.png)

L2 Weekly Stock Market News Analysis

February 22nd, 2026

TLDR:

Markets pushed higher again, led by Energy and Industrials, while digesting softer growth data and a major shift in tariff policy. This wasn’t defensive positioning — it was selective leadership favoring hard assets, domestic production, and companies delivering current earnings over consumer and defensive exposure.

Sector performance reflected that tone. Energy (XLE) led the week, up +2.22%, followed by Industrials (XLI) +2.08% and Utilities (XLU) +1.90%. Financials (XLF) rose +0.89%, Health Care (XLV) gained +0.81%, Real Estate (XLRE) added +0.77%, Technology (XLK) climbed +0.72%, and Communication Services (XLC) advanced +0.44%. At the bottom, Consumer Discretionary (XLY) was nearly flat at +0.09%, Materials (XLB) finished unchanged, and Consumer Staples (XLP) declined –1.73%, making it the clear laggard. The message wasn’t panic — it was preference. Capital leaned toward energy, infrastructure, and domestic exposure while pulling back from consumer defensives.

Growth data added context but didn’t derail sentiment. Q4 US GDP came in at 1.4% annualized, below expectations and down sharply from Q3’s pace. Consumer spending slowed and the government shutdown weighed on the headline number, though business investment remained firm. The takeaway: growth is cooling, not collapsing — reinforcing selective positioning rather than broad risk reduction.

The bigger development came from Washington. The Supreme Court ruled 6–3 that the President cannot use IEEPA to impose broad tariffs, arguing that tariffs function as taxes — a power reserved for Congress. However, the administration quickly pivoted to Section 122 of the Trade Act of 1974, implementing a 15% global tariff for up to 150 days. Markets now face a defined timeline and continued trade-policy uncertainty rather than a clean removal of tariff pressure.

Import-heavy retailers and global brands remain exposed under the new structure, while domestic metals, energy, and industrial producers could remain supported — particularly if the administration later turns to Section 232 national-security tariffs. The result is likely greater dispersion across sectors rather than a unified market move.

Next week centers on Nvidia’s earnings, which will serve as a key test of global AI demand that has supported U.S. equities in recent quarters.

The Supreme Court Decision: What Was Struck Down — and Why

This week, the Supreme Court ruled 6–3 that President Trump cannot use the International Emergency Economic Powers Act (IEEPA) to impose broad tariffs.

IEEPA is a law designed for national emergencies. It allows a president to block transactions, freeze assets, and restrict economic activity when facing foreign threats. It does not explicitly mention tariffs.

The Court’s reasoning was simple: tariffs function as taxes, and the Constitution gives Congress — not the President — the authority to impose taxes. For nearly 50 years, no president had used IEEPA to impose tariffs. The Court viewed this as too large an expansion of executive power.

So IEEPA-based tariffs were struck down. That framework failed.

But the ruling did not say the President lacks tariff authority altogether. It said he cannot use IEEPA for that purpose.

That distinction matters.

The Immediate Pivot: Section 122 Replaces IEEPA

Within 24 hours, Trump announced he would reimpose tariffs using Section 122 of the Trade Act of 1974.

Section 122 allows the President to impose a temporary, across-the-board tariff of up to 15% for 150 days without congressional approval. It is designed to address balance-of-payments problems or currency instability. It does not require a long investigation.

The administration first announced a 10% global tariff, then quickly raised it to the full 15% cap.

In practical terms, that means:

- IEEPA tariffs are gone.

- A 15% global tariff baseline is now in place under a different law.

- The legal structure changed — the economic pressure largely did not.

This is why markets did not get a clean “tariffs are over” moment.

What This Means for Stocks

The impact depends on who imports, who produces domestically, and which authority is used next.

Consumer and Import-Heavy Companies

If tariffs had truly disappeared, import-dependent companies would have been the clearest beneficiaries. Retailers and global brands such as Costco (COST), Walmart (WMT), Nike (NKE), and Crocs (CROX), along with automakers like General Motors (GM) and Ford (F), rely heavily on overseas manufacturing and complex global supply chains. Lower tariffs would directly reduce their costs and support margins.

Nike highlights how significant the impact has been. The company is estimated to have paid roughly $1.5 billion in tariffs — about $1.00 per share — and recently reported Q2 FY26 EPS of $0.53, down 32% year over year, with gross margin falling to 40.6% largely due to higher tariff-related costs. If those costs were refunded or permanently removed, earnings could move closer to about $4.50 per share versus roughly $3.50 under current pressure. With the stock trading near $65, that difference is substantial and shows how heavily tariffs have weighed on performance.

That said, the new 15% global tariff under Section 122 keeps import costs elevated for now. Any recovery in margins depends on whether refunds are granted and whether future tariff policies become narrower rather than broad-based. Autos remain particularly exposed — if tariffs return under national-security authority, manufacturers could once again face higher costs on imported parts or finished vehicles, keeping the sector volatile.

Domestic Metals and Industrial Producers

Industries tied to national security and domestic production remain supported.

Examples include:

- Alcoa (AA) – aluminum

- ATI (ATI) – specialty metals

- Nucor (NUE) – steel

- Cleveland-Cliffs (CLF) – integrated steel

Even though IEEPA failed, tariffs can still be imposed under other laws — particularly Section 232, which allows tariffs on imports that threaten national security.

Section 232 has historically been used for steel and aluminum and could be extended to autos, critical minerals, or industrial inputs.

That means protection for domestic producers is still very much alive.

What Comes Next

With IEEPA struck down, the administration is shifting to other tariff laws. The key question for markets is not “are tariffs gone?” but which authority is used next — and who does it affect?

Section 122 (Now in Place – 15% for 150 Days)

This is the temporary law currently being used. It allows a broad tariff of up to 15% for 150 days without Congress.

That means:

- Import-heavy retailers like Costco (COST), Walmart (WMT), Nike (NKE), and Crocs (CROX) still face higher product costs.

- Automakers such as GM and Ford remain exposed to imported components and finished vehicles.

- Markets now have a visible 150-day clock. As that deadline approaches, volatility will likely increase.

This keeps pressure on consumer names while preserving uncertainty.

Section 301 (Country-Specific Tariffs)

Section 301 allows tariffs against specific countries for unfair trade practices. It takes time because investigations are required, but once imposed, tariffs can be higher and last much longer.

If applied aggressively — particularly toward China — the impact would be concentrated in:

- Companies dependent on Chinese supply chains

- Multinational industrial exporters

- Consumer electronics manufacturers

Retailers and brands sourcing heavily from China would face renewed pressure, while domestically focused small-cap companies could outperform due to lower import exposure.

Section 232 (National Security Tariffs)

Section 232 allows the government to impose tariffs on imports that are considered a national security risk. It has previously been used for steel and aluminum but could be expanded to cover:

- Autos and auto parts

- Semiconductors

- Critical minerals and battery inputs

- Defense-related industrial components

If expanded, the impact would shift toward companies directly tied to domestic production and defense supply chains.

Potential beneficiaries could include:

- U.S. Steel (X) – domestic steel production

- Steel Dynamics (STLD) – U.S.-focused steel manufacturer

- MP Materials (MP) – rare earth production tied to defense and industrial uses

- Freeport-McMoRan (FCX) – copper production, critical for electrification and grid buildout

- Howmet Aerospace (HWM) – aerospace and defense components

- BWX Technologies (BWXT) – nuclear and defense-linked manufacturing

At the same time, higher input costs would pressure:

- Automakers

- Construction companies

- Equipment manufacturers

- Industrial users of metals and specialty materials

The result would likely be wider dispersion within industrial and materials stocks — some names benefiting from protection and pricing power, while downstream users face margin pressure.

Under this path, the broader reindustrialization and domestic production theme remains intact, but stock selection becomes far more important.

The Refund Variable — And Why It Matters

One major unresolved issue is refunds.

Estimates suggest roughly $175 billion may have been collected under the now-invalid IEEPA tariffs. The Supreme Court did not provide a clear refund process. The issue now moves to the U.S. Court of International Trade.

Here’s how it works:

- Importers paid tariffs when goods entered the U.S.

- Customs later finalizes those payments (a process called liquidation, typically about 314 days later).

- Companies generally have two years to file suit for refunds.

- Over 1,000 lawsuits are already pending, and many more could follow.

- Each importer may need to file individually — smaller businesses may face legal costs that deter claims.

- Refunds, if ordered, could take years to distribute.

The trade court has ruled it has authority to reopen final tariff determinations and order refunds with interest, which makes repayment legally possible — but administratively complex.

If large-scale refunds are required:

- Treasury borrowing could rise to finance repayments.

- Bond yields could face upward pressure.

- The U.S. dollar could weaken, particularly against other major currencies — pressuring dollar-linked ETFs like UUP.

- Gold and silver could benefit on deficit concerns.

- Bitcoin could also attract flows as investors look for assets outside the traditional monetary system during periods of fiscal strain.

If refunds are delayed or limited, the macro effect is smaller and the issue becomes more procedural than systemic.

Last's Weeks Sector Winners & Losers

Sector performance was broadly positive, with most areas of the market finishing higher. This wasn’t a defensive flight — it was a steady, controlled advance led by cyclical and real-economy sectors.

Energy (XLE) led the week, up +2.22%, followed by Industrials (XLI) at +2.08% and Utilities (XLU) at +1.90%. The leadership from Energy and Industrials points to continued support for infrastructure, domestic production, and hard-asset exposure.

Behind them, gains were more modest but still positive across most sectors. Financials (XLF) rose +0.89%, Health Care (XLV) gained +0.81%, and Real Estate (XLRE) added +0.77%. Technology (XLK) climbed +0.72%, while Communication Services (XLC) advanced +0.44%.

At the bottom of the table, Consumer Discretionary (XLY) was nearly flat, up just +0.09%, suggesting limited conviction in consumer-driven growth. Materials (XLB) finished unchanged, and Consumer Staples (XLP) was the only sector to decline, down –1.73%, making it the clear laggard.

Upcoming Events This Week

Next week centers on Nvidia’s earnings, which will act as a key test for global AI demand that has supported U.S. equities in recent quarters.

In the U.S., markets will also focus on Producer Price Index (PPI) data, housing prices, consumer confidence, factory orders, and regional Fed activity surveys, alongside speeches from Fed officials following meeting minutes that showed division over the rate outlook.

Globally, attention turns to consumer inflation data in Germany, France, Australia, and Singapore; Q4 GDP reports from Canada, Switzerland, India, and Turkey; and rate decisions from the People’s Bank of China and the Bank of Korea as Asia reopens after Lunar New Year.

Company News

LevelFields AI Stock Alerts Last Week

RingCentral (RNG) +35% — Stock Buyback

RingCentral surged 35% in one day after announcing it increased its share repurchase authorization to $500 million — roughly 12% of its market cap. The move signaled management confidence in cash generation and valuation, reinforced by FY2025 revenue of $2.5B (+5%) and free cash flow of $530M (+32% YoY), alongside the launch of its first quarterly dividend.

Masimo (MASI) +34% — $10 Billion Acquisition Deal

Masimo jumped 34% in one day after agreeing to be acquired in a deal valued at roughly $10 billion. The transaction price represented about a 40% premium to the prior close, immediately re-pricing the stock higher as investors priced in the cash takeout.

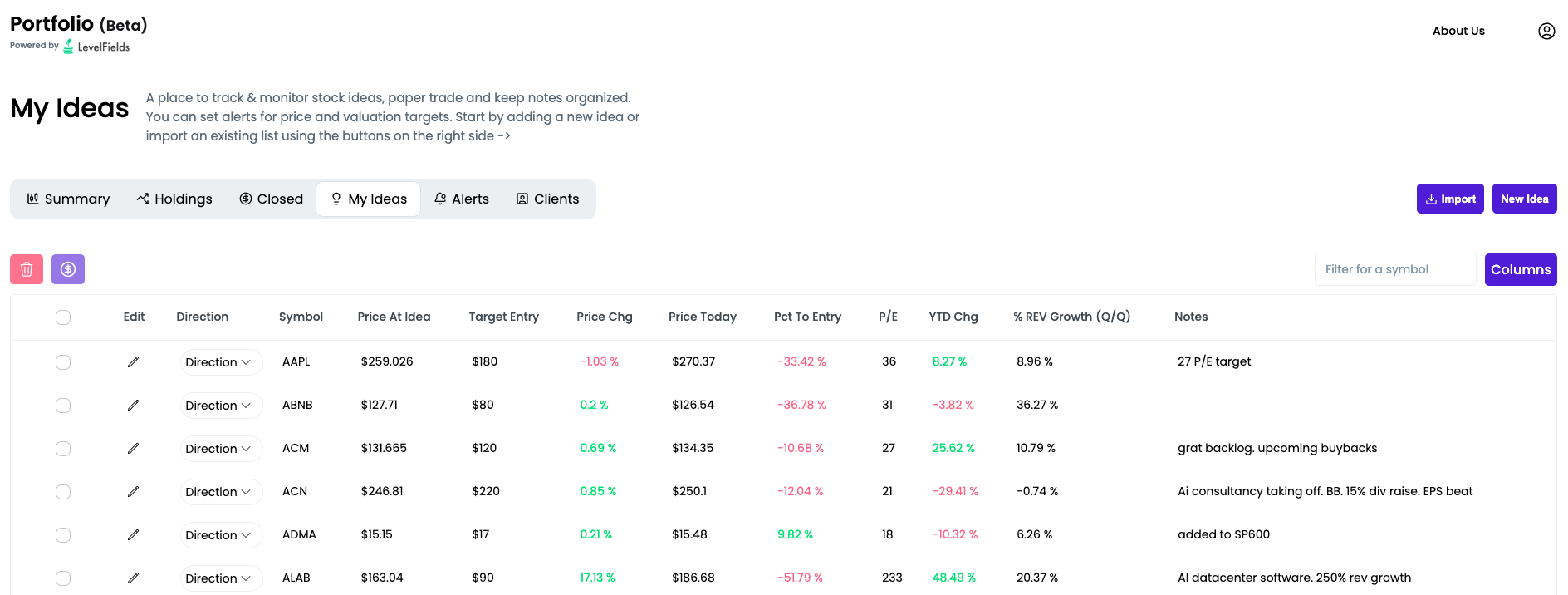

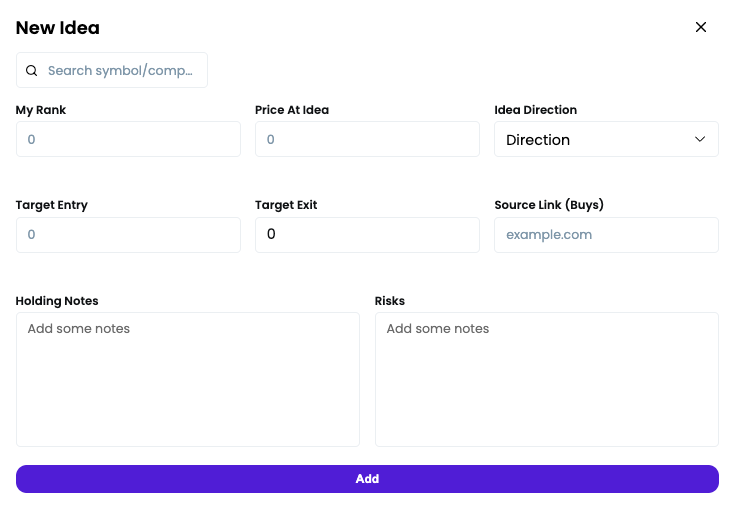

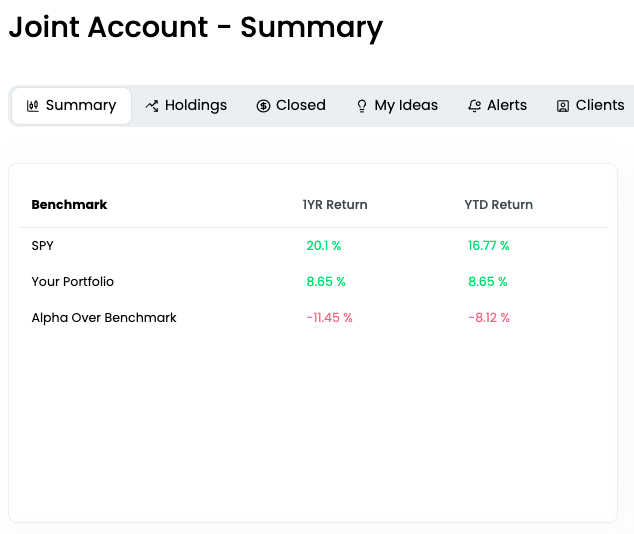

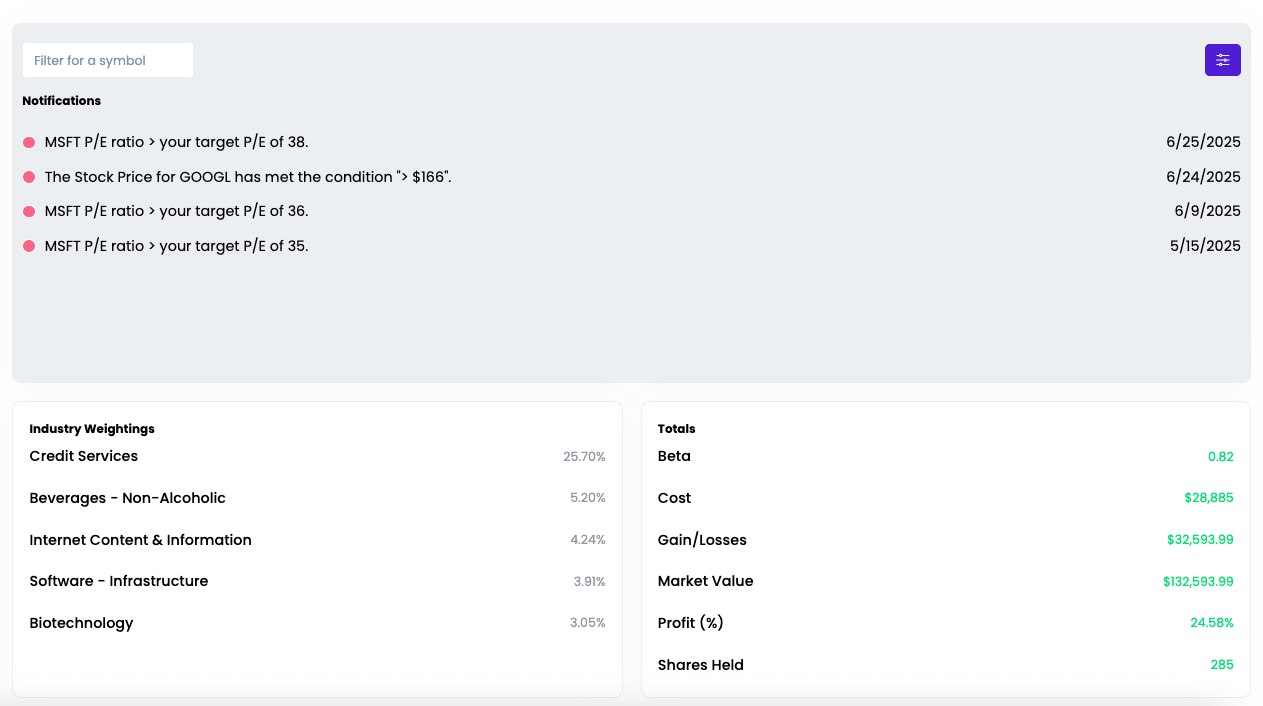

Introducing the LevelFields Portfolio Tracker

We’ve just launched the new LevelFields Portfolio platform — a centralized dashboard built for active investors and wealth managers to track their trades, organize trade ideas, and monitor real or prospective portfolios.

We've replaced Excel and Google Sheets trade tracking with software that updates as prices and valuations of stocks change, so you don't lose money by missing great entry and exit points.

You can sign up for free!

What it does:

- Lets you add both real positions and idea-stage trades into one unified portfolio.

- Tracks allocation, profit/loss, KPIs, P/E, price targets, and thesis notes in one place.

- Allows you to set real-time alerts on valuation changes, price moves, and price targets using bulk editing (e.g. one alert for all holdings).

- Lets you toggle any ticker between “Idea → Holding → Closed” while preserving the original trade thesis and exit notes.

- Designed for traders, advisors, and fund managers who need a live, organized view of positions + rationale, not just a static spreadsheet of tickers.

- Import CSV file of existing ideas, notes, and portfolio holdings for a quick start

- Keep track of reasons you bought and sold to analyze your performance and for compliance

- Design your own model portfolios based on allocations, sector, and industry

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai