L2 Weekly Stock Market News Analysis

April 13th, 2026

TLDR:

Markets head into the week with momentum shifting, but conviction remains low.

Last week’s rally was driven by optimism around peace talks and a pullback in oil, pushing cyclicals and growth higher. That optimism has now faded. With negotiations breaking down and escalation risks rising again, markets are back to trading headlines and energy.

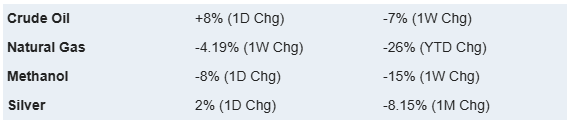

Energy remains the dominant driver, but the dynamic has changed. It’s no longer just about supply levels—it’s about reliability of flows. Tanker traffic has become unstable, routes are shifting in real time, and pricing is increasingly reflecting uncertainty rather than just outright shortages.

At the same time, the macro backdrop is becoming more complex.

Inflation is reaccelerating, with CPI jumping sharply on higher gasoline prices, while growth is slowing, with GDP revised down to just 0.5%. That combination—higher prices and weaker growth—limits the Fed’s flexibility. Strong labor data supports holding rates, but rising energy costs make it harder to move toward cuts.

Earnings now become the next key variable.

As energy costs move through the system, the impact shifts from commodities to margins and demand. Companies are heading into earnings facing higher input costs and a consumer that is already starting to reallocate spending toward essentials.

The focus this week is whether earnings and guidance begin to reflect that shift—or if markets continue to look through it. At the same time, any movement in oil tied to geopolitical developments will continue to dictate short-term direction.

Peace Talks Collapse — Markets Shift Back to Escalation Risk

Over the weekend, the market got its answer: there is no near-term resolution.

U.S.–Iran negotiations in Islamabad broke down after nearly 20 hours of talks, with the core issue unchanged—Iran refused to give up its nuclear ambitions. That single sticking point outweighed progress on everything else and ultimately derailed the deal.

What followed was immediate escalation.

The U.S. has now moved forward with a naval blockade targeting vessels tied to Iranian ports, while Iran has threatened retaliation and made clear it will not accept restrictions on its leverage in the region.

The market reaction wasn’t just higher oil—it was a shift in behavior.

- Tanker flows became unstable, with vessels turning away mid-route

- Traffic visibility collapsed, even without a full closure

- Pricing began reflecting uncertainty, not just supply loss

That distinction matters.

Markets aren’t just reacting to how much oil is available—they’re reacting to how predictable the system is. When flows become unreliable, even partially, it forces traders, insurers, and buyers to reprice risk immediately.

At the same time, the U.S. is increasingly acting as a “supplier of last resort,” stepping in to offset disrupted flows. President Trump reinforced that view directly, stating the U.S. has “much more oil” than Russia and Saudi Arabia combined and that tankers are already rerouting—“boats are coming here & filling up. We don’t have to go through Hormuz.”

The shift is no longer just about disruption—it’s about control.

Last week, markets were balancing the possibility of a deal. Now they are being forced to price a prolonged standoff where energy flows, pricing, and leverage are all actively in flux.

Image Below: vessel-tracking data highlighting tankers with U.S. destinations shows how global flows are increasingly being redirected toward American ports. Even amid disruptions around Hormuz, the U.S. is emerging as the world’s de facto “emergency gas station,” absorbing demand as other routes become less reliable.

Inflation Is Reaccelerating — But It’s Still an Energy Shock

This week’s data confirms the worst-case macro mix is starting to form: higher inflation and weaker growth.

CPI surged 0.9% month-over-month in March, the largest increase since 2022, with gasoline accounting for nearly three-quarters of the move. Year-over-year inflation rose to 3.3%, reversing the recent cooling trend.

At the same time, the growth picture is deteriorating.

U.S. GDP was revised down to just 0.5% annualized growth in the fourth quarter, a sharp slowdown from the ~4% pace seen earlier in 2025. Consumer spending weakened materially, and underlying demand (excluding volatile components) also decelerated.

That combination matters.

On the surface, inflation is rising—but it’s being driven almost entirely by energy. Core inflation remains relatively contained, showing that broader demand is not overheating.

In fact, the opposite is happening.

Higher oil prices are acting as a tax on consumers:

- More money spent on gas

- Less available for discretionary goods

- Slower overall consumption

This is why oil shocks don’t automatically create sustained inflation—they shift spending rather than expand it unless supported by new liquidity.

But in the real world, these shocks don’t stay isolated.

Higher energy costs feed into:

- Transportation

- Food (fertilizers)

- Corporate margins

And those effects take time to show up.

The result is a difficult setup for the Fed:

- Inflation is moving higher

- Growth is slowing

- Policy flexibility is limited

Why This Inflation Cycle Looks Different

An energy-driven inflation spike behaves very differently from what we saw in 2020–2022.

Back then, inflation was driven by a combination of:

- Massive money supply expansion

- Pent-up demand from lockdowns

- Supply chain breakdowns

- Energy shocks layered on top

That created a broad, persistent inflation cycle where demand consistently outpaced supply across the economy.

This time, the driver is much narrower.

An energy shock pulls spending forward into essentials rather than expanding total demand. Consumers don’t suddenly have more money—they’re reallocating what they already have. That creates faster transmission through prices, but also faster feedback into the economy.

The result is a more volatile cycle:

- Inflation spikes quickly as energy rises

- Growth slows almost immediately as consumption gets squeezed

- Demand destruction follows, which eventually pressures prices back down

Instead of a sustained inflation regime, this setup tends to produce sharper up-and-down moves in both inflation and growth.

That’s why the current environment looks less like a prolonged inflation cycle—and more like a shorter, more unstable shock that forces faster market and policy reactions.

How to Position — Trade the Shock and the Spillovers

1. If the Conflict Persists (No Deal / Escalation)

Primary beneficiaries:

- Oil majors: XOM, CVX, OXY → higher realized prices as supply tightens

- LNG / gas exporters: LNG, VG → U.S. supply fills gaps as global flows reroute

- Fertilizers: MOS, IPI, NTR → Middle East disruption tightens nutrient supply

As oil rises, spending shifts across the economy:

- CASY (Casey’s) → higher pump prices increase total dollar sales per gallon and drive in-store traffic

- Fuel / travel centers → benefit from higher fuel prices and sustained demand

At the same time, the conflict is physically damaging infrastructure across the region:

- ERII (desalination / water systems) → Gulf facilities have already been targeted, and rebuilding water and energy infrastructure becomes a priority

The key dynamic is simple:

- More money goes toward energy

- Less goes toward discretionary spending

- Costs rise across logistics and production

2. The Underappreciated Trade — Earnings Pressure

This is where the bigger opportunity is developing. We are now entering earnings season.

As consumers spend more on energy, they cut back elsewhere. That hits discretionary demand and margins across multiple sectors.

Most exposed:

- Retail / discretionary: TGT, WMT, HD, LOW

- Restaurants: MCD, SBUX, CMG

- Travel / airlines: DAL, UAL, AAL

- Logistics / shipping: FDX, UPS

These companies face:

- Higher input and transportation costs

- Slower demand from consumers

- Limited ability to pass through prices

That combination leads to margin compression and weaker guidance, which is typically when stocks reprice.

3. If a Deal Emerges (De-escalation)

The unwind is just as important—and likely fast.

- Oil moves lower

- Inflation pressure eases

- Rates stabilize or fall

Beneficiaries shift to rate-sensitive and cost-sensitive areas:

- Large-cap tech: MSFT, NVDA, AAPL

- Rate-sensitive growth / software: CRM, NOW, ADBE, INTU

- Consumer discretionary rebound: AMZN, TSLA, HD, LOW

- Housing: DHI, LEN, PHM

- REITs / real estate: PLD, AMT, O

- Utilities (bond proxies): NEE, DUK

Fuel-sensitive names also benefit directly from lower input costs:

- Airlines: DAL, UAL, AAL

- Cruises / travel: CCL, RCL

This is where the market shifts from pricing disruption to pricing normalization, with lower energy costs easing both inflation pressure and corporate cost structures.

Last's Weeks Sector Winners & Losers

Sector performance last week reflected a broad risk-on rally following initial optimism around peace talks and a pullback in oil prices.

Cyclicals and growth led the move, with Industrials (XLI) up +5.14%, Technology (XLK) gaining +4.47%, and Consumer Discretionary (XLY) rising +4.24%. Financials (XLF) also moved higher, up +3.63%, alongside Real Estate (XLRE) at +2.69% and Materials (XLB) at +2.50%.

Defensives participated but lagged, with Consumer Staples (XLP) up +1.90%, Utilities (XLU) +1.75%, and Health Care (XLV) +1.72%.

Energy (XLE) was the only sector to decline, falling -3.24% as oil prices pulled back on expectations of de-escalation.

The rotation highlights how quickly positioning shifted—markets moved into growth, cyclicals, and rate-sensitive areas on the prospect of a resolution, while energy unwound alongside the drop in oil.

Upcoming Events This Week

The Middle East remains the primary driver, with ceasefire talks still fragile and energy flows through the region not yet normalized. Any headlines around negotiations or escalation will continue to move oil—and by extension, the broader market.

In the U.S., producer price data (PPI) will be the key release, offering the first look at how the recent surge in energy prices is feeding into costs for businesses. Headline PPI is expected to rise sharply, which could reinforce concerns around margin pressure heading into earnings season.

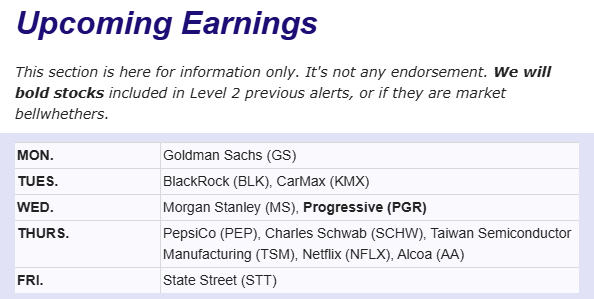

Earnings season also begins to pick up, with a heavy focus on financials:

- JPMorgan, Goldman Sachs, Bank of America, Wells Fargo, Citigroup, Morgan Stanley, BlackRock

These reports will provide early insight into:

- Consumer health

- Credit conditions

- Market activity and positioning

On the industrial and housing side, data including industrial production, housing market index, and existing home sales will help gauge how growth is holding up following the recent slowdown.

Globally, China will be a major focus with a full slate of data:

- GDP, industrial production, retail sales, trade, unemployment, housing, and credit data

This will offer a broader read on global demand at a time when energy shocks are starting to ripple through supply chains.

In tech, TSMC and ASML will report, setting the tone for AI and semiconductor demand.

On the policy front, multiple Federal Reserve speakers are scheduled throughout the week, which could provide further clarity on how policymakers are interpreting the recent inflation spike.

Finally, the IMF and World Bank Spring Meetings and Hungary’s elections will be watched for any signals around global growth, policy direction, and geopolitical alignment.

Company News

LevelFields AI Stock Alerts Last Week

Greenlane Holdings (GNLN) +21.6% — Digital Asset Strategy + Buyback

Greenlane Holdings surged after announcing a digital asset treasury update alongside a $2.0 million share repurchase program. With a market cap of just ~$1.8 million, the size of the buyback is significant relative to the company’s valuation.

Investors reacted to both the capital allocation shift and the signal of confidence from management. At this scale, even modest buybacks can meaningfully impact the float, which helped drive the sharp move higher.

Subsea 7 (SUBCY) +6% — $1.25B+ Offshore Contract Award

Subsea 7 moved higher after announcing a supermajor contract (>$1.25 billion) with Petrobras for the development of the Sépia 2 offshore field in Brazil.

The contract covers engineering, procurement, and installation for a large-scale deepwater project tied to Brazil’s pre-salt expansion—one of the most important growth areas in global oil production.

Investors reacted to the size and strategic importance of the award, which strengthens Subsea 7’s backlog and reinforces its position in offshore energy infrastructure at a time when global energy investment is rising.

Other Company News

Intel Surges on AI Momentum — But Earnings Will Decide If It Holds

Intel has quickly become one of the market’s hottest stocks, rallying sharply over the past two weeks and adding over $100B in market value as a wave of positive headlines reignited the turnaround narrative.

The move has been driven by a series of developments that all point in the same direction: Intel positioning itself as a core player in AI infrastructure.

A key catalyst is still the $14.2B buyback of its Ireland Fab 34 stake, which signals a shift back into expansion mode and gives Intel full control over a key manufacturing asset. On top of that, the company has stacked multiple high-profile partnerships:

- A multi-year collaboration with Google to co-develop AI and cloud infrastructure using Xeon CPUs and custom IPUs

- Participation in Musk’s Terafab project, a massive AI chip manufacturing initiative

- Continued push into 18A process manufacturing, positioning Intel as a U.S.-based foundry alternative

Taken together, these moves reinforce the idea that Intel is no longer just stabilizing—it’s trying to reassert itself at the center of the AI buildout.

That’s what the market is reacting to.

But the financials haven’t caught up yet.

Recent results still show:

- Declining revenue and weak near-term guidance

- Margin compression

- Negative free cash flow

- A foundry business losing over $10B annually

At the same time, the stock is now trading at extremely elevated forward multiples, reflecting expectations of a successful turnaround rather than current performance.

That’s what makes the upcoming April 23 earnings report critical.

After a move of this size, the question isn’t just whether Intel is improving—it’s whether the improvement is happening fast enough to justify the re-rating.

There are two ways this can play out:

- If Intel shows stabilization in revenue declines, continued AI/data center strength, and progress on foundry economics, the rally can extend as the narrative starts to get validated.

- If results continue to lag while expectations keep rising, the stock risks a reset as the gap between story and fundamentals becomes harder to justify.

There’s also a real possibility the move is front-running good news.

With multiple partnerships announced in quick succession and a clear push into AI infrastructure, investors appear to be positioning ahead of improved guidance or forward commentary.

That creates a familiar setup.

When a stock rallies this aggressively into earnings—especially on narrative rather than financial improvement—it raises the risk of a “sell the earnings” reaction if the results don’t match the expectations being priced in.

Bottom line:

Intel’s rally is being driven by narrative acceleration around AI and manufacturing. Earnings will determine whether that narrative is being confirmed—or priced in ahead of reality.

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai