.png)

L2 Weekly Stock Market News Analysis

March 8th, 2026

TLDR:

Markets entered March facing two major forces: escalating geopolitical risk in the Middle East and renewed focus on inflation data that will shape Federal Reserve expectations.

Tensions intensified after U.S. and Israeli strikes expanded to Iran’s energy infrastructure, including fuel depots and refinery facilities near Tehran. The attacks sent flames and smoke across parts of the capital and raised concerns about disruption to energy supply chains tied to the Persian Gulf. Because roughly 20% of global oil supply moves through the Strait of Hormuz, markets are watching closely for any escalation that could affect shipping or insurance costs for tankers. Energy prices and volatility tend to react first in these scenarios, making oil markets the key signal to watch.

At the same time, markets are turning their attention back to inflation. February CPI and January PCE will be the most important economic releases this week, with inflation expected to hold near 2.5% annually. Investors are watching for confirmation that price pressures remain stable enough to keep the Federal Reserve on track for potential easing later this year.

Sector performance reflected a more defensive tone. Energy (XLE) led the market with a +2.60% gain, followed by Communication Services (XLC) +1.47%, while most other sectors declined. Consumer Staples (XLP) fell –3.88% and Materials (XLB) dropped –4.09%, while Industrials (XLI) and Financials (XLF) also saw notable losses. The pattern suggests investors rotated toward energy exposure tied to geopolitical risk while reducing exposure across much of the broader market.

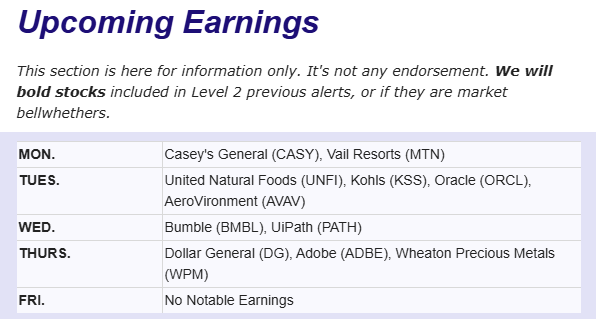

Looking ahead, markets will focus on CPI, PCE, GDP revisions, housing data, and consumer sentiment, all of which will help shape expectations for interest rates and economic momentum. Earnings from Oracle, Hewlett Packard Enterprise, Adobe, UiPath, and Wheaton Precious Metals will also provide insight into enterprise technology spending and commodity markets.

A Strategic Playbook Is Emerging

Over the past year, U.S. foreign policy has increasingly emphasized several consistent priorities: securing energy supply chains, reinforcing Western Hemisphere influence, limiting rival powers’ access to critical resources, and strengthening alliances in the Indo-Pacific.

Those priorities are not hypothetical. They appear directly in the current U.S. national security framework, which frames energy, minerals, and supply chains as core components of national power.

They also reflect a theme President Trump emphasized repeatedly during the 2024 campaign and early in his second term: countering efforts by the BRICS bloc to reduce reliance on the U.S. dollar and build alternative financial systems. Trump warned that countries attempting to replace the dollar with a new BRICS-linked currency could face major tariffs and trade consequences, underscoring how central dollar dominance is to U.S. economic strategy.

What is notable now is how several seemingly separate geopolitical events begin to fit together.

Pressure on Venezuela, growing alignment across North America, escalating tensions with Iran, and stronger military coordination with Indo-Pacific allies are often discussed as isolated developments.

Viewed together, they suggest a broader strategic sequence shaping global energy flows and geopolitical leverage.

The Strategic Sequence

Step 1: Venezuela

Pressure on Venezuela targets more than domestic politics.

The country sits on the largest proven oil reserves in the world, along with significant deposits of lithium, gold, and rare earth minerals — resources that are increasingly critical for energy systems, defense technologies, and industrial supply chains.

For years, China has been the largest buyer of Venezuelan crude, importing roughly 470,000 barrels per day in 2025, with Chinese firms also investing billions in the country’s oil sector.

Even after U.S. sanctions, shipments often continued through shadow tanker networks and relabeled cargoes, allowing Chinese refiners to buy heavily discounted oil.

In other words, Venezuelan crude became one of the ways China secured cheap energy outside Western financial channels.

If those flows are disrupted or redirected, that supply cushion weakens.

Step 2: Canada

This step is quieter but strategically significant.

North America increasingly functions as an integrated energy and economic bloc — combining Canadian oil and gas production, American capital markets, and continental manufacturing capacity.

Canada holds the world’s third-largest oil reserves, vast mineral deposits, and expanding Arctic shipping routes.

Closer alignment between Washington and Ottawa strengthens access to energy, minerals, and logistics across the entire continent.

That kind of integrated resource base creates a geopolitical advantage few rivals can replicate.

Step 3: Greenland

Greenland is less about symbolism and more about access.

What began as a territorial flashpoint increasingly looks like a negotiation over strategic positioning, Arctic access, and critical minerals rather than formal ownership. The broader objective appears to be securing deeper U.S. influence over an area that matters for missile defense, Arctic shipping lanes, and future resource development.

That matters because Greenland sits atop one of the world’s more important untapped stores of critical minerals, including rare earth elements, graphite, uranium, titanium, and other inputs needed for defense systems, energy infrastructure, and advanced manufacturing. As Arctic ice continues to melt, the island also becomes more important as a logistics and surveillance hub tied to northern shipping routes and military positioning.

In practical terms, Greenland fits the same broader pattern as the rest of this strategy: expand U.S. influence over strategic geography, secure future access to critical resources, and prevent rival powers — especially China and Russia — from gaining a foothold in a region growing more valuable over time.

Step 4: Iran

With Venezuelan supply already compromised by U.S. intervention and oversight, China’s next major source of discounted oil is Iran.

China has become the primary buyer of Iranian crude, receiving roughly 90% of Iran’s oil exports through intermediaries and sanctions-evasion shipping networks. That relationship has been central to Beijing’s energy strategy, with Iranian barrels often sold below global prices, making them especially attractive to Chinese refiners.

But the Middle East escalation now puts that supply at risk.

Recent U.S.–Israeli strikes have begun directly targeting Iran’s energy infrastructure, including fuel depots, storage facilities, and transfer centers around Tehran and nearby provinces. Attacks on sites such as the Shahran oil depot, the Tehran refinery, and major storage facilities signal a shift toward disrupting the logistics that move fuel and crude across the country.

Even limited damage to storage and distribution infrastructure can slow exports, complicate shipping logistics, and increase insurance and transport risks for tankers carrying Iranian oil.

Iranian crude accounts for roughly 13% of China’s seaborne imports, and instability around the Persian Gulf threatens an even larger share of global oil flows passing through the Strait of Hormuz.

The strategic effect is straightforward:

With Venezuelan supply already constrained and Iranian export infrastructure now under pressure, two of China’s largest sources of discounted oil tighten at the same time.

That forces Beijing to compete more directly for global supply—often from producers aligned with the United States and its partners—shifting leverage back toward Western energy markets.

Image Below: Massive flames and thick smoke rise over Tehran after Israeli strikes hit Iranian fuel depots and oil infrastructure, leaving parts of the city covered in smoke and reports of toxic, oil-laden “acid rain” falling across the capital.

Step 5: Russia

Russia remains one of the most important swing suppliers in global energy markets.

Since Western sanctions were imposed, Russia has redirected much of its oil exports toward Asia — particularly China and India — often at discounted prices. These discounted barrels have become an important part of China’s energy strategy, helping offset supply risks from sanctioned producers like Iran and Venezuela.

But Russia’s role also highlights how fragmented global energy markets have become. Sanctions, shipping restrictions, insurance rules, and payment systems increasingly determine where oil can move and at what price.

If pressure rises across multiple sanctioned suppliers at the same time — Russia, Iran, and Venezuela — China’s access to discounted crude becomes less secure. That doesn’t require a geopolitical realignment. It simply means Beijing would face tighter competition for global supply, increasing the strategic value of Western and allied energy production.

The Bitcoin + Stablecoin Layer

The final layer of the sequence is financial.

Energy shocks and rising defense spending historically push capital toward hard assets. In a fragmented geopolitical environment, Bitcoin would likely absorb part of that liquidity as a neutral asset outside traditional banking systems.

But Bitcoin alone isn’t the structural shift.

Stablecoins are.

Dollar-pegged stablecoins already move tens of billions of dollars across borders daily, allowing companies and traders to settle transactions instantly without relying on traditional banks or payment networks.

The GENIUS Act quietly builds the legal framework for this system. It classifies payment stablecoins as payment instruments rather than securities and requires them to be fully backed by reserves such as cash, bank deposits, or short-term U.S. Treasuries.

That design has a powerful implication:

Every new stablecoin issued effectively creates additional demand for U.S. Treasury reserves and dollar liquidity.

Instead of weakening the dollar system, stablecoins may extend it globally — allowing digital dollars to circulate anywhere while the underlying reserves remain anchored in the U.S. financial system.

In that architecture:

- Bitcoin (or another crypto) becomes the neutral reserve asset

- Stablecoins become the global transaction rails

- U.S. Treasuries remain the reserve backing the system

A geopolitical reset would likely accelerate adoption dramatically.

Stablecoins wouldn’t just survive that transition.

They would become the rails it runs on.

Positioning for the Strategic Shift

If this sequence continues, the investment implications center on energy security, critical minerals, defense spending, and financial infrastructure tied to the dollar system.

Energy Producers

If discounted supply from Venezuela and Iran tightens, global markets increasingly rely on Western producers. That favors companies with large reserves and scalable output such as Exxon Mobil, Chevron, Suncor Energy, ConocoPhillips, and EOG Resources.

Uranium and Energy Security

Fragmented energy markets also strengthen the case for nuclear baseload power. Key players include Cameco, one of the world’s largest uranium suppliers, and Centrus Energy, which provides enriched uranium fuel for reactors.

U.S.-focused producers such as Energy Fuels also benefit from policies aimed at rebuilding domestic nuclear fuel supply chains.

Critical Minerals

Supply chain competition also increases the value of domestic mineral production. Companies tied to rare earths and strategic metals include MP Materials, U.S. Antimony, and Perpetua Resources.

Defense

Rising geopolitical tensions typically translate into higher defense spending, benefiting contractors such as Lockheed Martin, Northrop Grumman, and RTX Corporation.

Digital Dollar Infrastructure

If stablecoins expand as global settlement rails, companies tied to crypto infrastructure could benefit. Coinbase Global operates one of the largest digital asset exchanges and blockchain infrastructure platforms, while MicroStrategy functions as a leveraged proxy for Bitcoin exposure through its large holdings.

Last's Weeks Sector Winners & Losers

Sector performance turned more defensive last week as investors rotated away from cyclicals and into energy and communication services.

Energy (XLE) led the market, rising +2.60%, followed by Communication Services (XLC) +1.47%, making them the only sectors to post gains.

Most other sectors declined, with Consumer Discretionary (XLY) –0.43%, Utilities (XLU) –0.59%, and Information Technology (XLK) –0.59% seeing modest losses.

Weakness was more pronounced in economically sensitive areas. Industrials (XLI) fell –2.63%, Financials (XLF) dropped –2.42%, and Health Care (XLV) declined –2.23%.

The largest declines came from Consumer Staples (XLP) –3.88% and Materials (XLB) –4.09%, reflecting pressure across defensive consumption and commodity-linked sectors.

Overall, the pattern suggests investors favored energy exposure tied to geopolitical risk while broadly reducing exposure across the rest of the market.

Upcoming Events This Week

This week will focus on inflation, economic momentum, and geopolitical developments, all of which could shape expectations for Federal Reserve policy and global energy markets.

The February CPI report will be the main event, with inflation expected to edge up slightly to around 2.5% annually while monthly price growth holds near 0.2%. Investors will also watch the January PCE report—the Fed’s preferred inflation measure—for confirmation that price pressures remain stable.

Markets will also track the second estimate of Q4 GDP, durable goods orders, and housing data including building permits, housing starts, and existing home sales for signals about economic momentum and the impact of high borrowing costs. Labor and sentiment indicators such as JOLTS job openings and the University of Michigan consumer sentiment survey will provide additional clues about the strength of the labor market and consumer spending.

The key question for markets: Will inflation remain stable enough to keep the Fed on track for potential easing later this year while geopolitical tensions continue to pressure energy prices?

On the corporate side, earnings from Oracle, Hewlett Packard Enterprise, Adobe, UiPath, and Wheaton Precious Metals will offer insight into enterprise technology spending and commodity markets.

Company News

LevelFields AI Stock Alerts Last Week

Ziff Davis (ZD) +48% — $1.2B Connectivity Division Sale

Ziff Davis surged 48% in one day after announcing a definitive agreement to sell its Connectivity division to Accenture for $1.2 billion in cash.

The sale allows the company to monetize a major business segment and significantly strengthen its balance sheet with a large cash infusion. Investors reacted positively to the strategic move, viewing the transaction as a way to unlock value and potentially support future capital returns or reinvestment into higher-margin segments of the business.

Cohen & Company (COHN) +36% — Dividend Increase and Special Dividend

Cohen & Company jumped 36% in one day after its board approved a $0.25 quarterly dividend along with a $0.70 special dividend, both payable April 3, 2026, to shareholders of record on March 20.

The announcement signaled strong capital positioning and management’s willingness to return excess cash to shareholders, driving the sharp move higher as investors responded to the large combined payout.

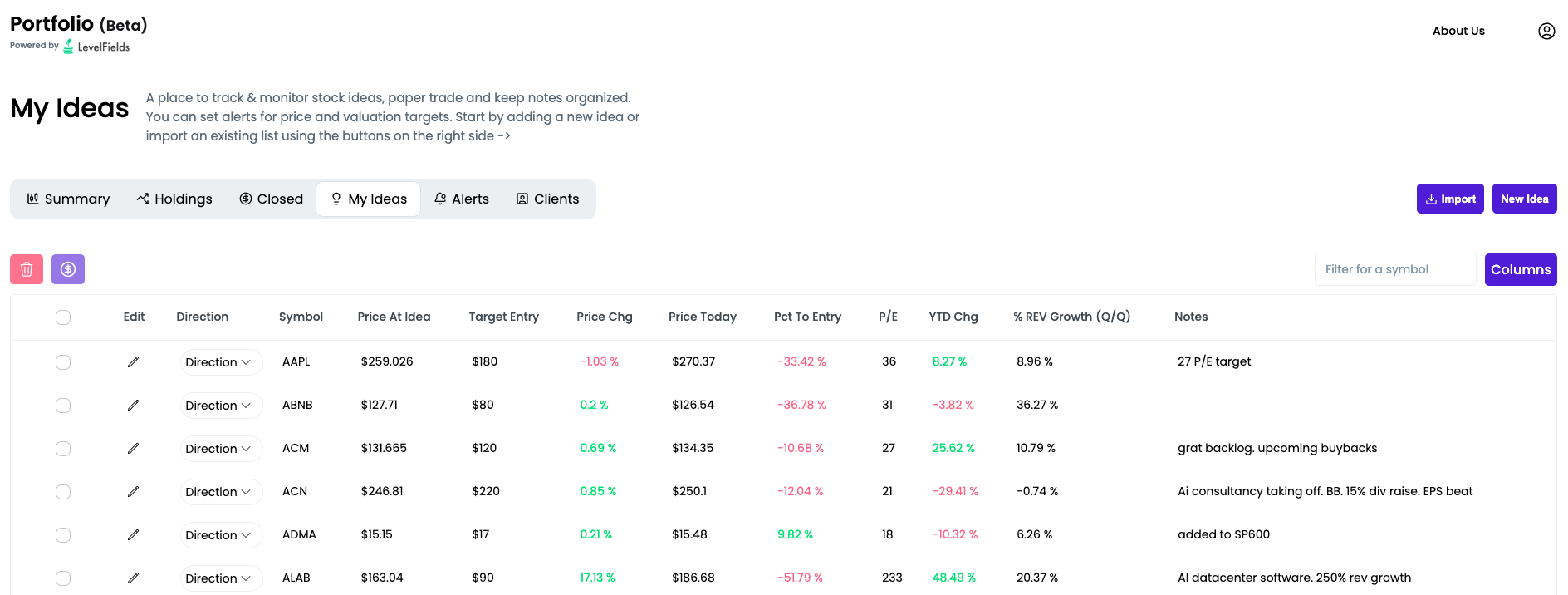

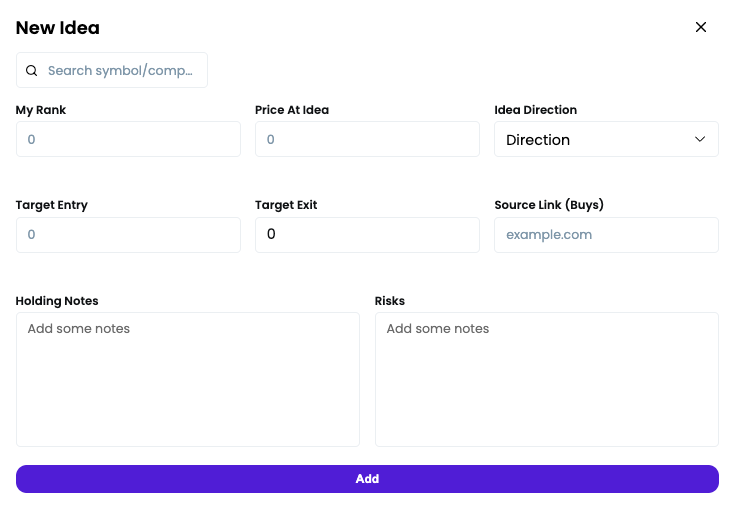

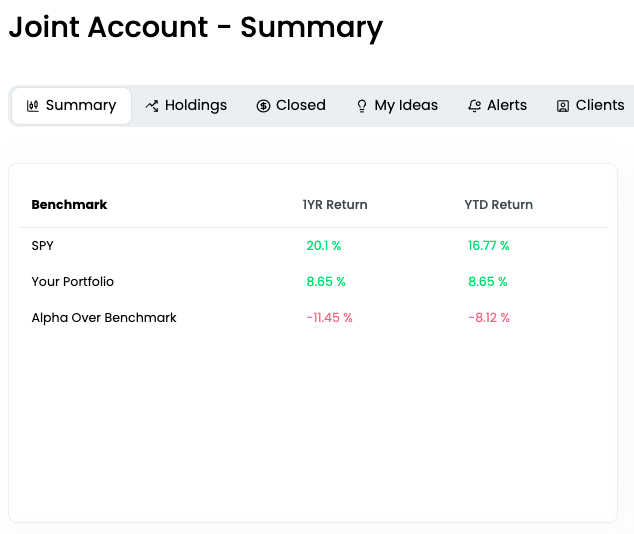

Introducing the LevelFields Portfolio Tracker

We’ve just launched the new LevelFields Portfolio platform — a centralized dashboard built for active investors and wealth managers to track their trades, organize trade ideas, and monitor real or prospective portfolios.

We've replaced Excel and Google Sheets trade tracking with software that updates as prices and valuations of stocks change, so you don't lose money by missing great entry and exit points.

You can sign up for free!

What it does:

- Lets you add both real positions and idea-stage trades into one unified portfolio.

- Tracks allocation, profit/loss, KPIs, P/E, price targets, and thesis notes in one place.

- Allows you to set real-time alerts on valuation changes, price moves, and price targets using bulk editing (e.g. one alert for all holdings).

- Lets you toggle any ticker between “Idea → Holding → Closed” while preserving the original trade thesis and exit notes.

- Designed for traders, advisors, and fund managers who need a live, organized view of positions + rationale, not just a static spreadsheet of tickers.

- Import CSV file of existing ideas, notes, and portfolio holdings for a quick start

- Keep track of reasons you bought and sold to analyze your performance and for compliance

- Design your own model portfolios based on allocations, sector, and industry

-

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai