.png)

L1 Weekly Stock Market News Analysis

October 12th, 2025

TLDR:

- Markets tumbled this week after President Trump announced a 100% tariff on Chinese goods and new export limits on U.S. software, reigniting trade tensions. The move followed China’s new restrictions on rare earth exports, raising fears of a wider economic clash and renewed supply chain shocks.

- The government shutdown entered its 12th day, halting key economic reports and leaving the Federal Reserve without data ahead of its next meeting — increasing the risk that rate cuts could be delayed.

- In crypto markets, over $19 billion in trades were wiped out in the largest liquidation event ever, as Bitcoin crashed sharply and panic selling spread across exchanges.

- Abroad, a U.S.-brokered Gaza ceasefire marked the most progress toward peace in two years, with Israel and Hamas agreeing to a hostage release and phased truce under Trump’s 20-point plan.

- Gold rose near record highs as investors sought safety, ending a volatile week defined by trade turmoil, data paralysis, and a rare diplomatic breakthrough.

-

White House Escalates Trade War: China’s Rare Earth Curbs Shake U.S. Markets

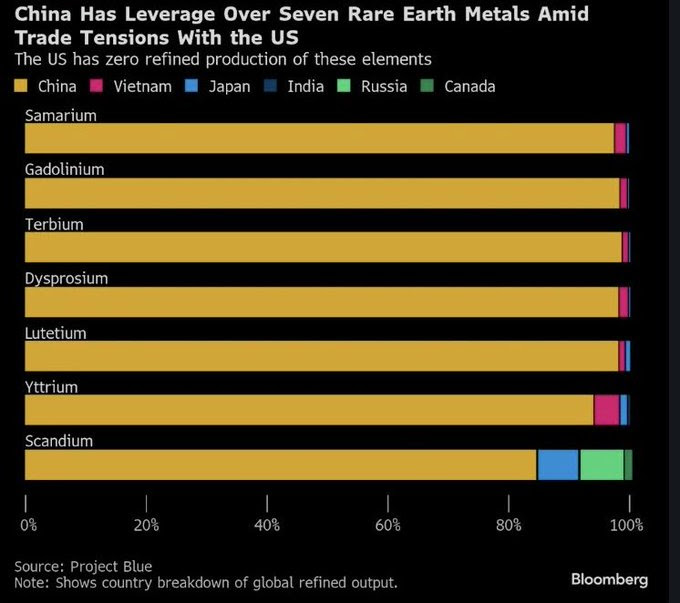

The U.S. government reignited tensions with China on Friday, accusing Beijing of becoming “very hostile” after China announced sweeping restrictions on exports of rare earth minerals — materials essential to everything from computer chips and electric vehicles to missiles and clean energy systems. The new rules require companies worldwide to get Chinese approval before shipping products that contain even trace amounts of these elements, effectively giving Beijing control over a critical link in the global supply chain.

Breakdown: China’s Newly Restricted Rare Earths Newly Restricted Rare Earths

- Neodymium (Nd) – Powers magnets in EV motors, wind turbines, and smartphones.

- U.S. source: MP Materials (MP) mines it in Nevada and plans to make magnets in Texas starting 2025.

- U.S. source: MP Materials (MP) mines it in Nevada and plans to make magnets in Texas starting 2025.

- Dysprosium (Dy) – Makes magnets stronger under high heat, key for EVs, drones, and jets.

- U.S. source: Energy Fuels (UUUU) is building facilities in Utah to separate and process it in the U.S.

- U.S. source: Energy Fuels (UUUU) is building facilities in Utah to separate and process it in the U.S.

- Terbium (Tb) – Used in lasers, sensors, and green lighting displays.

- U.S. source: Also part of Energy Fuels’ upcoming heavy rare earth program.

- U.S. source: Also part of Energy Fuels’ upcoming heavy rare earth program.

- Yttrium (Y) – Found in LEDs, radar, and missile guidance systems.

- U.S. source: Very limited; the U.S. still relies almost entirely on China.

- U.S. source: Very limited; the U.S. still relies almost entirely on China.

- Lanthanum (La) & Cerium (Ce) – Used in camera lenses, batteries, and catalytic converters.

- U.S. source: MP Materials (MP) produces both, but most refining still happens in China.

China’s decision immediately tanked the global technology sector. The restrictions could delay shipments for chip equipment makers like Applied Materials (AMAT) and raise costs for semiconductor producers such as Nvidia (NVDA) and Intel (INTC) that depend on magnets and other components containing these minerals. Prices for neodymium, dysprosium, and terbium are already expected to climb, raising costs across electronics and defense manufacturing.

Within hours, Trump responded by announcing an additional 100% tariff on all Chinese imports starting November 1, along with new export controls on “any and all critical software.” He called China’s actions an effort to “hold the world captive” and warned he might cancel his meeting with President Xi Jinping if the restrictions remain.

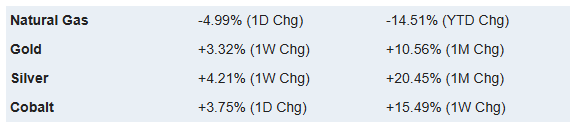

Markets sold off sharply on the news — the S&P 500 fell 2.7%, the Nasdaq dropped 3.5%, and soybean futures slid nearly 2%. Technology and semiconductor stocks led the decline, while gold and silver climbed as investors sought safety.

Market & Industry Impact

- Semiconductors:

- Losers: NVDA, INTC, AMD, QCOM, LRCX, AMAT — face higher input costs and possible delays due to rare earth shortages, hurting production and margins.

- Why: These firms depend on rare-earth-based magnets, lasers, and chemicals in chipmaking equipment.

- Chinese Tech & E-Commerce:

- Losers: Alibaba (BABA), JD.com (JD), Tencent (TCEHY) — could see weaker exports and cloud demand as U.S. tariffs and export bans restrict access to U.S. tech and software.

- Why: Tariffs raise import costs while export controls limit AI chips and critical software supplied to Chinese platforms.

- U.S. Rare Earth Producers:

- Winners: MP Materials (MP), Energy Fuels (UUUU), United States Antimony (UAMY), Perpetua Resources (PPTA), Trilogy Metals (TMQ), USA Rare Earth (USAR) — gain from domestic supply push and higher rare earth prices.

- Why: The U.S. and allies will look to them to fill gaps left by China’s export curbs.

- Defense & Energy:

- Winners: BWX Technologies (BWXT), Centrus Energy (LEU), Constellation Energy (CEG) — benefit from rising demand for U.S.-made materials used in reactors, satellites, and missile systems.

- Why: National security projects will prioritize domestic sourcing of strategic materials.

- Consumer & Manufacturing:

- Losers: Electronics and auto makers that depend on Chinese imports — Apple (AAPL), Tesla (TSLA) — face higher production costs and possible delays.

- Why: Tariffs and material shortages make it harder to maintain margins or meet demand.

Trump’s move marks the sharpest trade escalation since 2019, hitting just as the government shutdown stalls economic data. With trade, data, and manufacturing all under strain, investors face a new period of uncertainty — one where energy, defense, and domestic mining may rise, while tech and global supply chains come under pressure.

U.S. Expands Its Own Stakes in Critical Minerals

The trade standoff comes just days after the U.S. government announced a 10% stake in Trilogy Metals (TMQ) — the latest step in Trump’s push to secure domestic supplies of essential minerals. The $35.6 million investment supports Trilogy’s Upper Kobuk Mineral Projects (UKMP) in Alaska, rich in copper, zinc, gold, silver, and lead — vital for defense systems, clean energy, and data infrastructure.

The deal also reverses a Biden-era block on the Ambler Road, a 211-mile route needed to reach the mines in Alaska’s Brooks Range. Once built, it will connect one of North America’s largest untapped mineral regions to U.S. industry. Trilogy’s stock surged over 210% following the news.

Why Copper Matters So Much

Copper is one of the most important metals in the world — it powers electric cars, data centers, renewable energy, and defense systems. Demand is climbing fast, but global supply is falling behind.

Recently, major copper mines have been hit by accidents and protests — including a deadly mudslide at Freeport-McMoRan’s Grasberg mine in Indonesia, which wiped out over 500,000 tonnes of supply. Analysts say the world could face a major copper shortage by 2026 because not enough new mines are being built.

To show how big the demand is: Microsoft’s AI data centers use about 27 tonnes of copper for every megawatt (MW) of power. A single 500 MW data center needs around 13,000 tonnes of copper — enough to make millions of EV motors or power thousands of homes for a year.

This shortage makes U.S. copper projects much more important. Mines like Trilogy Metals’ Upper Kobuk project in Alaska could help reduce U.S. reliance on foreign supply and support energy, defense, and AI growth.

- Freeport-McMoRan (FCX) – Largest U.S. copper miner; key to grid and EV expansion.

- Trilogy Metals (TMQ) – Backed by U.S. government stake; developing Alaska’s Upper Kobuk copper and zinc mines.

- Taseko Mines (TGB) – Building the Florence Copper project in Arizona for domestic production.

- Ivanhoe Electric (IE) – Advanced U.S. copper exploration using 3D geophysics.

- Hudbay Minerals (HBM) – Developing the Mason copper project in Nevada.

The Bigger Picture

Trump’s recent actions — from partnerships and stakes in Intel, UAMY, MP Materials (rare earths), and Lithium Americas (lithium) to Trilogy Metals (copper and zinc) — show a clear strategic shift: the U.S. is no longer just funding key industries; it’s buying ownership in them.

By building a network of domestic mining and processing projects, Washington is laying the foundation for energy independence, defense readiness, and long-term control of critical resources — just as the next global trade war begins.

Level 2 users have already captured several major gains tied to this trend, including:

Rare Earth & Semiconductor Trades

- PPTA (3/20/26 $15 Calls): $5.40 → $8.90 | +64.8% in 24 days

- PPTA (Equity): $18.85 → $22.00 | +16.7% in 24 days

- INTC (1/16/26 $25 Calls): $3.45 → $7.60 | +120.3% in 34 days

- INTC (Equity): $24.72 → $32.50 | +31.5% in 34 days

Nuclear Energy Theme

- CCJ (3/20/26 $75 Calls): $14.15 → $22.20 | +56.9% in 29 days

- BWXT (Equity): $174.50 → $195.27 | +11.9% in 17 days

- BWXT (2/20/26 Calls): $22.00 → $35.00 | +59.1% in 14 days

- LEU (Equity): $191.65 → $297.00 | +55.0% in 25 days

We also release exclusive Level 2 Reports detailing high-impact trends such as the nuclear trade, data center infrastructure buildout, and U.S. strategic reserve expansion — each featuring actionable trade opportunities aligned with these policy-driven market shifts.

Last Week's Stock Market Performance

Over the past week, the S&P 500 finished the week down almost 3% and up 11.7% for the year to date. U.S. sectors displayed a predominantly downward trend with notable variations in performance. Utilities (XLU) stood out as the strongest performer, rising by 1.45% amid potential investor shifts toward defensive assets in a volatile environment. Consumer staples (XLP) remained relatively stable with a slight gain of 0.09%. Health care (XLV) experienced a moderate decline of 1.81%, while technology (XLK) dropped 2.22%, possibly influenced by broader market pressures on growth-oriented sectors. Financials (XLF) and industrials (XLI) fell by 2.90% and 3.08% respectively, indicating sensitivity to economic uncertainties. Materials (XLB), real estate (XLRE), and communications (XLC) each shed around 3.33%, with consumer discretionary (XLY) declining 3.83%. Energy (XLE) was the weakest, plunging 4.15%, likely due to concerns a renewed U.S.-China trade war will slow demand.

Metals and mining (XME) emerged as the biggest industry winner with a notable 3.40% gain, likely driven by strong commodity prices and industrial demand. The internet sector (FDN) followed as a top performer with only a minimal 0.62% decline, demonstrating stability in digital services during market volatility. Biotech (IBB) held relatively steady with a 1.32% drop, supported by ongoing innovation and healthcare needs, while gold miners (GDX) saw a 1.66% decrease but remained among the better performers due to gold's safe-haven status. On the other end, homebuilders (ITB) were the biggest loser with an 8.60% plunge. Oil services (OIH) dropped 6.97%, highlighting volatility linked to oil price swings, closely followed by oil and gas exploration and production (XOP) at a 6.93% decline amid similar energy sector challenges. Regional banks (KRE) fell 5.14%, potentially from economic uncertainties affecting lending, and MLPs (AMLP) rounded out the major losers with a 4.20% drop as energy infrastructure contended with broader headwinds.

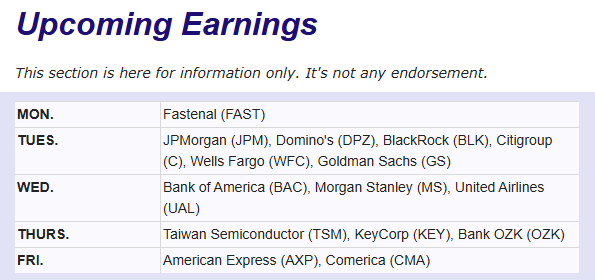

Upcoming Events This Week

Next week marks the start of earnings season, with major banks — JPMorgan, Goldman Sachs, Citigroup, Bank of America, Wells Fargo, and Morgan Stanley — set to report results.

The government shutdown will enter its third week, keeping key reports like CPI, PPI, and retail sales delayed. Traders will instead focus on updates still scheduled, including industrial production, the housing market index, and manufacturing surveys from the Philadelphia and New York Feds, along with the NFIB small business optimism report.

Fed Chair Jerome Powell is also expected to speak at the NABE Annual Meeting, offering clues on the central bank’s outlook. The bond market will close Monday for Columbus Day, while U.S. stock markets remain open.

.png)

Company News

LevelFields AI Stock Alerts Last Week

Spruce Biosciences (SPRB) +1,400% on FDA Breakthrough News

Spruce Biosciences (SPRB) surged over 1,400% in one day after the U.S. FDA granted Breakthrough Therapy Designation for its experimental enzyme replacement therapy, Tralesinidase Alfa (TA-ERT), which targets Sanfilippo Syndrome Type B (MPS IIIB) — a rare and deadly genetic disorder.

The designation fast-tracks development and review, signaling strong confidence in the drug’s potential and marking one of the biggest single-day gains for a biotech stock this year.

Crypto Crash: Record $19B Wipeout

Crypto markets suffered their worst crash ever after Trump’s new China tariff announcement sent shockwaves through global markets.

Bitcoin plunged from $126,000 to $105,000 within hours, while other major coins like Ethereum, Cardano, and Chainlink lost significant value.

Data from CoinGlass showed over $19 billion in crypto bets were wiped out — the largest one-day loss in crypto history, far surpassing the FTX collapse and COVID crash.

Much of the damage came from traders using borrowed money (leverage) to boost their bets. When prices fell, their positions were automatically sold to cover losses — triggering a cascade of forced selling that deepened the crash.

Crypto-linked stocks also tumbled: Coinbase (COIN) fell nearly 10%, and MicroStrategy (MSTR) dropped about 7% as investor panic spread. Even Trump’s own WLFI token sank nearly 50% before partially recovering.

The selloff showed how quickly the crypto market can unravel when heavy speculation meets sudden political shocks.

.png)

The Greatest Trades of All Time!

How Warren Buffet Used Events to Make Fortunes

How Are Robots Being Used Today for Business?

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai