.png)

L2 Weekly Stock Market News Analysis

April 6th, 2026

TLDR:

Markets head into the week with momentum stabilizing after a sharp stretch of selling, but the setup remains fragile. Stocks just posted their first weekly gain in six weeks, yet the S&P 500 is still down nearly 6% from its late-January high, and direction continues to follow oil prices and headlines out of the Middle East.

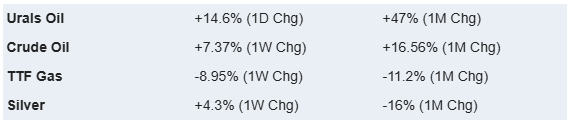

Energy remains the dominant driver. Crude is holding above $110, with the Strait of Hormuz still operating below normal capacity, keeping supply tight and uncertainty elevated. That continues to feed through to gasoline prices, inflation expectations, and overall market sentiment.

At the same time, the Fed has limited flexibility. March payrolls came in solid at 178,000 with unemployment at 4.3%, reinforcing the case for a hold. This week’s CPI and FOMC minutes now carry more weight as markets look for clearer evidence of how much higher energy costs are feeding into inflation.

Private credit remains a secondary risk in the background. While Powell noted the Fed is monitoring the space, it has not yet signaled broader concern, leaving it as a developing rather than immediate issue.

The focus this week is whether improving positioning and the start of earnings can support the recent bounce, or if another move higher in oil alongside firm inflation data puts pressure back on equities.

The Bounce Was Expected — But It Was Driven By Positioning, Not A Change In The Story

Last week’s rally was sharp, but it did not come out of nowhere.

After five straight weeks of declines, the market had become stretched enough that a rebound was likely. That tends to happen in periods like this. Some of the strongest market days usually happen very close to the worst ones because heavy selling, fear, and short positioning create moves that reverse quickly once the pressure starts to ease.

That was the setup coming into last week.

Stocks had fallen below key levels, sentiment had turned defensive, and a lot of the selling had already happened in a short period of time. Once that selling pressure began to exhaust itself, the rebound followed. Tuesday’s rally ended up being one of the strongest single days since 2022, which fits that pattern of reflexive bounces happening in weak markets rather than healthy ones.

That distinction matters.

This was not a rally driven by better earnings, lower oil, or a clear improvement in the macro backdrop. It was mostly a rally driven by how far and how fast the market had already fallen. In other words, the move was real, but the reason for it was technical and positional rather than fundamental.

That does not automatically make it fake or meaningless. It simply means the bounce, by itself, does not answer the bigger question of whether the market has actually found a durable floor.

When the main argument for a rally is that “stocks were down a lot and people were scared,” that is only a short-term explanation. It can produce a strong move, but it does not last unless something underneath it improves.

And underneath it, not much has changed.

Oil is still elevated. The effects of higher gasoline and energy costs are still moving through the economy. Private credit stress has not gone away. Questions around AI spending and broader growth remain unresolved. So while the market got a bounce, the pressures that drove the correction are still sitting there.

That is why the move is better understood as a reset after heavy selling, not proof that the market has turned the corner.

The Bigger Issue Is Still Ahead — Earnings And Expectations Have Not Fully Adjusted

If last week’s move was driven by positioning, the next phase comes down to expectations.

Earnings forecasts still reflect a stronger environment than what markets are currently facing. Right now, analysts expect companies in the S&P 500 to collectively earn about $309 per share in 2026, which is essentially a bet on steady economic growth, manageable costs, and stable demand.

The issue is that those assumptions were made before the recent rise in oil prices and broader cost pressures. If energy stays elevated or growth slows, those profit expectations may be too high.

When that happens, the adjustment usually comes through earnings revisions — analysts lowering their estimates as companies report and update guidance. Markets don’t wait for the earnings to actually drop; they tend to reprice as soon as expectations start moving lower, which is why changes in forecasts often matter more than the numbers themselves.

That process rarely happens all at once. It typically unfolds gradually, then accelerates as companies begin reporting and updating guidance. As those revisions come through, they tend to reset how the market is priced, which is why the difference between a durable recovery and a short-term bounce usually shows up in fundamentals rather than price action alone.

The technical backdrop also hasn’t fully recovered. The market remains below its 200-day moving average, and historically, breaks below that level that aren’t quickly reversed have more often led to further downside than immediate recoveries. With only a few weeks since that break, there hasn’t been enough time to confirm whether the recent move has repaired that damage or simply paused it.

At the same time, this isn’t a one-sided setup. Most corrections don’t turn into full bear markets, and rebounds are common once selling pressure exhausts itself. The recent rally fits that pattern — a reset after a sharp decline — but it doesn’t, on its own, confirm that the broader correction is over.

What matters now is how expectations adjust. If companies hold up better than feared and cost pressures stabilize, the market can build on this rebound. If earnings estimates begin to move lower while oil remains elevated, the recent strength is more likely to prove temporary.

The shift is from positioning to fundamentals. Last week relieved pressure. The next move will depend on whether the underlying outlook begins to align with it.

Image below shows that the market doesn’t just react to earnings levels—it tracks the change in earnings, with drawdowns consistently lining up with periods where forward EPS turns negative. In practice, markets tend to bottom before earnings do, but sustained upside usually doesn’t happen until earnings revisions stabilize and turn higher.

Rising Pressure on Iran Keeps Multiple Market Outcomes in Play

Trump’s latest comments have added pressure on Iran while negotiations continue, keeping both escalation and a potential deal in play.

Over the weekend, he set a new deadline for Tuesday evening for reopening the Strait of Hormuz and warned that energy infrastructure could be targeted if talks break down. At the same time, negotiations are still ongoing, with several countries pushing for a temporary ceasefire. That combination matters—because it keeps risk elevated without locking markets into a single outcome.

You can see that in how assets are trading.

Oil remains elevated after rising more than 50% since the conflict began, gasoline prices have moved back above $4, and shipping through Hormuz is still significantly below normal levels. But at the same time, equities have started to stabilize and even rebound modestly on signs that talks are still active. That’s not a market pricing escalation alone—it’s a market balancing disruption against the possibility of resolution.

Trump’s address last week added to that tension. He described the conflict as nearing completion, while also repeating that further strikes remain on the table if a deal isn’t reached. That kind of mixed signaling doesn’t resolve uncertainty—it extends it.

The initial liquidation phase appears to have run its course, but there’s no clear conviction behind the rebound. Volatility has eased off recent highs, flows have stabilized, and leadership has become less one-sided, which typically happens after the first leg of a selloff. But markets are still reacting to headlines rather than trending on fundamentals.

If the Strait remains constrained and oil stays elevated, the current setup holds: energy and commodities remain supported by supply disruption, and inflation pressure stays in focus.

If conditions begin to ease—even partially—the pressure points reverse, and a different set of trades starts to matter:

- Rates / Duration (TLT): Lower oil would ease inflation pressure and reduce upward pressure on long-term yields.

- High-duration equities that typically benefit from falling yields include growth/tech names like MSFT, NVDA, AAPL, as well as rate-sensitive software (IGV ETF)

- Homebuilders (DHI, LEN) and REITs (PLD, AMT) also tend to respond positively to lower rates

- Utilities (NEE, DUK) often act as bond proxies and benefit from declining yields

- Biotech (XBI): Has held up relatively well and tends to benefit from improving liquidity and lower discount rates

- Examples: VRTX, REGN, MRNA

- China / EM (FXI, EWZ): Stabilizing global growth and lower energy stress support flows

- China large caps: BABA, JD

- Brazil/commodities: VALE, PBR

- Consumer (XLY): Lower fuel costs and easing inflation support spending

- Discretionary: AMZN, TSLA, HD

- Travel/leisure (fuel-sensitive): DAL, UAL, RCL

Last's Weeks Sector Winners & Losers

Sector performance last week showed a shift away from energy leadership, with gains concentrated in defensives and real assets.

Materials (XLB) led the market, rising +2.13%, followed by Utilities (XLU) up +1.90% and Real Estate (XLRE) gaining +1.69%. Health Care (XLV) also held firm, up +1.02%, while Financials (XLF) were modestly positive at +0.20%.

On the downside, Energy (XLE) was the weakest sector, falling -2.64% despite elevated oil prices, suggesting positioning and profit-taking played a larger role than fundamentals. Technology (XLK) also lagged, down -1.35%, alongside Consumer Discretionary (XLY) at -0.84% and Industrials (XLI) at -0.41%.

Communication Services (XLC) slipped -0.18%, while Consumer Staples (XLP) were essentially flat, down just -0.06%.

Overall, the pattern points to a rotation into more defensive and rate-sensitive areas, while prior leaders—particularly energy and growth—saw some unwind. The move suggests positioning is beginning to reset even as the macro backdrop remains largely unchanged.

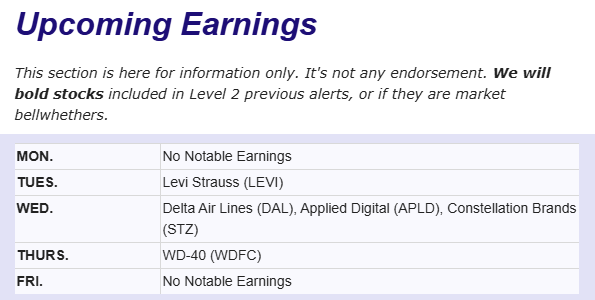

Upcoming Events This Week

This week remains centered on the Middle East and oil, but Tuesday is now the key swing day. Trump said Iran has 48 hours to reach a deal and reopen the Strait of Hormuz, with a deadline extended to Tuesday at 8:00 p.m. ET. He also warned that Iranian power plants and bridges could be targeted if no deal is reached, which matters because any escalation tied to energy infrastructure or Hormuz access could quickly push oil prices higher.

In the U.S., Wednesday’s Fed minutes will show how policymakers were thinking about inflation and rates before the latest move in oil. Thursday brings the Q4 GDP third estimate and February personal income/outlays, while Friday’s CPI report is the main macro event of the week because it will give markets a cleaner read on inflation as energy prices stay elevated.

Globally, Tuesday’s Eurozone retail sales, Wednesday’s RBNZ decision, and Friday’s China CPI/PPI will help shape the next read on growth and inflation outside the U.S.

Company News

LevelFields AI Stock Alerts Last Week

Apellis Pharmaceuticals (APLS) +129% — $5.6B Buyout DealApellis surged after agreeing to be acquired by Biogen in a deal worth about $5.6 billion. Shareholders are set to receive $41 per share in cash plus up to $4 per share in milestone payments tied to Syfovre sales, with the deal expected to close in Q2 2026.

Investors reacted to the size of the premium and the fact that the deal locks in value far above where the stock had been trading. The acquisition also brings Biogen two commercial drugs, Syfovre and Empaveli, which generated about $689 million of combined revenue last year and are expected to keep growing.

Franklin Covey (FC) +45.82% — Earnings Strength + BuybackFranklin Covey jumped after reporting fiscal Q2 2026 results that showed $59.6 million in revenue, 7% growth in Enterprise North America invoiced amounts, deferred revenue up 7% to $101.5 million, and adjusted EBITDA up 99% to $4.1 million. The company also bought back $17.0 million of stock during the quarter and kept full-year guidance unchanged.

Investors focused less on the headline net loss and more on the improvement underneath the business. Better invoicing, higher deferred revenue, stronger free cash flow, and a meaningful buyback all pointed to improving demand and better execution, which helped drive the sharp move higher.

Lantern Pharma (LTRN) +10.93% — Earnings Update + Pipeline ProgressLantern moved higher after reporting fourth-quarter and full-year 2025 results alongside updates across its AI-driven cancer pipeline. The company highlighted continued progress in its LP-300 Phase 2 trial, completion of Phase 1a for LP-184, and a 19% year-over-year reduction in total operating expenses.

Investors responded to the combination of lower costs and real pipeline progress. In this market, small biotech names need to show both discipline and momentum, and Lantern did that with tighter spending, multiple clinical milestones, and a broader push to grow the commercial reach of its RADR AI platform. Cash remains something to watch, but the update was strong enough to support the stock’s move higher.

Other Company News

Intel Rallies on Factory Buyback

Intel’s ~18% move last week followed its decision to spend about $14B to buy back a previously sold stake in its Ireland manufacturing facility. That stake had been sold in 2024 to raise cash during a weaker period, so reversing the transaction signals a stronger balance sheet and improved financial flexibility.

The deal is also expected to be accretive to earnings and gives Intel full control over the facility rather than sharing economics with a partner. That increases its direct exposure to any improvement in demand tied to servers and data center chips, including those connected to AI spending.

Importantly, this doesn’t represent a new shift into AI, but rather a continuation of Intel’s existing effort to rebuild its manufacturing and compete more directly in that market.

The move stood out because it was concrete. At a time when parts of the AI trade have been more sensitive to expectations around timing and returns, Intel’s update pointed to balance sheet improvement, earnings impact, and operational control—factors that tend to drive more immediate re-pricing.

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai