L2 Weekly Stock Market News Analysis

October 26th, 2025

TLDR:

Inflation cooled:September CPI rose 0.3% MoM and 3.0% YoY, slightly below forecasts. Core inflation also held at 3.0%, keeping the Fed on track for another 25 bps rate cut next week despite the government shutdown — which now threatens to delay October’s inflation report entirely.

Intel earnings mixed: Intel returned to profit ($13.7B revenue, $0.23 EPS) but shares faded as investors focused on debt, execution risks, and questions about its foundry turnaround. The U.S. government’s near-10% equity stake remains a centerpiece of the broader industrial-policy strategy.

Russia sanctions roiled energy: The U.S. imposed new sanctions on Rosneft and Lukoil, restricting financing and trade. Oil prices spiked briefly before easing, while uranium and nuclear-fuel stocks gained on expectations of tighter global supply chains.

Quantum stocks popped: Speculation about U.S. strategic investments in quantum computing and post-quantum security drove small-cap names higher, adding to tech volatility in a week dominated by macro uncertainty and the still-frozen federal government.

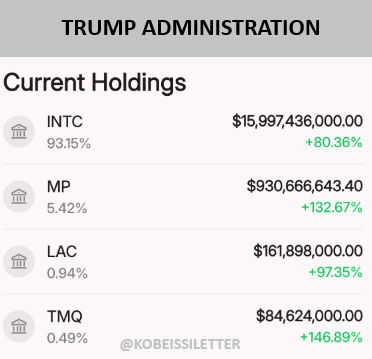

The White House Strategic Reserve Is Beating Wall Street

This week, reports surfaced that Washington may be taking equity stakes in quantum-computing firms, marking another expansion of what’s become the best-performing institutional portfolio in the world.

Every disclosed government holding is now up at least +80%, with two nearing +150%. We’ve tracked this policy shift since early August, and Level 2 members have already captured a series of wins from it.

Level 2 Trade Receipts (Strategic-Reserve Theme):

- LAC (equity) 7.53 → 9.50 | +26.2 % (15 days)

- TMQ (equity) 8.93 → 10.60 | +18.7 % (in < 1 day)

- INTC Jan ’26 $25 Calls 3.45 → 7.60 | +120.3 % (34 days)

- INTC (equity) 24.72 → 32.50 | +31.5 % (34 days)

The Strategic Reserve is the working arm of the administration’s February 2025 plan to build a U.S. sovereign wealth fund—not a single mega-pool, but a decentralized, deal-by-deal approach. The goal is to turn industrial policy into a return-generating portfolio that also secures control of key supply chains.

1) Grow federal assets and share the AI upside

A large share of recent GDP growth has come from data-center construction, AI infrastructure, and critical-mineral expansion. Data centers now make up nearly 1% of GDP and over 7% of total fixed investment. Meanwhile, automation will replace some jobs, concentrating gains in capital-intensive sectors.

By taking small equity stakes or long-term offtake rights in projects where public funding already reduces risk — from AI data centers to rare earths, lithium, and copper supply chains — the government can build federal assets and capture part of the upside, rather than simply footing the bill for the transition.

2) Strengthen bargaining power with allies and suppliers

This week’s U.S.–Australia critical-minerals deal shows how Washington is using joint investments to build leverage. The agreement backs Alcoa’s gallium project in Western Australia — expected to produce about 100 tons per year, roughly 10% of global supply — and adds access to germanium, another metal China has restricted.

Both are vital for chips, sensors, quantum tech, and defense systems. By co-financing projects and securing long-term offtake, the U.S. strengthens its bargaining power with allies and manufacturers while expanding non-Chinese supply-chain capacity in mining, refining, and advanced manufacturing.

3) Keep control of critical supply chains

The U.S. is building ownership and long-term supply links across semiconductors, rare earths, lithium, copper, and nuclear fuel to reduce reliance on China, which dominates rare-earth refining and has curbed exports of gallium, germanium, and graphite.

Projects like Trilogy Metals (TMQ), Lithium Americas (LAC), U.S. Antimony (UAMY), and MP Materials (MP) anchor this shift—securing inputs vital for defense, energy, and chip production. If trade tensions escalate, these holdings ensure the U.S. retains direct access to critical materials, protecting both industry and national security.

Where They Could Go Next

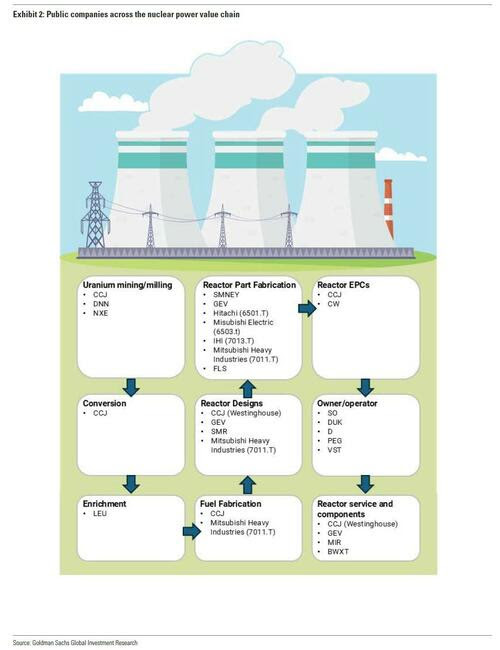

Nuclear power and fuel: the backstop for AI electricity

Nuclear stocks rebounded this week as new U.S. sanctions on Russia’s energy sector renewed focus on Moscow’s dominance in uranium enrichment and reactor exports. Russia still controls roughly 44–50% of global enrichment capacity and around 65% of new reactor exports, underscoring how dependent the world remains on a single source for nuclear fuel and technology.

That imbalance is risky at a time when AI data centers are straining the U.S. power grid. Electricity demand is rising at the fastest rate in decades, and grid operators have warned of regional shortages as data-center and semiconductor loads accelerate. In response, policymakers and utilities are increasingly turning back to nuclear power as the most reliable, zero-carbon source of steady energy. Oracle’s plan for a 1-gigawatt small modular reactor (SMR) campus reflects this shift — showing how nuclear is being positioned not just as clean baseload power, but as the foundation for meeting AI-driven electricity needs over the next decade.

A strategic U.S. stake in nuclear or uranium companies would serve two key objectives:

- Supply security: ensuring energy resilience if a foreign adversary controls key materials.

- Long-term growth capture: owning part of a core industry that will power the AI era and digital economy.

Level 2 members captured this nuclear theme early, securing strong gains across the value chain:

- Cameco (CCJ) +19.8% in 34 days

- Cameco (CCJ) Mar 2026 $75 calls +56.9% in 29 days

- Energy Fuels (UUUU) +30.4% in 5 days

- Centrus Energy (LEU) +55.0% in 25 days

- BWX Technologies (BWXT) +11.9% in 17 days and +59.1% on 2026 calls in 14 days

These companies anchor the U.S. nuclear value chain — CCJ and UUUU in uranium mining, LEU in enrichment and fuel fabrication, and BWXT in reactor components and defense systems. Others such as Constellation Energy (CEG), GE Vernova (GEV), Curtiss-Wright (CW), Denison Mines (DNN), and NexGen Energy (NXE) extend the ecosystem through generation, equipment, and mining exposure.

Shipbuilding and maritime capacity: preparing for a new fleet mix

The White House’s proposed “Golden Fleet” marks a major shift in U.S. naval strategy — targeting a force of about 280–300 crewed ships supported by unmanned vessels to strengthen coverage in the Western Hemisphere and improve defense against drones and hypersonic weapons.

At the center of this plan is Huntington Ingalls Industries (HII), the largest military shipbuilding company in the United States. HII operates the shipyards that built many of America’s largest battleships and remains the only U.S. builder of nuclear-powered aircraft carriers. Its role is vital as the Navy begins to modernize its fleet for a new era of deterrence and maritime competition.

Treasury Secretary Scott Bessent has already hinted at the idea of a government stake in the shipbuilding industry, noting in August that sectors like shipbuilding could be included in the administration’s broader investment strategy.

Other likely beneficiaries include BWX Technologies (BWXT), which supplies naval reactors, and General Dynamics (GD), which builds submarines.

U.S.–China Trade Framework: Tariff Threats Ease, Rare Earth Leverage Holds

The U.S. and China reached a “framework deal” over the weekend, defusing Trump’s planned 100% tariffs on Chinese goods and setting the stage for a broader agreement at next week’s Trump–Xi summit.

Treasury Secretary Scott Bessent said China agreed to make large soybean purchases and delay new rare-earth export restrictions for up to a year — a key win for U.S. supply stability. The U.S. will keep its own export controls but extend the current tariff truce.

The deferral gives Washington and its allies time to expand domestic and partner supply chains for critical materials while easing near-term market stress.

Soybeans and ag equities (e.g., ADM, BG, CF) could see near-term demand upside from renewed Chinese buying.

All eyes now turn to the Trump–Xi meeting, where a formal rare-earth or trade announcement could determine whether this truce becomes a lasting reset or a temporary pause.

Upcoming Events This Week

Next week will bring a wave of major monetary policy decisions and high-stakes earnings releases. The Federal Reserve’s FOMC meets without its usual economic data due to the ongoing U.S. government shutdown, now entering its fourth week. Markets are fully pricing in a 25-basis-point rate cut, which would bring the federal funds rate to a 3.75%–4.00% range.

Abroad, the European Central Bank, Bank of Japan, and Bank of Canada will also issue rate decisions. The Bank of Canada is expected to cut by 25 bps, while GDP figures from the Eurozone, Mexico, and South Korea, and monthly data from Canada, will help gauge global momentum. China’s PMI data and an inflation print from Australia and the Eurozone round out a packed macro calendar.

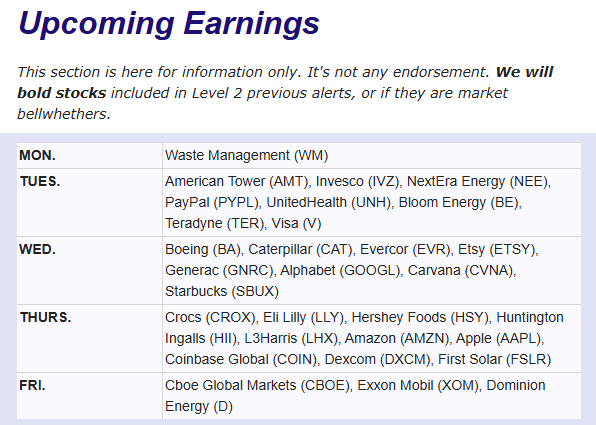

Earnings will dominate headlines as Big Tech steps to the plate — reports are due from Microsoft, Apple, Alphabet, Meta, Amazon, Visa, Mastercard, UnitedHealth, NextEra, Eli Lilly, AbbVie, ExxonMobil, and Chevron.

.png)

Company News

LevelFields AI Stock Alerts Last Week

Spruce Biosciences (SPRB) +1,400% on FDA Breakthrough News

Spruce Biosciences (SPRB) surged over 1,400% in one day after the U.S. FDA granted Breakthrough Therapy Designation for its experimental enzyme replacement therapy, Tralesinidase Alfa (TA-ERT), which targets Sanfilippo Syndrome Type B (MPS IIIB) — a rare and deadly genetic disorder.The designation fast-tracks development and review, signaling strong confidence in the drug’s potential and marking one of the biggest single-day gains for a biotech stock this year.

Viomi Technology (VIOT) +20% on Earnings and Buyback News

Viomi Technology Co., Ltd (VIOT) jumped 20% in one day after announcing that it will release its first-half 2025 financial results on November 10, 2025, alongside a new US$20 million share repurchase plan.

Intel: Earnings, the White House stake, and the road to a real comeback

Q3 recap. Intel is finally back in the black. The company reported $13.7 B in revenue (+3% YoY) and $0.23 in adjusted EPS, marking its first profit since 2023. But shares gave back early gains as investors focused on the tough road ahead.

Debt and balance sheet. Intel repaid $4.3 B of debt last quarter and now holds about $30.9 B in cash and short-term investments. It also secured roughly $15 B in new capital — including a ~9.9% U.S. government stake (bought at $20.47 per share), $5 B from Nvidia, and $2 B from SoftBank. That funding, plus $5.7 B in U.S. government support already received, gives Intel breathing room to rebuild without taking on new debt.

What’s working — and what still isn’t.

- PC rebound: Laptop and desktop sales rose 5%, helping the quarter’s beat.

- Data Center & AI: Still down 1% YoY — Intel is struggling to catch up to Nvidia in AI chips.

- Foundry division: This is Intel’s manufacturing business — it makes chips for itself and (other companies in the future). Revenue was $4.2 B, but it still lost $2.3 B last quarter. That’s an improvement from a $5.8 B loss a year ago, but the division needs outside customers before it can turn profitable.

Why the foundry matters.

Intel wants to become America’s version of TSMC — the company that manufactures most of the world’s chips. If Intel can prove its “Intel 18A” production process works and win contracts from other chip designers, it can secure a long-term place in the global semiconductor supply chain and reduce U.S. dependence on Asia.

Capital spending & capacity.

Intel plans to spend about $18 B on new plants and equipment this year and will likely cut spending next year. Its massive Ohio fab project was pushed to the 2030s as Intel prioritizes stabilizing current operations.

.png)

The Greatest Trades of All Time!

How Warren Buffet Used Events to Make Fortunes

How Are Robots Being Used Today for Business?

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai