.png)

L2 Weekly Stock Market News Analysis

April 26th, 2026

TLDR:

Markets are still being driven by energy, geopolitics, and policy.

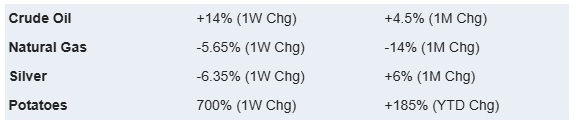

Iran talks have stalled, and even if a deal happens, supply won’t normalize quickly. Repositioning tankers and restoring routes takes time, keeping supply tighter than markets are pricing.

That is now showing up in earnings. Halliburton confirmed the setup: profits more than doubled on flat revenue as oil rose ~20–25% QoQ. Next up, ExxonMobil, Chevron, and EOG will show how much of that pricing strength is flowing through.

The impact is spreading beyond producers—fuel margins, fertilizer, agriculture, shipping, and industrial demand all benefit as higher energy moves through the system.

Reconstruction adds another layer. Roughly $50–60B in Gulf damage across energy, logistics, and industrial infrastructure creates demand for equipment, materials, and engineering capacity.

Policy is also driving price action. Intel’s earnings this week ($0.29 EPS vs ~$0.01 expected, $13.6B revenue) and ~24% move higher show how positioning around U.S. priorities—AI, semiconductors, and domestic production—is translating into earnings follow-through.

Market positioning was selective last week. Staples (+2.5%), Tech (+2.5%), and Industrials (+2.2%) led, while Utilities, Financials, and Communication Services lagged.

Looking ahead, the key catalysts are Iran headlines, mega-cap tech earnings, energy majors, Fed policy, GDP, PCE, and ISM.

Iran Talks Stall — Watch the Lag, Not the Headlines

Talks stalled again over the weekend, and the Strait of Hormuz remains effectively blocked.

What matters now isn’t whether a deal happens—it’s how long normalization takes after one does. Even in a best-case scenario, reopening flows takes time: clearing routes, repositioning tankers, and restoring logistics.

That keeps supply tight longer than the market is pricing.

This week added another layer: earnings.

Oilfield services and energy names are now reporting into a higher price environment.

- HAL (Halliburton) already showed the setup: EPS more than doubled to $0.55 on flat revenue, driven by margin expansion and stronger pricing.

- Oil prices were up ~20–25% quarter-over-quarter (WTI ~$72 vs ~$60; Brent ~$80 vs ~$64), supporting activity levels and pricing power across the system.

There was still some offset—Middle East disruptions reduced EPS by ~$0.02–$0.03—but profitability improved anyway, which is the key signal.

More importantly, the largest integrated and upstream players report next:

- XOM (ExxonMobil) — Friday, May 1, 8:30 AM

- CVX (Chevron) — Friday, May 1, 11:00 AM

- EOG (EOG Resources) — Wednesday, May 6

These reports will show how higher crude prices are flowing through upstream earnings.

Why higher oil prices matter for earnings:

- Higher oil prices increase the price producers receive per barrel

- Costs don’t rise as quickly, so margins expand

- Higher cash flow supports continued drilling and production activity

- That keeps demand strong for services companies

Other Earnings to Watch

Retail / Fuel Margins

CASY (Casey’s) — Earnings: June 8, 2026

Convenience store and fuel retailer; higher fuel price volatility can expand per-gallon margins while driving in-store traffic

MUSA (Murphy USA) — Earnings: April 29, 2026

Operates high-volume gas stations (often near Walmart); benefits from widening fuel margins during price swings

Fertilizer / Chemicals

CF (CF Industries) — Earnings: May 6, 2026 (AMC)

Nitrogen fertilizer producer; higher energy prices and supply disruptions tighten global fertilizer supply, supporting pricing

Agriculture / Commodities

ADM (Archer-Daniels-Midland) — Earnings: April 28, 2026

Processes and trades agricultural commodities; higher oil boosts biofuel demand and crop pricing

Shipping / Logistics

MATX (Matson) — Earnings: May 5, 2026

Ocean shipping company focused on Pacific routes; rerouted trade flows and tighter capacity support higher rates

TNK (Teekay Tankers) — Earnings: May 14, 2026

Oil tanker operator; longer routes increase demand for ships and daily charter rates

Rail / Transport

CNI (Canadian National Railway) — Earnings: April 27, 2026

North American rail operator; higher oil supports crude-by-rail volumes and makes rail more competitive vs trucking

Industrial / Energy Inputs

APD (Air Products) — Earnings: May 7, 2026

Supplies industrial gases to refiners and energy companies; higher refining activity increases demand

Gulf Rebuild — $50B+ in Damage Driving Equipment and Infrastructure Demand

The focus is still on the conflict, but the rebuild is already taking shape.

Estimates point to roughly $50–60 billion in total damage, with losses concentrated in energy infrastructure, logistics systems, and industrial assets.

Where the damage is concentrated:

Energy infrastructure (~$25–30B | ~45–50%)

Oil fields, refineries, pipelines, and storage facilities account for the largest share of losses.

Disruptions to production and transport have already tightened global supply, making restoration the first priority.

Transport and logistics (~$10–15B | ~20–25%)

Ports, shipping terminals, and trade routes have been impacted, slowing the movement of materials needed for reconstruction itself.

That creates a second constraint—rebuilding requires logistics capacity that is also damaged.

Industrial and urban systems (~$15–20B | ~25–30%)

Facilities tied to manufacturing, utilities, and basic services are also affected, increasing demand for construction materials and heavy equipment.

Companies That Can Benefit from These Shortages:

Water / Desalination

ERII — desalination systems; direct exposure to Gulf water infrastructure, which depends heavily on seawater desalination

XYL — water treatment and infrastructure

Water systems depend on both energy and power. Any disruption forces immediate repair, making desalination one of the first areas to receive capital.

EPC / Engineering

Saipem — SPM.MI

Technip Energies — TE.PA

Fluor Corporation — $FLR

KBR — $KBR

Jacobs — $J

These companies are tied to rebuilding refineries, pipelines, ports, and industrial systems—projects that move quickly once funding is allocated.

Oilfield Services

Schlumberger — $SLB

Halliburton — $HAL

Baker Hughes — $BKR

Energy infrastructure repair directly feeds into demand for services tied to drilling, completion, and production restoration.

Heavy Equipment

Caterpillar — $CAT

Komatsu — 6301.T

Volvo Construction Equipment — VOLV-B.ST

Rebuilding at scale drives demand for excavators, cranes, and industrial machinery, especially as multiple projects compete for equipment.

Steel / Materials

ArcelorMittal — $MT

Nucor — $NUE

Tata Steel — TATASTEEL.NS

Large-scale reconstruction increases demand for steel and raw materials, adding pressure to already tight supply chains.

Power / Grid / Electrical Systems

Quanta Services — $PWR

EMCOR — $EME

Eaton — $ETN

Power restoration is required before most industrial activity can resume, putting grid and electrical systems early in the rebuild cycle.

Logistics

A.P. Moller-Maersk — MAERSK-B.CO

DHL Group — DHL.DE

JB Hunt — $JBHT

C.H. Robinson — $CHRW

Reconstruction requires moving large volumes of equipment and materials, tightening freight capacity and increasing demand for global logistics providers.

Policy Is Driving Price Action

The biggest moves in this market are not coming from fundamentals—they’re coming from Trump.

Data shows the largest up days in the S&P 500 this cycle are tied to policy and Trump commentary, and you’re seeing it play out in real time across individual stocks.

Look at Intel (INTC). This wasn’t just a random earnings move this week—the stock is one of the best performers over the past 12 months, and that run has been tied to its positioning inside U.S. policy priorities: domestic chip production, AI infrastructure, and supply chain security.

This week simply confirmed it. Intel printed a major beat ($0.29 EPS vs ~$0.01 expected, $13.6B revenue, strong data center growth) and the stock jumped ~24% in a day.

That’s the pattern: policy tailwind first → positioning → earnings catch up.

Same thing with Palantir (PLTR). The company has been consistently gaining share in federal contracts under the Trump administration while traditional players have lost ground, reinforcing its position at the center of government and defense systems.

That’s showing up in the scale of wins:

- Up to $10B Army data platform contract consolidating dozens of legacy systems

- $448M Navy “ShipOS” program tied to shipbuilding and supply chain optimization

- $300M USDA AI contract focused on food supply visibility

- $130M+ IRS analytics work tied to large-scale data and enforcement

- In the mix for FAA modernization (part of a $30B+ initiative)

- Involved in next-gen defense systems like missile defense software (“Golden Dome”)

This isn’t just incremental growth—it’s consolidation. Palantir is moving from one of many vendors to core infrastructure across multiple agencies.

What’s notable is that Trump has been posting about the company with the ticker “PLTR” included, explicitly pointing to the stock—a direct signal layered on top of already accelerating contract momentum.

And this isn’t new or limited to one sector. The administration has already been taking stakes across rare earths, critical minerals, semiconductors, and energy supply chains, turning policy into direct capital allocation.

This week’s Spirit Airlines (SAVE / now OTC: FLYYQ) move fits the same pattern. The stock surged ~40% intraday on policy-driven speculation around potential government involvement in preserving domestic airline capacity.

That move isn’t about fundamentals—Spirit is already in distress. It’s the market reacting purely to the possibility of policy intervention.

Last's Weeks Sector Winners & Losers

Sector performance last week showed a more muted, balanced move, rather than a broad rotation.

Leadership came from defensive and large-cap growth areas, with Consumer Staples (XLP +2.52%), Technology (XLK +2.51%), and Industrials (XLI +2.20%) leading gains. Energy (XLE +0.71%) also held up despite volatility in oil.

The rest of the market saw limited movement, with Real Estate (XLRE +0.34%), Materials (XLB +0.12%), and Consumer Discretionary (XLY +0.09%) posting modest gains.

On the downside, defensives and rate-sensitive sectors lagged, with Utilities (XLU -0.56%), Financials (XLF -0.44%), Health Care (XLV -0.25%), and Communication Services (XLC -1.21%) finishing lower.

Overall, the move suggests selective positioning rather than a full risk-on shift—with strength concentrated in staples and tech, while broader cyclicals and rate-sensitive areas showed less conviction.

Upcoming Events This Week

The global backdrop is still being driven by the Iran conflict as it enters its eighth week. Any signs of a deal—or concessions to restore trade—will continue to dictate energy markets and, by extension, broader risk assets.

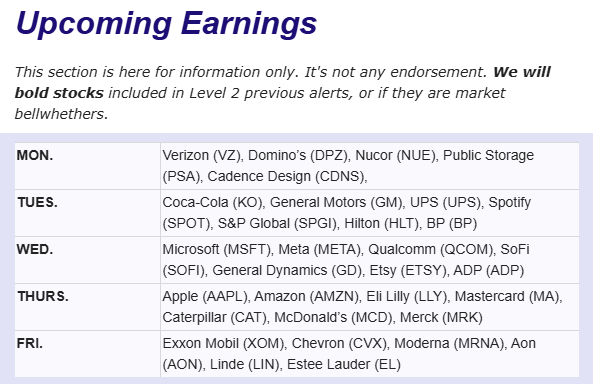

At the same time, this is one of the busiest weeks of earnings season, led by mega-cap tech. Microsoft, Amazon, Alphabet, and Meta report Wednesday, followed by Apple Thursday. These updates will be critical in shaping expectations around AI spending, which has been the primary driver of global equity performance.

Energy and cyclicals will also be in focus, with Chevron and Exxon Mobil reporting, alongside major names across pharma, industrials, and consumer goods. This will give a broader read on how higher energy prices are flowing through margins and demand.

On the policy side, the Federal Reserve is expected to hold rates at 3.50–3.75%, with this likely being Powell’s final meeting as Chair. The tone is expected to remain cautious as the Fed evaluates inflation risks tied to rising oil prices.

Globally, policy decisions from the ECB, Bank of England, and Bank of Japan will add to the macro backdrop.

On the data front, Q1 GDP (U.S. and Euro Area) will be key, with U.S. growth expected around 2.1%, alongside the PCE inflation report, which will show whether price pressures are easing or being re-accelerated by energy.

Additional data includes ISM Manufacturing, durable goods, housing data, and employment cost index, all providing a read on how the economy is holding up under rising input costs.

Company News

LevelFields AI Stock Alerts Last Week

Skillz (SKLZ) +237% — Quick Sprints Scenario

SKLZ surged over 200% following a Quick Sprints alert, driven by a major catalyst after the company secured a $420M legal win against a competitor.

The ruling removed a key overhang and triggered a rapid repricing of the stock, showing how quickly these setups can move once a catalyst hits.

Pineapple Financial (PAPL) +46% — Buyback Expansion

Pineapple Financial jumped ~46% in one day after announcing a major expansion of its share repurchase program, increasing authorization from $3M to $15M.

For a company of this size, the buyback is highly material relative to its market cap, signaling strong confidence from management and creating immediate demand for shares.

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai