AI investment, Fed uncertainty, and energy shocks drive selective market gains as earnings expectations rise.

Sectors & Industries

May 4, 2026

Table of Contents

The latest Fed meeting exposed a meaningful shift beneath the surface.

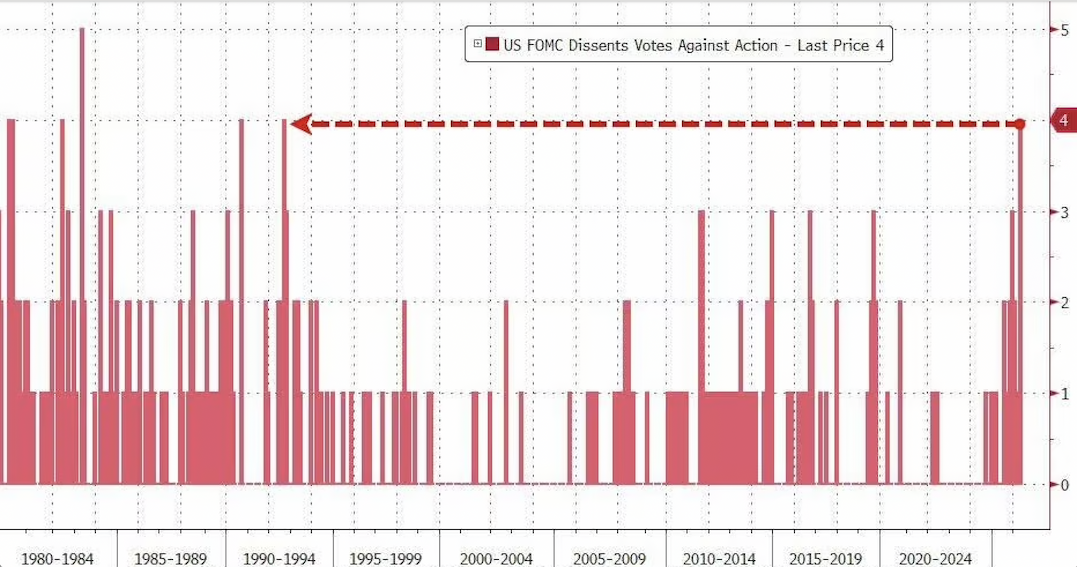

Rates were held at 3.50–3.75%, but the decision came with an 8–4 vote split—the most divided outcome in decades and a clear sign that policymakers are no longer aligned on the path forward.

The breakdown:

This reflects a clear divide:

That inflation concern is no longer abstract:

At the same time, Powell indicated the center of the committee is shifting toward a neutral stance—meaning policy could move either direction depending on data, rather than being biased toward cuts.

He also made clear why the Fed is so divided: policymakers are trying to interpret an economy shaped by repeated supply shocks—pandemic disruptions, tariffs, and now the Iran-driven energy shock—which are pushing inflation higher while making growth harder to read.

Leadership is also in transition.

Powell confirmed he will remain on the Board after stepping down as Chair, while Kevin Warsh moves toward taking over—an unusual overlap that adds another layer of uncertainty.

Warsh is generally viewed as more open to rate cuts, but he is stepping into a committee already pushing back against easing, with three dissents against maintaining an easing bias and a broader shift toward neutrality across the Fed. Convincing the committee to ease further is likely to be an uphill battle.

The implication for markets:

Earnings season has come in significantly stronger than expected.

That strength is why markets are holding near highs.

But the composition of that growth is shifting—and the market is reacting to it.

The biggest development this quarter is the scale of AI investment:

This is no longer incremental spending—it’s a full-scale infrastructure buildout.

At the same time, the payoff is still uneven:

This is where the market is drawing a line:

You’re already seeing that divergence in price action:

And beneath that:

The key shift:

The market is no longer rewarding AI exposure—it’s rewarding AI efficiency and visibility.

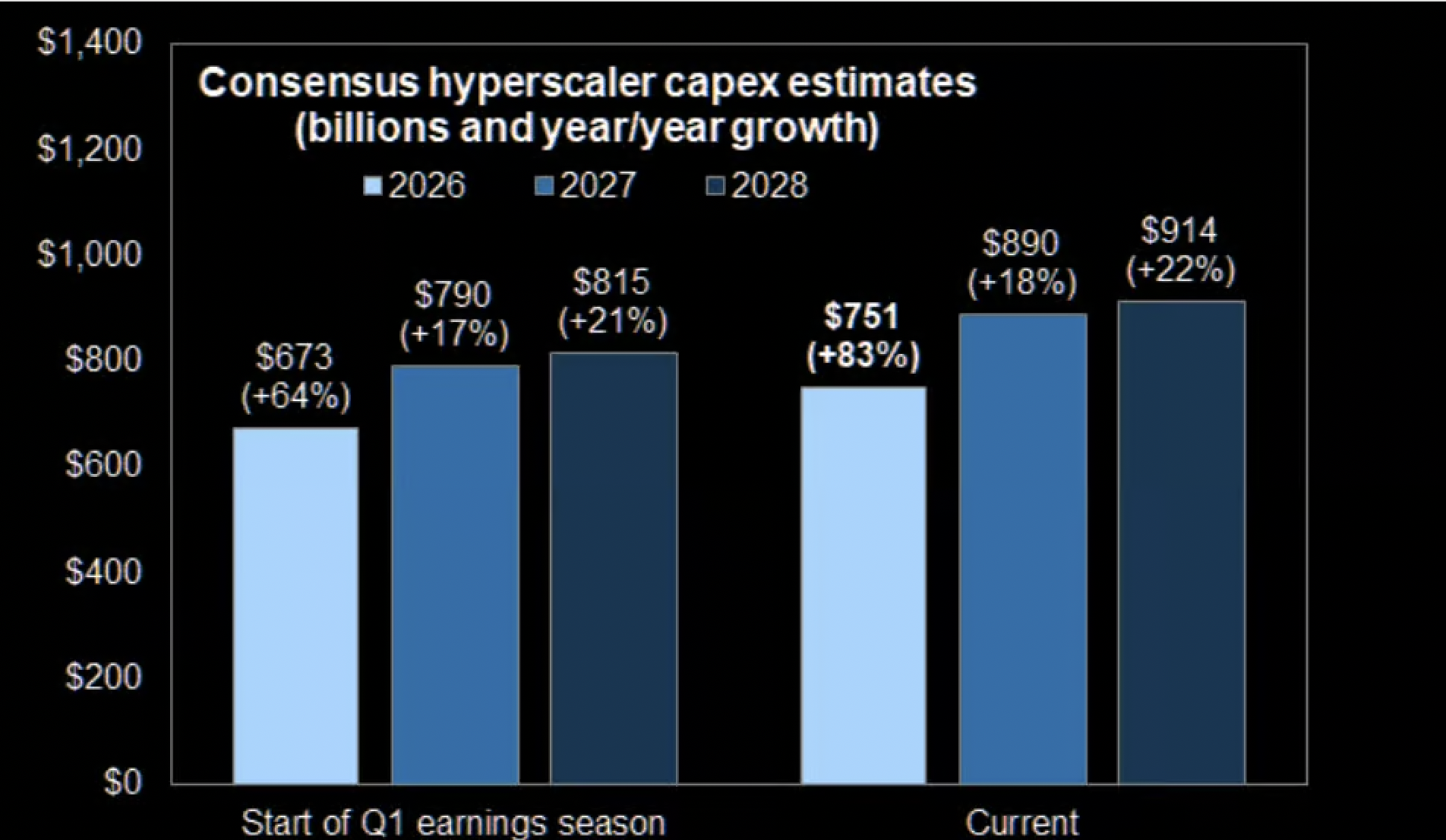

Image Above:

Consensus estimates for hyperscaler capex have moved sharply higher since the start of earnings season.

This confirms what companies are saying:

AI spending is accelerating faster than expected—and still moving up.

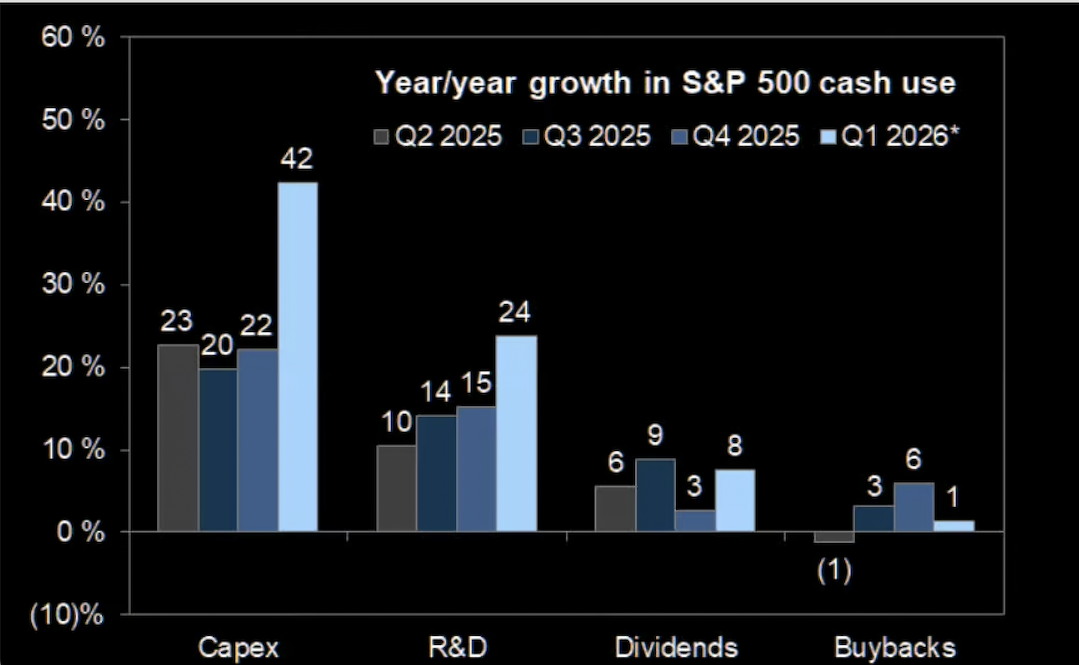

Image Below:

At the same time, how companies are using cash is shifting.

This is a clear change from prior cycles, where excess cash was returned to shareholders.

This reinforces the shift: markets are moving from capital return → capital investment, which raises the bar for future returns.

The Iran conflict is no longer just lifting oil prices—it’s disrupting supply chains and day-to-day operations.

Across earnings, the message is consistent:business remains solid, but disruptions are increasing.

Energy — Strong Results, But More Difficult Conditions

Halliburton delivered solid earnings but said the conflict reduced profits slightly and lowered activity in the Middle East.

Schlumberger reported disruptions, including paused projects and weaker performance in the region as operations were scaled back.

ExxonMobil described a more volatile environment, with tighter supply and more complex logistics requiring rerouting.

Chevron performed well overall, but still saw some production slowdowns tied to the region and emphasized the uncertainty in the external environment.

Higher oil prices are supporting results, but operations are becoming less predictable.

Airlines — Fuel Costs Are Driving Changes

United Airlines remained profitable, but fuel costs increased by $340 million, leading to capacity reductions and schedule adjustments for the rest of the year.

Airlines are responding by reducing flights in some markets, adjusting schedules, and raising fares where possible.

At the same time, Spirit Airlines shut down after failing to secure financing, highlighting how quickly rising costs are affecting weaker operators.

Join LevelFields now to be the first to know about events that affect stock prices and uncover unique investment opportunities. Choose from events, view price reactions, and set event alerts with our AI-powered platform. Don't miss out on daily opportunities from 6,300 companies monitored 24/7. Act on facts, not opinions, and let LevelFields help you become a better investor.

AI scans for events proven to impact stock prices, so you don't have to.

LEARN MORE