The broader takeaway: strong earnings alone aren’t enough to drive sustained upside in consumer stocks right now. Markets appear more focused on margin risks, soft guidance, and macro headwinds than headline beats.

Big Tech Earnings Split as AI Bets Diverge

Q2 results from Microsoft, Amazon, and Meta drew a sharp line between AI ambition and AI execution—and markets responded accordingly. Microsoft surged 8.2% after Azure revenue accelerated to +39% YoY, beating expectations and reasserting its AI dominance. The company’s $30B+ quarterly CapEx is backing tangible cloud growth, helping lift its market cap past $4 trillion.

Amazon, by contrast, delivered a strong quarter on paper—13% revenue growth and $30.9B in AWS sales—but soft Q3 guidance and slower AWS growth spooked investors. Despite a record $31.4B in CapEx (up 90% YoY), the stock fell 6.9%, as Wall Street questioned the near-term payoff of its AI spending spree.

Meta stole the spotlight. Shares jumped 13% after it beat across the board and raised guidance, attributing gains to AI-powered ad tools already lifting pricing and efficiency. While Reality Labs posted another $4.5B loss, the market focused on Meta’s ability to fund AI expansion through its dominant ad business—highlighting a rare blend of vision and profitability.

The message was clear: investors are done rewarding AI hype without follow-through. Microsoft and Meta are monetizing; Amazon is still proving it. In this phase of the AI race, capital alone isn’t enough—markets want margin traction, execution, and results now.

.png)

Flying Taxis in Dubai

This Stock is Up 1500%. You've Likely Never Heard of It.

Tesla's True Value Is From This Technology Fueling Everything

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai