.png)

L2 Weekly Stock Market News Analysis

October 19th, 2025

TLDR:

- Regional-bank jitters deepened: Zions and Western Alliance disclosed big hits tied to a failed SoCal borrower with disputed collateral, Jefferies flagged losses on a separate bankruptcy, and the KRE ETF had its worst week since 2023 as investors questioned how “secured” many small-bank loans really are.

- China risk cooled: After threatening steep tariffs, Trump dialed back his rhetoric and hinted at room for talks, easing fears of an immediate trade escalation. U.S. Treasury Secretary Bessent and China’s Vice Premier are set to meet in an effort to defuse the planned U.S. tariff hike.

- Metals surged: Gold and silver ripped to/near record highs on a classic flight to hard assets, fueled by bank stress, easier-policy expectations, and doubts about “paper” balance sheets.

- Fed tilt turned softer: Powell signaled quantitative tightening could stop “in coming months” and acknowledged a softer labor backdrop, reinforcing odds of further easing while the shutdown kept official economic data thin.

Regional Bank Meltdown: What Happened and Why It Matters

This week’s regional bank sell-off started with one bad loan and quickly turned into a bigger question: how many more are out there?

Two banks — Zions (ZION) and Western Alliance (WAL) — both took major hits from the same failed borrower, MOM CA Investco, a Southern California real estate group that went bankrupt earlier this year. Each thought they had first rights to the borrower’s assets, but when the dust settled, multiple lenders claimed the same collateral. What should have been a safe loan turned into a legal mess.

Zions wrote off about $50 million, and Western Alliance is trying to recover nearly $100 million through lawsuits. Then Jefferies (JEF) fell over 10% after revealing its own loan losses tied to a separate bankruptcy. Suddenly, investors started connecting the dots — Tricolor, First Brands, and now MOM CA — all pointing to the same issue: banks lending on shaky collateral and poor oversight.

Goldman Sachs told clients the phone “hasn’t stopped ringing,” with everyone asking the same thing:

- How did these loans get approved?

- Why are multiple “fraud” cases surfacing so close together?

- Are smaller banks loosening standards just to keep business flowing?

Behind the scenes, many regionals have quietly been loading up on NDFI loans — loans to nonbank lenders and private credit funds — now roughly 15% of total lending for some institutions. These are hard to value and even harder to unwind when things go wrong.

By week’s end, the KRE regional-bank ETF sank about 7%, its worst drop since the 2023 banking scare. The takeaway is simple: what started as one borrower’s default has exposed a deeper problem. Banks are realizing their “secured” loans might not be so secure after all.

How We Got Here

After years of easy money and fierce competition to lend, banks got comfortable taking bigger risks. They piled into loans tied to commercial real estate, subprime auto lending, and private credit funds — often using complex structures and cutting corners on oversight.

We flagged this back in February 2024 in our article “The Looming CRE Crisis: A Closer Look at OZK’s Vulnerability and Broader Banking Sector Implications.” That piece showed how smaller banks—responsible for about 70% of all U.S. commercial real estate loans—had taken on nearly $2 trillion in exposure. We pointed out that Bank OZK, in particular, had loan commitments more than five times its own equity, leaving it dangerously stretched. The warning was simple: when property values fall and refinancing costs rise, these banks don’t have much room to absorb losses.

That’s now playing out in real time. The bankruptcies of Tricolor (a subprime auto lender) and First Brands (an auto-parts supplier) have revealed how messy things get when too many lenders claim the same assets. MOM CA’s collapse showed the same pattern inside smaller banks — recycled collateral, questionable paperwork, and borrowers who took on more debt than they could handle while lenders stopped checking the details.

Higher interest rates have only made things worse. Borrowers who once could refinance easily are now defaulting, forcing banks to admit that many of their old loans are worth far less than they thought.

What It Means

Near-term stock impact

- Regional banks (KRE): expect continued volatility as auditors re-verify titles, liens, and cash accounts. ZION and WAL are the poster names.

- Jefferies (JEF): under pressure from First Brands exposure; management calls losses absorbable, but investors discount earnings quality until more is known.

- JPM / FITB: took Tricolor hits (~$170 M and $200 M respectively). Systemically fine—but even big banks missed red flags in complex collateral chains.

Bigger picture

- Tighter credit ahead. Regionals will slow lending and raise rates, especially in CRE and specialty finance.

- Loan-by-loan audits. Banks are re-checking collateral—painful, expensive, and likely to reveal new weak loans.

- Not 2008—but not nothing. Losses are in the hundreds of millions, not trillions, so far. The risk is a steady earnings drag and confidence erosion—and traders being a lot more jumpy should something more structural appear in the banking sector. For now, it's watch, wait, and hedge with hard assets for the big asset managers.

Whats Next

This isn’t a one-off. The same kinds of risky loans and sloppy paperwork that took down SVB and Signature Bank in 2023 have quietly built back up under new names. Now the cracks are showing again.

Level 2 users know this playbook well — we captured the downside on Signature’s collapse in March 2023, alerting users to buy one-month-to-expiration puts just five days before the stock plunged from $113 to $0, delivering a 987% gain. The setup then is the same as now: overextended banks, mispriced collateral, and misplaced confidence.

For years, regional banks stuffed their books with hard-to-sell loans — commercial real estate, subprime auto, and private credit — assuming nothing could go wrong. But when even one or two borrowers default, everyone scrambles to cover losses. One player sells assets at a discount, prices fall, and others are forced to mark down their own portfolios. That’s how contagion spreads — not through headlines, but through basic math and liquidity pressure.

We’re now in the stage where banks and investors are losing trust in their own marks. The lawsuits and fraud allegations popping up are really just a way to deflect blame. When you see multiple banks taking hits and calling them “isolated,” it usually means the problem is everywhere.

Here’s the short version of what likely comes next:

- More shoes to drop. Expect more surprise bankruptcies and loan write-downs before things stabilize. The same credit themes — subprime auto, CRE, and private-credit exposure — are likely to keep surfacing.

- Fed steps in (again). If losses widen, the Fed will likely move fast with rate cuts, emergency liquidity, or quiet backstops — even if inflation is still running hot. Policy prioritizes keeping credit flowing over keeping prices stable.

- Gold and silver keep running. The rush into hard assets is a classic flight to safety. As trust in balance sheets fades, investors move out of currrency that can devalue into things they can hold — metal, minerals, and real-asset equities.

- Regional banks shrink. Smaller lenders will likely keep tightening credit, raising borrowing costs, and in many cases, merging or disappearing altogether.

- Be selective in equities. Focus on companies with strong balance sheets and tangible assets — miners, industrials, and energy producers — rather than credit-heavy sectors.

- Don’t chase parabolic rallies. Gold and stocks have both run fast; short-term pullbacks are likely as wealth managers rebalance portfolios to meet allocation percentiles. But the long-term setup still favors real assets over leveraged growth plays.

- Stay cautious on banks. Easy money props up valuations, not loan quality. Expect more surprises before confidence truly returns.

It’s not the end of the system—but it is the market finally calling out years of optimism.

Areas to Avoid (for now)

- Subprime Auto Lenders

- Delinquencies are rising while used-car prices fall and funding costs stay high.

- Names: CVNA, CACC, ALLY, SC

- Stick with OEMs that have clean balance sheets.

- The Banks That Finance Them

- Warehouse lines and securitizations can unravel quickly when redemptions hit.

- Names: JEF, ALLY

- Watch for widening ABS spreads — an early warning sign of stress.

- Regional Banks with CRE or Specialty Credit

- Thin diversification and deposit risk make these names volatile.

- Names: KRE ETF constituents

- Key tell: rising non-performing loans or lawsuits over liens and titles.

- Commercial Real Estate Heavyweights

- Office vacancy, refinancing walls, and falling property values remain unresolved.

- Names: SLG, BXP, VNO

- Focus on debt maturities and any distressed asset sales.

- Buy-Now-Pay-Later (BNPL)

- Consumers are overextended, and these lenders rely on fragile funding lines.

- Names: AFRM, SQ, SEZL

- Defaults could spike quickly if credit-card delinquencies keep rising.

- Speculative “Story” Tech (Quantum, etc.)

- Valuations built on hype, not earnings — long runway to real profits.

- Names: IONQ, RGTI

- Momentum-driven trades only; little to no downside protection.

- Levered Crypto or Stablecoin Plays

- First to crack during liquidity squeezes.

- Keep only small, unlevered BTC/ETH exposure for the long term.

- Student-Loan Servicers & Lenders

- Rising delinquencies meet unpredictable policy shifts.

- Names: NAVI, NNI, SLM, SOFI

- Widening student-loan ABS spreads signal increasing credit stress.

Last Week's Stock Market Performance

Upcoming Events This Week

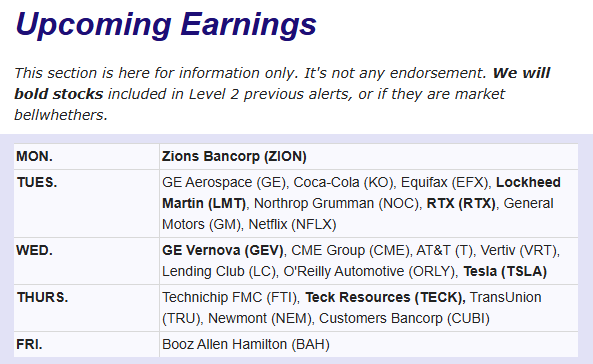

In the week ahead, investors will be balancing earnings, inflation, and global macro data against the backdrop of a still-frozen U.S. government. The federal shutdown is expected to enter its fourth week, but traders will still get one key release: Friday’s CPI report, where headline inflation is projected to rise to 3.1% while core inflation holds steady at 3.1%. Alongside that, fresh readings on S&P Global PMIs, existing home sales, and the Chicago Fed activity index will offer clues on how the economy is holding up under higher rates. Corporate earnings will dominate the headlines, with major reports from Tesla, Procter & Gamble, General Electric, Coca-Cola, Netflix, IBM, AT&T, Verizon, Intel, Ford, and Blackstone expected to drive sector-specific volatility.

.png)

Company News

LevelFields AI Stock Alerts Last Week

Spruce Biosciences (SPRB) +1,400% on FDA Breakthrough News

Spruce Biosciences (SPRB) surged over 1,400% in one day after the U.S. FDA granted Breakthrough Therapy Designation for its experimental enzyme replacement therapy, Tralesinidase Alfa (TA-ERT), which targets Sanfilippo Syndrome Type B (MPS IIIB) — a rare and deadly genetic disorder.The designation fast-tracks development and review, signaling strong confidence in the drug’s potential and marking one of the biggest single-day gains for a biotech stock this year.

Trump, Tomahawks, and the Next Defense Play

President Trump’s recent meeting with Ukraine’s Zelenskyy made headlines for what didn’t happen: the U.S. stopped short of sending Tomahawk missiles, with Trump saying he wants both sides to “stop at the battle line.” But behind the diplomacy is a supply problem — and a potential business opportunity.

According to military analysts cited by ZeroHedge and the Financial Times, the Pentagon has only a few dozen Tomahawks left to spare after heavy use. Out of roughly 4,000 total missiles, only 20–50 could be sent to Ukraine, far too few to shift the war. Production is lagging, and the U.S. defense stockpile is running low as demand spikes worldwide.

That shortfall creates an opening for Lockheed Martin (LMT) and Raytheon (RTX), the primary manufacturers of Tomahawks and precision strike weapons. Trump’s emphasis on “America First” defense and past moves to take direct U.S. stakes or long-term production contracts in strategic industries (as seen in lithium and rare-earths) make a similar model likely for missile manufacturing. A government equity position or guaranteed supply contracts would ensure control over production while rebuilding depleted arsenals.

If that happens, Lockheed Martin stands to benefit first — it already produces key systems like the JASSM, HIMARS, and next-generation hypersonics. A new replenishment initiative or government-backed expansion deal could push order books and margins higher heading into 2026.

Investor takeaway: The U.S. can’t meet defense demands without rebuilding domestic missile capacity. Trump’s approach — limiting exports while rebuilding at home — suggests a new cycle of state-backed defense production. For investors, that points toward Lockheed Martin (LMT) and Raytheon (RTX) as quiet winners of the Tomahawk shortfall and the next wave of “America First” defense policy.

.png)

The Greatest Trades of All Time!

How Warren Buffet Used Events to Make Fortunes

How Are Robots Being Used Today for Business?

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai