.png)

L2 Weekly Stock Market News Analysis

April 19th, 2026

TLDR:

Markets head into the week after a sharp risk-on move driven by headlines rather than sustained conviction.

Friday’s rally was triggered by claims that the Strait of Hormuz had reopened, sending oil sharply lower. That drop in oil pulled yields down as well, as lower energy prices reduce inflation expectations and ease pressure on the Fed to keep rates elevated.

That move in yields drove the rotation.

As yields fell, capital moved into tech, consumer discretionary, and other rate-sensitive sectors, where lower discount rates support valuations and financing conditions. Within hours, that narrative began to unwind. By the weekend, Iran rejected those claims, tanker traffic stalled, and ships were left anchored or reversing course mid-transit.

The market has effectively priced in lower energy risk—and is now exposed if that assumption proves wrong.

The key shift is in how oil is being priced.

This is no longer just about supply, but flow. Even without a full shutdown, disrupted routing and stalled traffic mean supply isn’t moving normally. With a large volume of crude sitting idle, pricing is reflecting uncertainty around transit rather than production levels.

That dynamic feeds directly into positioning.

Last week’s leadership was concentrated in sectors that benefit from falling yields. If oil moves higher again, inflation expectations rise, yields follow, and pressure shifts back onto those same areas that just led the rally.

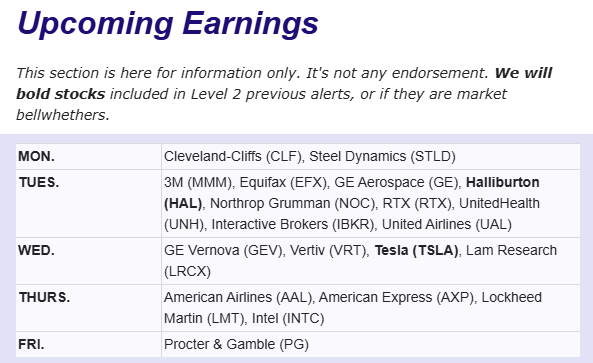

This week also brings a heavy earnings slate, with key reports from Tesla, Intel, UnitedHealth, American Express, and Procter & Gamble. These results will give a clearer read on how companies are handling shifting costs and consumer behavior.

Developments around U.S.–Iran negotiations remain the primary driver of oil—and by extension, markets.

Risk-On Rally — Friday Morning

At 8:45 AM ET Friday, Iran’s Foreign Minister said the Strait of Hormuz was “completely open” to commercial shipping. Minutes later, Trump confirmed it. Over the next few hours, additional claims followed — that the U.S. and Iran were coordinating on clearing the strait, that it would remain open, and that Iran could suspend its nuclear program.

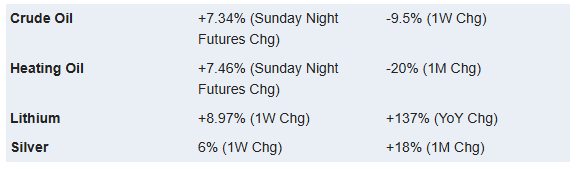

Oil reacted immediately. Prices dropped nearly $10 per barrel and briefly moved into the low $80s as supply disruption risk was taken out of the market . Around the same time, roughly $800 million in oil shorts were placed just before the announcement, generating an estimated ~$70 million in profit within the hour as prices fell.

Equities moved higher, yields declined, and rate expectations shifted alongside the drop in oil.

Image Below: the latest Bloomberg ship tracking data showing that tanker traffic through the Strait of Hormuz has largely ground to a halt.

Breakdown — Strait Disruption and Escalation

By Friday evening, Iran rejected multiple U.S. claims, calling them false and denying any agreement on nuclear concessions.

Conditions in the strait changed quickly after that.

Ships attempting to pass received conflicting instructions. Some moved toward the strait, others were told to turn back. Within hours, vessels began reversing course mid-transit, and by Saturday, Iranian forces were actively enforcing control — including reported gunfire and direct warnings to ships.

By the weekend, traffic had effectively stalled.

Very few vessels were able to transit, and ship tracking data showed tankers anchored or waiting, with an estimated ~135 million barrels of crude and refined products sitting idle in the Persian Gulf . In practical terms, the strait was not functioning as a reliable route for global energy flows.

At the same time:

- The U.S. said talks would resume this week in Pakistan and framed them as a final opportunity

- Iran backed out of those talks under current conditions

- Iran accused the U.S. of preparing a “surprise attack”

- The U.S. intercepted, disabled, and took control of an Iranian-flagged cargo ship attempting to move through the strait

The ceasefire is still in place, but both sides are now signaling escalation if no agreement is reached this week, including explicit threats of broader strikes.

Positioning Risk — Leaders This Week

This week’s gains were concentrated in:

- XLK (Tech): +8.2%

- XLY (Consumer Discretionary): +6.7%

- XLC (Communication): +4.5%

- XLRE (Real Estate): +3.9%

Energy lagged (XLE -3.4%) as oil fell.

That matters going into tomorrow.

If oil moves higher again, it feeds directly into inflation expectations, which pushes Treasury yields higher. That’s where pressure shows up first in long-duration assets.

Tech / Real Estate → via yields (MSFT, NVDA, PLD, AMT)

These names are valued on future cash flows. When yields rise:

- Discount rates increase → future earnings are worth less today

- Valuations compress even if fundamentals don’t change

- Rate-sensitive sectors like real estate (REITs) also face higher financing costs

That’s why tech and real estate rallied on the way down in yields — and why they’re exposed if that reverses.

Consumer Discretionary → via reduced spending (AMZN, SBUX, HD, LOW)

Higher gas and energy costs act like a direct hit to disposable income:

- More spending on essentials → less left for discretionary purchases

- Big-ticket items (autos, home improvement, e-commerce) are the first to slow

- Companies see weaker demand and more cautious consumer behavior

More directly, it pressures consumer credit.

Higher gas and energy costs take up a larger share of monthly income, especially for lower- and middle-income consumers. That forces trade-offs:

- Less discretionary spending

- More reliance on financing (BNPL, personal loans)

- Less flexibility to stay current on payments

That’s where delinquency risk builds:

- Borrowers already using BNPL or loans are more likely to fall behind

- New borrowers tend to be lower quality

- Lenders tighten standards, slowing growth

For companies like AFRM (+35% in the last week), UPST (+30% in the last week), SOFI, RKT, that shows up as:

- Slower volume

- Higher charge-offs over time

- Pressure on forward expectations

These names are tied to the marginal consumer, which is where stress shows up first when costs rise.

Last's Weeks Sector Winners & Losers

Sector performance last week reflected a sharp risk-on move driven by the drop in oil and improving sentiment around a potential resolution in the Middle East.

Leadership was concentrated in growth and rate-sensitive sectors, with Technology (XLK) up +8.22%, Consumer Discretionary (XLY) +6.66%, and Communication Services (XLC) +4.52%. Real Estate (XLRE) also moved higher, gaining +3.88%, alongside Financials (XLF) at +3.27%.

More cyclical areas were positive but lagged, with Industrials (XLI) up +1.16% and Materials (XLB) roughly flat at -0.15%.

Defensives underperformed, with Consumer Staples (XLP) essentially flat (+0.11%) and Utilities (XLU) declining -1.70%, while Health Care (XLV) saw only modest gains of +1.01%.

Energy (XLE) was the weakest sector, falling -3.37% as oil prices dropped sharply following the announcement that the Strait of Hormuz had reopened.

The move shows a clear shift toward growth, consumer exposure, and rate-sensitive areas as markets reacted to lower energy prices and easing inflation expectations, while energy and defensive positioning were unwound.

Upcoming Events This Week

The Middle East remains the dominant driver, with markets now focused on whether the situation stabilizes or escalates further following the breakdown in messaging around Hormuz. Developments around the second round of U.S.–Iran negotiations, set to begin Monday, will be the primary catalyst, especially with the ceasefire deadline approaching Tuesday. Any headlines around a deal—or lack of one—will continue to move oil and set direction for broader markets.

Earnings remain a major focus this week, with roughly 15% of S&P 500 companies reporting, including key names such as Tesla, Intel, UnitedHealth, American Express, and Procter & Gamble. These results will provide insight into how companies are navigating higher input costs, consumer behavior, and broader macro uncertainty.

On the data front, March retail sales (Tuesday) will be the most important release, expected to show strong growth and extend the trend in consumer spending. Pending home sales will also be released the same day, offering a read on housing activity as rates remain elevated. Later in the week, Michigan inflation expectations (Friday) will be closely watched for any shift in consumer inflation outlook.

Flash S&P PMIs will provide an updated look at how the manufacturing and services sectors are responding to the energy shock and geopolitical backdrop.

On the policy side, Fed Chair nominee Kevin Warsh will testify before Congress, marking his first major public appearance and offering insight into his stance on rates and balance sheet policy.

Globally, central banks and data will also be in focus:

- PBoC sets loan prime rates in China

- Japan releases trade and inflation data

- Europe and the UK report PMIs, inflation, and retail sales

The key dynamic this week is straightforward:

markets are balancing incoming economic data and earnings against a geopolitical backdrop that can shift quickly, with energy prices acting as the transmission channel into inflation, rates, and risk assets.

Company News

LevelFields AI Stock Alerts Last Week

FRMM (Forum Markets) +81% — Buyback + Strategic Review Drives Massive Spike

FRMM surged 81% in a single session after the company announced the reinitiation of its share repurchase program, with authorization to buy back stock even beyond typical safe harbor limits.

The board also formed a special committee to evaluate strategic alternatives, including potential mergers, asset sales, partnerships, or a full return of capital to shareholders.

The move signals two things clearly:

- Management believes the stock is deeply undervalued

- The company is actively exploring ways to unlock that value

The combination of aggressive buybacks and a formal strategic review created a squeeze-type reaction, driving one of the largest single-day moves in the market this week.

Other Company News

Strong Earnings, Weak Guidance — Why the Market Rally Is More Fragile Than It Looks

Markets have pushed back toward highs on the combination of easing geopolitical tensions and stronger-than-expected first-quarter earnings, but the underlying trend that matters most right now isn’t the results—it’s the outlook.

And that outlook is starting to crack.

On the surface, earnings season has been solid. S&P 500 companies are beating expectations by roughly 11% on aggregate, with overall earnings growth tracking near 12% for the quarter. That kind of performance would normally support a sustained rally.

But the market isn’t reacting to what just happened—it’s reacting to what comes next.

Guidance is deteriorating across the board.

More analysts are cutting profit estimates than raising them, and the number of companies increasing both earnings and revenue outlooks is declining at the same time—a pattern historically seen ahead of major market drawdowns, including 2008 and 2021.

That shift reflects a growing list of pressures building beneath the surface:

Weaker consumer demand expectations

Rising input costs tied to inflation and energy shocks

Tariff uncertainty and shifting trade policy

Limited visibility due to geopolitical instability

Companies aren’t collapsing—but they’re becoming more cautious.

That caution is already showing up in behavior.

Roughly 40 S&P 500 companies have lowered their guidance so far this season—the highest since mid-2025—and some firms are going a step further by withdrawing guidance entirely.

And the market response has been clear.

Companies that beat earnings but cut outlooks are getting sold.

Companies that withdraw guidance are getting hit even harder.

Recent examples reinforce the pattern:

Abbott fell after lowering profit guidance

JPMorgan slipped after trimming net interest income outlook

Netflix dropped on weak forward estimates

In each case, strong results didn’t matter—the forward view did.

That’s the key shift.

The market is no longer rewarding backward-looking strength. It’s punishing forward-looking uncertainty.

And that creates a fragile setup for equities here.

There are two ways this plays out:

If companies stabilize guidance—even at lower levels—and provide clearer forward visibility, the market can continue grinding higher as uncertainty fades and expectations reset.

But if guidance continues to weaken, or more companies begin withdrawing outlooks altogether, the risk is a broader repricing—potentially pushing equities back down 5–10% as the gap between strong past earnings and weaker future expectations closes.

There’s also a structural issue at play.

This rally is being supported by macro relief—peace expectations, liquidity, and strong headline earnings—not by improving forward fundamentals.

That’s a dangerous mix.

When markets rally into uncertainty rather than through it, they become increasingly dependent on confirmation.

And right now, that confirmation isn’t showing up in guidance.

Bottom line:

Earnings are strong enough to support the current market—but guidance is not. Until forward outlooks stabilize, this rally remains vulnerable to sharp resets driven not by what companies report, but by what they expect.

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai