L2 Weekly Stock Market News Analysis

March 22nd, 2026

TLDR:

Markets head into the week of March 23 with three main risks in focus: the Middle East oil shock, a tougher Fed, and growing stress in private credit. Iran and the Strait of Hormuz remain the biggest swing factor, with higher oil prices now raising risks not just for energy, but also for inflation, shipping costs, and supply chains.

The Fed kept rates at 3.50%–3.75% on March 18, but its message was tougher than markets wanted. Officials raised their inflation outlook, showed less room for rate cuts, and signaled that higher oil prices could make it harder to lower rates.

At the same time, problems in private credit are becoming harder to ignore. Tighter lending, more investor withdrawals, and weaker fund performance are adding another layer of risk as markets already deal with high rates and geopolitical tension.

Market action still looks cautious. Energy continues to lead, while the broader stock market remains under pressure as investors pull money from economically sensitive and rate-sensitive areas. This week, the focus will be on whether new data show a mix of slower growth and sticky inflation.

Sector performance last week showed broad weakness across the market. Energy (XLE) was the top performer, rising +2.79%, while Financials (XLF) also posted a small gain of +0.39%. Losses were widespread elsewhere, with Technology (XLK) down -1.10%, Industrials (XLI) down -1.81%, and Communication Services (XLC) down -1.94%. The biggest declines came from Consumer Discretionary (XLY) down -2.81%, Health Care (XLV) down -2.98%, Real Estate (XLRE) down -3.93%, Consumer Staples (XLP) down -4.07%, Materials (XLB) down -4.49%, and Utilities (XLU) down -4.92%, showing broad weakness in most sectors.

Federal Reserve: Holding Steady as Constraints Build

The Federal Reserve held rates at 3.50%–3.75%, in line with expectations, but the underlying message shifted in a more restrictive direction.

While the policy decision itself was uneventful, the Statement of Economic Projections showed higher inflation expectations, and officials explicitly highlighted uncertainty tied to the Iran conflict and rising energy prices.

More importantly, market expectations have adjusted meaningfully:

- Rate cuts have been pushed further out

- Financial conditions are tightening without a policy move

- Inflation risks are re-emerging as a dominant concern

The result is a “hold under pressure” environment. The Fed is not easing, but conditions are tightening anyway — driven externally by energy markets and geopolitics rather than domestic demand.

This shifts the focus away from policy decisions themselves and toward what is driving policy constraints.

Iran Escalation and Oil: From Price Shock to Flow Shock

The situation in the Middle East has moved beyond a geopolitical headline into a structural disruption of global energy flows.

Iran has escalated its posture significantly:

- Threatening to target regional infrastructure

- Imposing a $2 million transit fee through the Strait of Hormuz

- Restricting access to certain vessels based on alignment

At the same time, the key dynamic is not production capacity but transportation and logistics.

The Strait of Hormuz remains one of the most critical chokepoints in the global economy, and disruptions there are already impacting flows. Even under optimistic scenarios, normalization is unlikely to be immediate due to:

- Insurance delays

- Mine clearing

- Vessel repositioning

- Backlog of shipments

This introduces a critical shift in how oil should be understood:

The market is no longer pricing supply — it is pricing duration of disruption.

Scenario analysis suggests:

- Short disruption → contained move

- Multi-month disruption → materially higher oil prices

- Prolonged disruption → severe dislocation

The key takeaway is that time, not just magnitude, is now the dominant variable.

Price Increases and the Inflation Pipeline

The most important development is not just the rise in oil prices, but the broad-based repricing across commodities that sit downstream of energy.

Since the start of the Iran conflict:

- European Natural Gas: +85%

- Heating Oil: +80%

- Brent Crude: +54%

- Gasoline: +44%

- Diesel: +42%

- Urea: +48%

- Fertilizer (aggregate): +23%

- Coal: +24%

- Palm Oil, Rice, Iron Ore: all moving higher

Fertilizer prices have risen 44% year-over-year to their highest levels since September 2022, and roughly one-third of global fertilizer supply moves through the Strait of Hormuz.

This creates a clear transmission mechanism:

- Energy prices rise

- Fertilizer costs increase

- Agricultural production becomes more expensive

- Food prices rise with a lag

This is a classic second-order inflation effect — and one that tends to be more persistent than the initial energy shock.

The implication is that inflation pressures are likely to broaden over the coming months, even if energy prices stabilize.

This ties directly back to the Federal Reserve.

Rising energy and food prices complicate the policy outlook by:

- Keeping inflation elevated

- Limiting flexibility in easing policy

- Tightening financial conditions indirectly

In effect, external supply shocks are doing the tightening for the Fed.

Image Below: U.S. 12-month inflation expectations have jumped to 5.2% — the highest since March 2023 — marking a sharp shift in sentiment. In just three weeks, markets have swung from anticipating rate cuts to pricing in a more restrictive policy outlook.

Positioning for the Current Setup

This environment is characterized by supply constraints, rising input costs, and increasing macro uncertainty. Positioning should reflect that shift.

Energy (XLE, XOM, CVX)

The market continues to price a relatively short-lived disruption. If constraints persist, energy markets remain supported by tight balances and limited spare capacity. Exposure to large-cap, integrated producers provides leverage to sustained pricing strength.

Fertilizers (MOS, CF, NTR)

Fertilizers represent a direct second-order beneficiary of rising energy prices. With pricing already up significantly and supply routes exposed to Hormuz disruptions, the sector is positioned to benefit from both cost pass-through and tightening supply conditions.

Energy Infrastructure and Power (GNRC, ETN, VRT)

Volatility in energy markets increases demand for reliable power solutions, particularly in industrial and data center applications. These businesses benefit from structural demand tied to electrification and grid instability rather than short-term cycles.

Hard Assets / Gold (GLD, physical, select miners)

With inflation pressures rising and policy flexibility constrained, gold continues to serve as a hedge against macro uncertainty and currency debasement risks. Demand from central banks and institutional investors remains supportive.

Caution on Cyclicals and Credit-Sensitive Areas

Sectors tied closely to economic growth and financing conditions — particularly financials, small caps, and highly leveraged companies — face increasing pressure as input costs rise and financial conditions tighten.

Last's Weeks Sector Winners & Losers

Sector performance last week showed broad weakness across the market, with only two sectors finishing higher. Energy (XLE) led the market, rising +2.79%, as investors continued to lean into oil exposure tied to Middle East tensions. Financials (XLF) also posted a small gain of +0.39%.

Losses were widespread across the rest of the market. Technology (XLK) fell -1.10%, Industrials (XLI) dropped -1.81%, and Communication Services (XLC) declined -1.94%. Consumer Discretionary (XLY) also came under pressure, falling -2.81%, while Health Care (XLV) lost -2.98%.

The weakest areas of the market were more defensive and commodity-linked sectors. Real Estate (XLRE) fell -3.93%, Consumer Staples (XLP) dropped -4.07%, Materials (XLB) declined -4.49%, and Utilities (XLU) was the worst-performing sector of the week, down -4.92%.

Overall, the pattern suggests investors stayed concentrated in energy while weakness spread across most other parts of the market.

This week will focus on the Middle East conflict, oil futures, and several key economic reports that could shape expectations for interest rates, growth, and inflation. Crude oil is trading near $98 per barrel after ending last week at its highest level in nearly four years, while Brent is above $111. That sharp move higher in energy prices is now a major part of the market story, because it could lift fuel costs, push inflation higher, and put more pressure on consumers and businesses at the same time.

The main event will be Monday’s March flash PMI reports. These are important because they give one of the first broad readings on how factories and service businesses are doing late in the month. Investors will be watching for signs that demand is slowing, costs are rising, or supply problems are getting worse as oil prices climb and geopolitical tensions remain elevated.

Markets will also track several key U.S. releases later in the week. Durable goods orders will show whether business spending on big-ticket items is holding up, weekly jobless claims will give another read on labor market strength, and new home sales will show whether housing demand is staying firm. On Friday, the final March consumer sentiment report will be closely watched for signs of how households are reacting to higher prices and rising uncertainty.

Outside the U.S., investors will also watch central bank decisions in Norway and Mexico for clues on how policymakers are handling slower growth risks and inflation pressure. The key question for markets this week is whether higher oil prices remain a temporary shock or start to create a bigger problem for growth, inflation, and rate expectations.

Company News

LevelFields AI Stock Alerts Last Week

Torrid Holdings (CURV) +28% — Strong Results + 2026 OutlookTorrid surged 28% in one day after reporting better-than-expected fourth-quarter and full-year 2025 results, while also issuing 2026 guidance above expectations. The company said full-year adjusted EBITDA reached $63.6 million and guided 2026 sales to $940 million–$960 million.Investors reacted positively because the report showed signs that the business is stabilizing. Management highlighted store closures, growth from newer brands, and improving early first-quarter trends as reasons for stronger confidence going forward.

Ovid Therapeutics (OVID) +14% — FDA Designation + Pipeline UpdateOvid rose 14% after announcing that OV329 received Breakthrough Therapy designation, alongside new data and broader pipeline updates. The company said OV329 continued to show a favorable safety profile and is advancing into Phase 2 development.Investors reacted positively because the designation strengthens the regulatory path for OV329 and improves the program’s commercial outlook. The update also showed continued pipeline progress and a cash position expected to fund operations into late 2028.

Swarmer (SWMR) +500% — Small IPO Drives Huge DebutSwarmer surged more than 500% in its public market debut after pricing a small $15 million IPO with limited available shares. The stock opened far above its IPO price and continued climbing through its first trading day.Investors piled in because Swarmer is tied to the high-interest defense drone and AI theme. The company’s small float, combined with strong demand for defense-related names, helped fuel the sharp move higher.

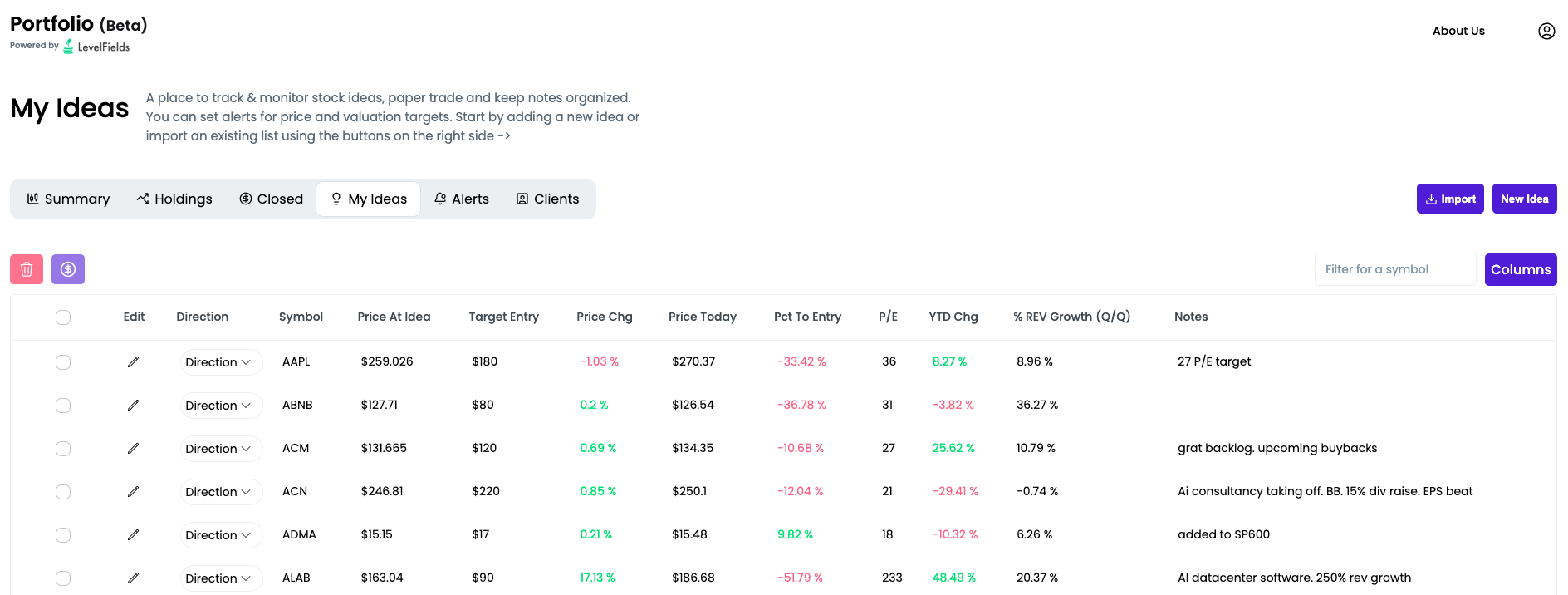

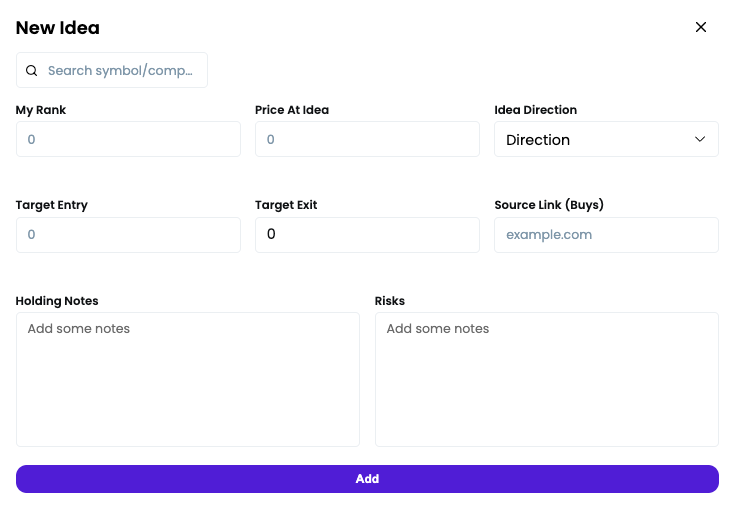

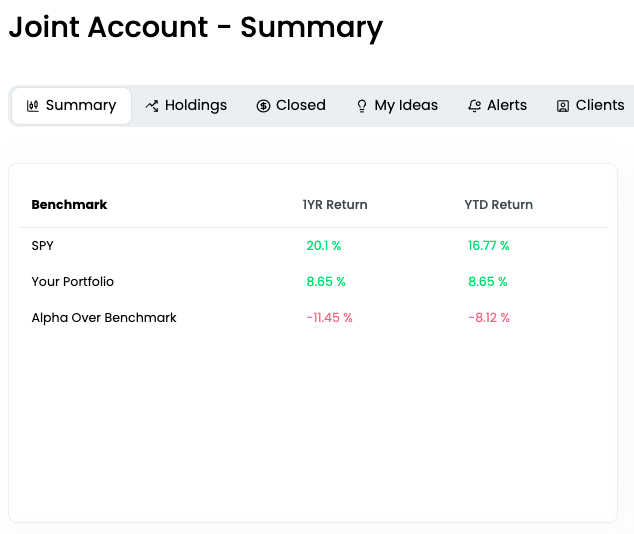

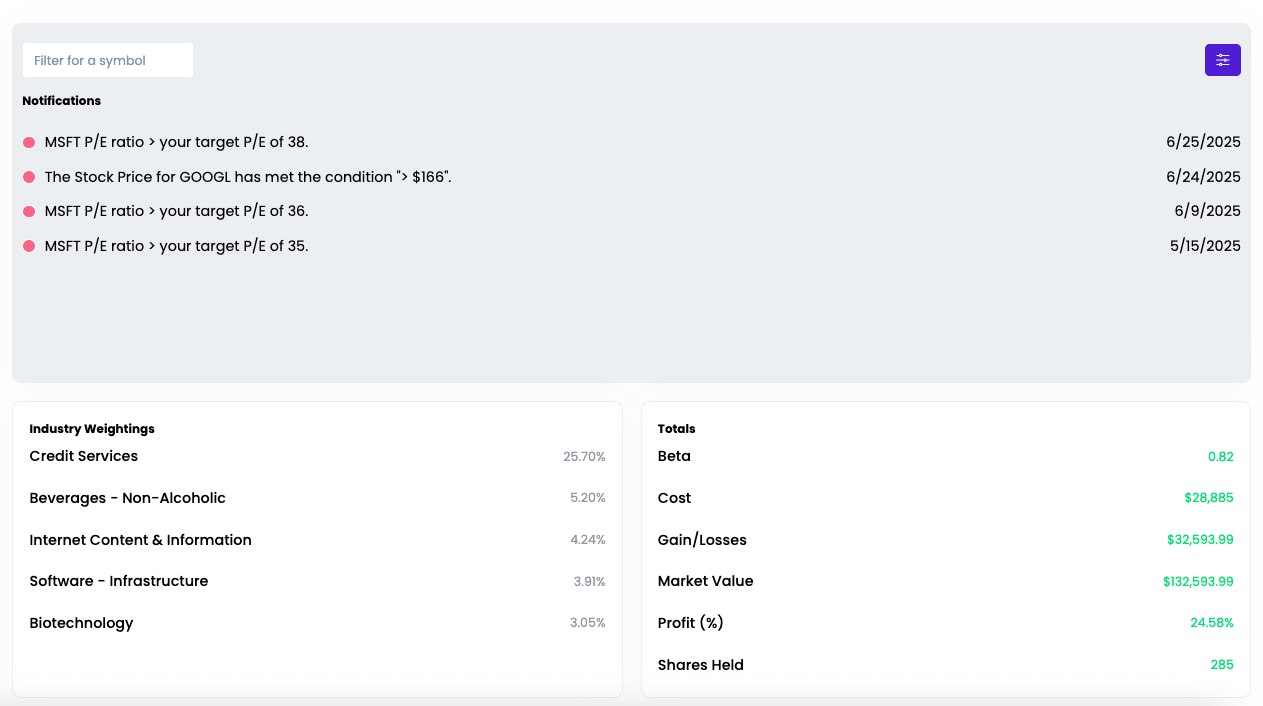

Introducing the LevelFields Portfolio Tracker

We’ve just launched the new LevelFields Portfolio platform — a centralized dashboard built for active investors and wealth managers to track their trades, organize trade ideas, and monitor real or prospective portfolios.

We've replaced Excel and Google Sheets trade tracking with software that updates as prices and valuations of stocks change, so you don't lose money by missing great entry and exit points.

You can sign up for free!

What it does:

- Lets you add both real positions and idea-stage trades into one unified portfolio.

- Tracks allocation, profit/loss, KPIs, P/E, price targets, and thesis notes in one place.

- Allows you to set real-time alerts on valuation changes, price moves, and price targets using bulk editing (e.g. one alert for all holdings).

- Lets you toggle any ticker between “Idea → Holding → Closed” while preserving the original trade thesis and exit notes.

- Designed for traders, advisors, and fund managers who need a live, organized view of positions + rationale, not just a static spreadsheet of tickers.

- Import CSV file of existing ideas, notes, and portfolio holdings for a quick start

- Keep track of reasons you bought and sold to analyze your performance and for compliance

- Design your own model portfolios based on allocations, sector, and industry

-

.png)

How to use LevelFields for Options Trading

The Truth About Dividend Stocks

Tracking Stocks Without Spreadsheets

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai