.png)

TLDR:

- Markets closed at new record highs amid mixed macro and political shocks.

Producer inflation hotter than expected, likely ruling out a 0.5% September rate cut but keeping a 0.25% cut priced in. - Treasury yields climbed, gold posted its worst week since June, and oil fell to three-month lows.

- Record August options expiration drove volatility in momentum stocks, boosting meme stocks while traditional "momo" funds suffered their worst week since March.

- Trump's Alaska summit with Putin hinted at a Ukraine peace deal.

- Markets viewed this as short-term negative for defense and energy stocks (European defense already weakening), but risk-on for broader equities with small caps surging.

- Nasdaq now at 145% of M2 money supply—exceeding dot-com peaks—reviving tech bubble debates as AI megacap capex dominates the market.

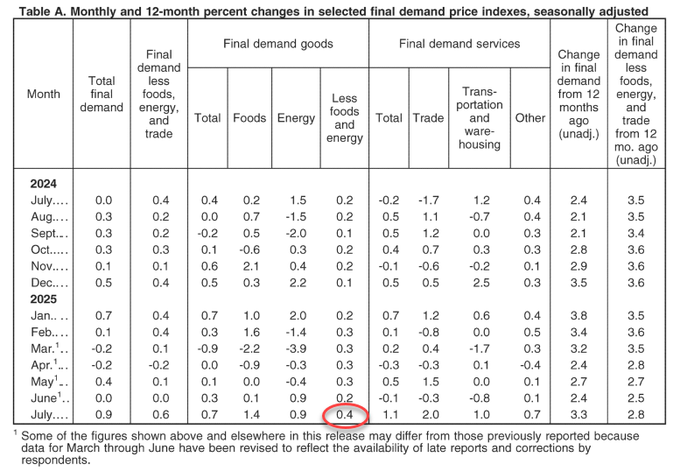

CPI, PPI and the Inflation Storm

July’s inflation data told a split story. Headline Consumer Price Index (CPI) looked benign, but core CPI rose 0.32% MoM and 3.1% YoY, its second-largest monthly gain of the year. That left the three-month annualized pace at 2.8%—well above the Fed’s 2% target and heading in the wrong direction. The real shock came with producer prices: PPI jumped 0.9% MoM, the steepest in over three years, with services up 1.1% and core PPI at 3.7% YoY. Portfolio management costs surged nearly 6%, while trade margins spiked 2%, signaling tariffs and input costs are filtering through although mainly on financial services not goods.

The effect was immediate: odds of a 50bps September cut fell, long-end Treasury yields rose, and gold logged its worst week since June. Equities largely shrugged it off, but inflation risk is re-pricing the curve.

Winter Almanac: Cold, Snow, and Energy Stress

The Farmer’s Almanac is projecting a harsh 2025–26 winter, with deep freezes from the Northern Plains to New England and repeated snowstorms across the Great Lakes and Northeast. Even with a spotty track record, the forecast collides with already fragile grids in the Mid-Atlantic, raising the risk of blackouts, price spikes, and political blowback. For markets, a colder winter favors going long on natural gas (UNG, LNG exporters) and heating oil plays, while utilities (XLU, Constellation, PPL) could see both upside in pricing and volatility risk. Severe snow years also boost demand for equipment and retailers (DE, CAT, GNRC, WMT, COST), while insurers face higher catastrophe losses.

Fiscal Expansion and the Next Wave

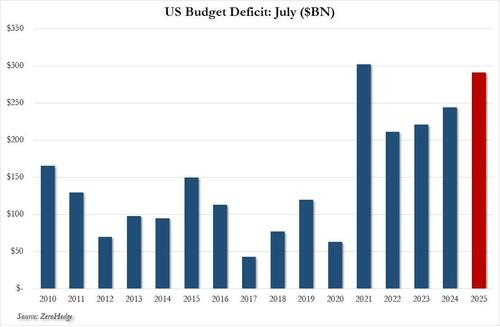

Tariffs are now bringing in nearly $20B per month—about $240B annually—but spending is rising far faster. July U.S. federal government spending jumped to $630B, up almost 10% YoY, while revenues gained just 2.5%. The result was a $291B deficit, the second-worst July on record and a reversal from June’s brief surplus. Year-to-date, the deficit has already hit $1.63T, putting 2025 on pace to be the third-worst fiscal year in U.S. history.

The burden of debt service is accelerating even faster: the U.S. paid $92B in July interest alone, pushing the year-to-date total over $1T—already larger than defense spending. With debt costs set to exceed $1.2T this year, fiscal pressures are reinforcing inflation just as PPI, core CPI, and electricity costs reheat.

Trump–Putin Alaska Summit: Peace or Stalemate?

President Trump’s high-stakes meeting with Vladimir Putin in Alaska aimed to hammer out a framework to end the Russia–Ukraine war. Trump hailed it as “very successful,” stressing that only a full peace agreement—not a temporary ceasefire—would suffice. European leaders cautiously welcomed the effort but insisted Ukraine’s sovereignty and security guarantees remain non-negotiable.

Putin, for his part, praised Trump’s approach and argued the conflict would never have erupted under his leadership, while reiterating Moscow’s demands for territorial concessions and NATO exclusion. Zelenskyy, set to visit Washington next week, has rejected ceding land and warned that Ukraine won’t accept any settlement imposed without its consent.

Market lens: Analysts see limited odds of a breakthrough. A stalled outcome likely keeps the status quo, while even a partial ceasefire could weigh on oil and defense names but lift European equities. Conversely, a breakdown in talks risks reigniting sanctions pressure and supporting energy prices. For now, the summit looks more like an opening gambit than a definitive endgame.

Last Week's Market Performance

Markets closed higher this week as investors priced in likely September Fed rate cuts and monitored Trump–Putin peace talks in Alaska. Inflation data drove headlines: July CPI came in hot while PPI spiked on tariff effects, reinforcing expectations for easing.

Earnings & Flows: Cisco reported, Berkshire revealed a new stake in UnitedHealth. 13F filings showed major fund moves.

Performance:

- Indices: Dow +1.7%, S&P 500 +0.9%, Nasdaq +0.8%, Russell 2000 +3.1%.

- Sectors: Healthcare (+4.6%) and Consumer Discretionary (+2.5%) led, while Staples (-0.8%) and Utilities (-0.8%) lagged.

- Global: Japan (+3.7%) outperformed; Europe and China posted moderate gains.

- Commodities: Oil (-1.7%) and Gold (-3.1%) declined.

- FX & Crypto: USD softened; Ethereum (+4%) outpaced Bitcoin (+1%).

Notables: Paramount Skydance (+31%), Intel (+23%), and UnitedHealth (+21%) topped S&P winners, while Applied Materials (-13%) and Cisco (-8%) lagged.

Upcoming Events This Week

Markets will focus on monetary policy signals, with the Fed’s Jackson Hole Symposium and FOMC minutes in the spotlight. Chairman Powell’s speech and remarks from dissenting members Waller and Bowman could shape expectations for rate cuts amid White House pressure and a mixed economic backdrop.

On the data side, the U.S. will release housing indicators (NAHB sentiment, permits, starts, and home sales) alongside flash PMIs and the Philly Fed index. Earnings from major retailers (Walmart, Target, Home Depot, Lowe’s, TJX) and tech names like Salesforce will also drive attention.

Internationally, investors will watch inflation reports from the UK, Canada, Japan, and South Africa, plus rate decisions in China, Sweden, New Zealand, and Indonesia. Canada’s calendar is packed with CPI, retail sales, PPI, and housing data.

.png)

Company News

LevelFields AI Stock Alerts Last Week

Intapp (INTA) +15.5% on $150M Buyback

Intapp gained more than 15% after unveiling a $150 million stock repurchase program, with management underscoring confidence in the company’s growth trajectory and balance sheet strength.

Citron Goes Short Palantir: “Valuation Is Absurd”

Famed short-seller Andrew Left of Citron Research is taking aim at Palantir after its 144% surge in 2025, calling the stock a “hype-driven narrative” with no precedent at current multiples. Palantir trades at nearly 80x sales and ~290x forward earnings, levels Left argues could see a 50–65% correction even if growth remains strong. While he acknowledged Palantir’s operational strength and AI leadership, he warned that retail-driven enthusiasm is fueling unsustainable momentum, echoing his past battles against meme stocks. The timing is notable: Citron went public with its short weeks after Palantir posted record quarterly earnings, signaling that valuation risk may now overshadow fundamentals in the bull case.

Intel Surges as U.S. Weighs Direct Stake in Chipmaker

Intel jumped after reports that the Trump administration is in talks to take an equity stake in the company, echoing the Pentagon’s recent $400M preferred equity investment in MP Materials. The move would provide Intel with crucial financial support to revive its long-delayed Ohio megafab project—once touted as the world’s largest semiconductor hub but recently pushed into the 2030s amid cost overruns and weak cash flow.

The potential deal follows a meeting between President Trump and Intel CEO Lip-Bu Tan, marking a sharp turnaround from just days ago when Trump called for Tan’s ouster over his China ties. Now, Tan appears set to stay on as the administration leans on Intel to anchor domestic chip capacity. The plan reflects a new model of state intervention, with Washington taking direct ownership stakes in strategic industries—ranging from rare earths to steel and now semiconductors—in order to insulate U.S. supply chains from geopolitical shocks.

For markets, the implication is clear: the White House isn’t just subsidizing reshoring—it’s nationalizing strategic risk. Intel, once the undisputed global leader but now fighting to regain its edge, may become the poster child for a broader industrial sovereignty push where defense, technology, and government finance converge.

.png)

Using AI to Spot Dividend Stocks

OPRX: 55% Growth Headed, Rule of 40 Pick

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai