.png)

L2 Weekly Stock Market News Analysis

May 3rd, 2026

TLDR:

Markets are being driven by policy uncertainty, AI investment, and energy disruption.

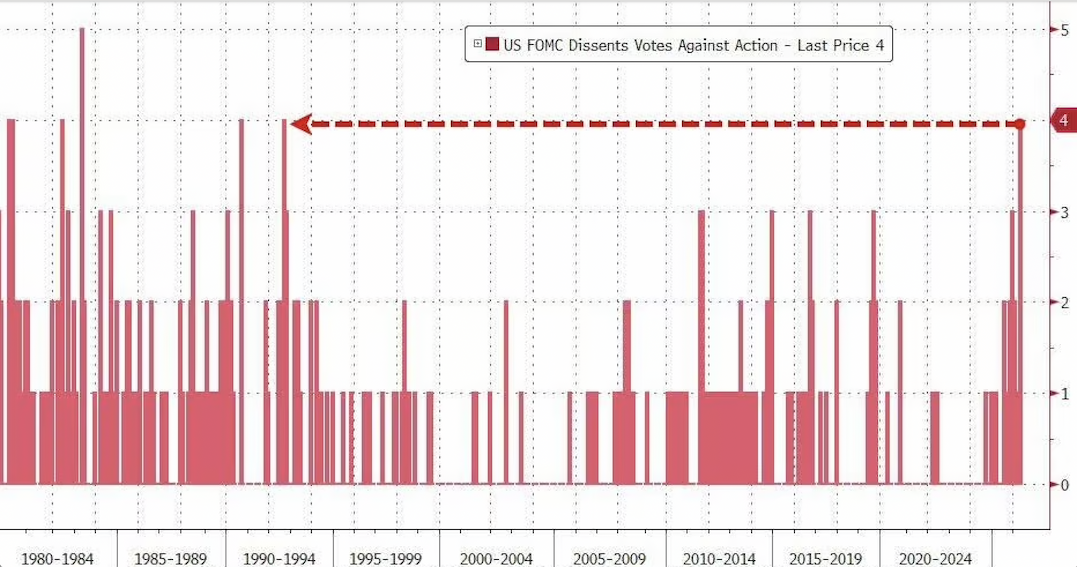

The Fed is no longer aligned. An 8–4 vote split, including three dissents against any easing bias, shows growing resistance to rate cuts. Inflation has moved back toward ~3.3%, and rising energy prices tied to the Iran conflict are making the path forward less clear. While Warsh is expected to lean more dovish, he is stepping into a committee that is shifting toward neutrality and may be less willing to ease than markets expect.

Earnings remain strong, with S&P 500 growth tracking mid-20% YoY and Big Tech driving ~50%+ growth. But the market is becoming more selective. AI spending is accelerating rapidly, with hyperscaler capex now expected to exceed ~$750B in 2026 and continue rising. The focus is shifting from growth to returns, with companies that show clear monetization being rewarded, while those increasing spend without near-term payoff are seeing weaker reactions.

That shift is reinforced by how companies are using cash. Capex and R&D are rising sharply, while buybacks remain flat. Capital is being reinvested into AI infrastructure rather than returned to shareholders, raising the bar for future performance.

At the same time, the Iran conflict is moving beyond oil prices and into operations. Energy companies are still benefiting from higher prices, but are reporting disruptions, rerouting, and reduced activity in key regions. Airlines are seeing a more immediate impact, with fuel costs rising sharply and capacity being cut. The shutdown of Spirit Airlines highlights how quickly weaker players are being affected.

Sector performance reflects this environment. Energy (+4.69%) and Technology (+2.35%) led, while defensives and cyclicals posted more modest moves. The market is not fully risk-on—it is positioning selectively around energy, AI, and policy.

Looking ahead, the key catalysts are Iran headlines, labor market data (jobs, ADP, JOLTS), and a broad set of earnings across tech, consumer, and industrial companies.

Fed Transition + Political Pressure — Policy Path Is Getting Less Clear

The latest Fed meeting exposed a meaningful shift beneath the surface.

Rates were held at 3.50–3.75%, but the decision came with an 8–4 vote split—the most divided outcome in decades and a clear sign that policymakers are no longer aligned on the path forward.

The breakdown:

- One member pushed for a rate cut

- Three opposed maintaining any easing bias, signaling resistance to cuts altogether

This reflects a clear divide:

- One side sees slowing momentum and is ready to ease

- The other is focused on inflation risks that are rebuilding

That inflation concern is no longer abstract:

- CPI has moved back toward ~3.3%

- The Fed explicitly upgraded its language, now calling inflation “elevated” and linking it to rising global energy prices

- Middle East developments are now described as a “high level of uncertainty” for the outlook

At the same time, Powell indicated the center of the committee is shifting toward a neutral stance—meaning policy could move either direction depending on data, rather than being biased toward cuts.

He also made clear why the Fed is so divided: policymakers are trying to interpret an economy shaped by repeated supply shocks—pandemic disruptions, tariffs, and now the Iran-driven energy shock—which are pushing inflation higher while making growth harder to read.

Leadership is also in transition.

Powell confirmed he will remain on the Board after stepping down as Chair, while Kevin Warsh moves toward taking over—an unusual overlap that adds another layer of uncertainty.

Warsh is generally viewed as more open to rate cuts, but he is stepping into a committee already pushing back against easing, with three dissents against maintaining an easing bias and a broader shift toward neutrality across the Fed. Convincing the committee to ease further is likely to be an uphill battle.

The implication for markets:

- Rate cuts are no longer a clear base case

- Policy is increasingly reactive to inflation shocks—especially energy

- The range of outcomes for rates is widening

- MSFT, NVDA, AMZN → more sensitive to rate repricing

- JPM, BAC → supported by higher rates, but exposed if credit tightens

- XLU, XLRE → remain under pressure in a higher-rate environment

Earnings — Strong Growth, But the Market Is Getting More Selective

Earnings season has come in significantly stronger than expected.

- S&P 500 earnings are tracking roughly mid-20% YoY growth

- Big Tech continues to lead, with ~50%+ earnings growth driving index performance

- Miss rates are near their lowest levels since 2021, with strength extending beyond tech into banks and small caps

That strength is why markets are holding near highs.

But the composition of that growth is shifting—and the market is reacting to it.

The biggest development this quarter is the scale of AI investment:

- Hyperscaler capex is now expected to reach ~$700B+ in 2026

- AMZN → Q1 capex up +77% YoY, maintaining ~$200B annual trajectory

- GOOGL → raised capex to $180–190B, with further increases expected into 2027

- META → raised to $125–145B, adding another ~$10B

- MSFT → guiding toward ~$190B, including ~$25B in higher component costs

This is no longer incremental spending—it’s a full-scale infrastructure buildout.

At the same time, the payoff is still uneven:

- MSFT → AI revenue run rate at $37B (+123% YoY), with Azure expected to re-accelerate

- GOOGL → cloud growth +63% YoY with backlog nearly doubling, showing clear monetization

- AMZN → AWS growth re-accelerating to 28% YoY, fastest in 15 quarters

- META → strong ad growth, but stock fell on higher capex and limited visibility into AI returns

This is where the market is drawing a line:

- Companies showing clear revenue + backlog conversion are being rewarded

- Companies with rising spend and delayed payoffs are being questioned

You’re already seeing that divergence in price action:

- GOOGL +7%, AMZN +3% post-earnings

- META -9%, MSFT -2% despite strong prints

And beneath that:

- Capex is accelerating

- Free cash flow is being compressed

- Buybacks are flat

- Even “beats” are producing smaller moves

The key shift:

The market is no longer rewarding AI exposure—it’s rewarding AI efficiency and visibility.

What the Data Is Showing — Capex Surge, Buybacks Stalling

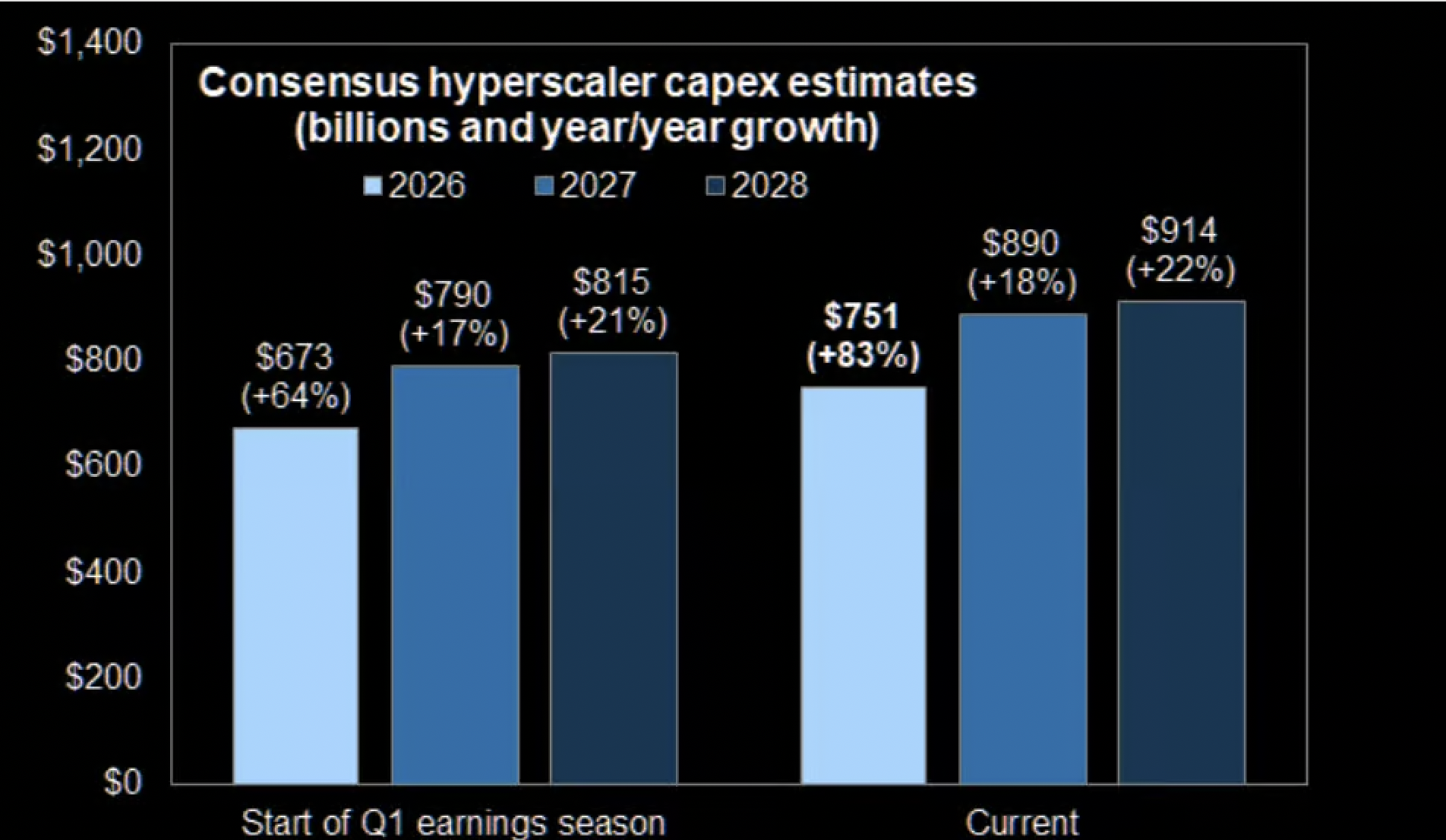

Image Above:

Consensus estimates for hyperscaler capex have moved sharply higher since the start of earnings season.

- 2026 estimates increased from ~$673B to ~$751B (+83% YoY)

- 2027 and 2028 projections were also revised higher, now approaching ~$900B+

This confirms what companies are saying:

AI spending is accelerating faster than expected—and still moving up.

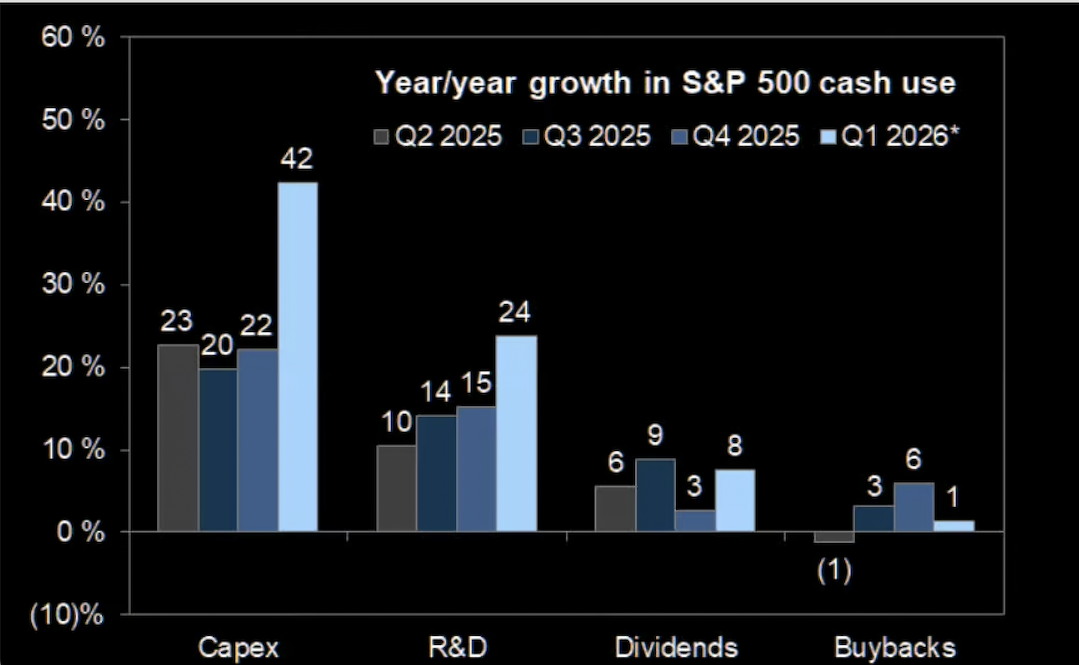

Image Below:

At the same time, how companies are using cash is shifting.

- Capex growth is now ~40%+ YoY

- R&D is also rising (~20%+)

- Buybacks are flat to down (~0–1%)

This is a clear change from prior cycles, where excess cash was returned to shareholders.

What It Means

- Companies are reinvesting aggressively instead of returning capital

- AI is driving a reallocation of cash toward infrastructure and growth

- Shareholder returns (buybacks) are no longer the primary support for stocks

This reinforces the shift: markets are moving from capital return → capital investment, which raises the bar for future returns.

Iran + Energy — Earnings Are Now Reflecting Real Constraints

The Iran conflict is no longer just lifting oil prices—it’s disrupting supply chains and day-to-day operations.

Across earnings, the message is consistent:business remains solid, but disruptions are increasing.

Energy — Strong Results, But More Difficult Conditions

Halliburton delivered solid earnings but said the conflict reduced profits slightly and lowered activity in the Middle East.

Schlumberger reported disruptions, including paused projects and weaker performance in the region as operations were scaled back.

ExxonMobil described a more volatile environment, with tighter supply and more complex logistics requiring rerouting.

Chevron performed well overall, but still saw some production slowdowns tied to the region and emphasized the uncertainty in the external environment.

Higher oil prices are supporting results, but operations are becoming less predictable.

Airlines — Fuel Costs Are Driving Changes

United Airlines remained profitable, but fuel costs increased by $340 million, leading to capacity reductions and schedule adjustments for the rest of the year.

Airlines are responding by reducing flights in some markets, adjusting schedules, and raising fares where possible.

At the same time, Spirit Airlines shut down after failing to secure financing, highlighting how quickly rising costs are affecting weaker operators.

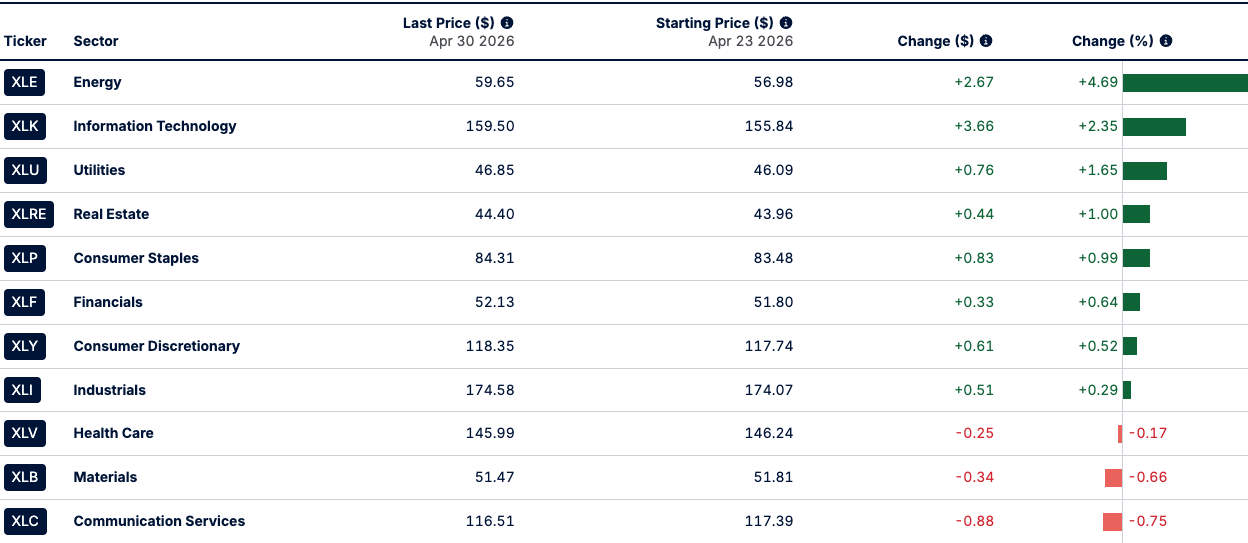

Last's Weeks Sector Winners & Losers

Sector performance last week was broadly positive, but gains were relatively contained and evenly distributed.

Leadership came from Energy (XLE +4.69%) and Technology (XLK +2.35%), with energy benefiting from higher oil prices and tech continuing to hold up on AI-driven demand.

Defensive sectors also moved higher, though more modestly, including Utilities (XLU +1.65%), Real Estate (XLRE +1.00%), and Consumer Staples (XLP +0.99%).

Cyclicals showed less conviction:

- Financials (XLF +0.64%)

- Consumer Discretionary (XLY +0.52%)

- Industrials (XLI +0.29%)

On the downside, only a few sectors finished lower:

- Communication Services (XLC -0.75%)

- Materials (XLB -0.66%)

- Health Care (XLV -0.17%)

Overall, the move reflects measured positioning rather than a strong rotation, with strength concentrated in energy and large-cap tech, while the rest of the market moved modestly in either direction.

Upcoming Events This Week

The global backdrop remains centered on the Iran conflict, with markets continuing to move in line with oil. The possibility of renewed U.S.–Iran talks will be a key driver this week, as any progress—or setback—has immediate implications for energy prices and broader risk assets.

On the data front, focus shifts to the labor market.

The April jobs report will be the headline release, with payrolls expected to slow to ~73K from 178K, while unemployment is seen holding around 4.3%. That will be reinforced by ADP, JOLTS, and productivity data, offering a clearer read on whether hiring is cooling.

At the same time, consumer sentiment remains a concern, with the Michigan survey expected to stay near lows, partly reflecting rising fuel costs tied to the Iran conflict.

Additional indicators include the ISM Services PMI, factory orders, and trade data, which will help gauge how demand is holding up under higher input costs.

Earnings remain a key driver, with a broad mix of companies reporting across sectors:

- Tech and AI: AMD, Palantir, Super Micro Computer, Arista Networks

- Consumer: McDonald’s, Disney, Uber, Kraft Heinz

- Healthcare: Pfizer, Viatris

- Financials/Global: HSBC, UniCredit

- Energy: Shell

These results will provide a more complete picture of how higher costs and shifting demand are affecting margins beyond mega-cap tech.

Globally, the macro picture broadens:

- China PMI data will give a read on industrial momentum

- Eurozone retail sales and German trade data will highlight demand trends

- Central bank decisions in Australia, Sweden, Norway, and Mexico will add to the policy backdrop

Overall, the week is less about a single catalyst and more about confirmation:

- whether labor is slowing

- whether consumers are pulling back

- and how much the energy shock is feeding into broader economic activity

Company News

LevelFields AI Stock Alerts Last Week

Five9 (FIVN) +29% — Accelerated Buyback + Capital Return Expansion

FIVN jumped ~29% in one day after announcing a $90M accelerated share repurchase to complete its existing $150M program, alongside a new $200M buyback authorization.

The move signals a clear shift toward returning capital while the company is also showing improving profitability and cash flow. The combination of stronger fundamentals and aggressive buybacks drove a sharp repricing.

Organon (OGN) +17% — Billion-Dollar Acquisition Catalyst

OGN moved ~17% following the announcement of a $11.75B acquisition deal by Sun Pharma, representing a significant premium and strategic expansion.

The transaction validates the company’s asset base and future cash flow potential, triggering a rapid revaluation as investors price in the deal terms and long-term synergies.

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai