.png)

L2 Weekly Stock Market News Analysis

May 17th, 2026

TLDR:

The Trump–Xi summit showed that the U.S. and China are attempting to stabilize tensions short term while continuing to compete aggressively around semiconductors, AI infrastructure, energy security, and industrial leadership.

Markets largely interpreted the meetings as reducing the immediate risk of a major escalation in semiconductor restrictions and broader trade tensions. That helped drive strong performance across semiconductors, AI infrastructure companies, and Chinese technology stocks with meaningful China exposure.

At the same time, many of the larger structural tensions remain unresolved.

Taiwan rhetoric intensified during the summit, semiconductor export controls remain in place, and no major breakthrough emerged around rare earth restrictions or broader tariff negotiations. The summit improved sentiment and stabilized markets short term, but it did little to resolve the longer-term geopolitical and industrial competition developing between the U.S. and China.

Sector leadership reflected this backdrop.

Technology (XLK +5.78%) and Energy (XLE +3.79%) led markets higher as investors continued rotating toward AI infrastructure, semiconductors, and geopolitical commodity exposure, while much of the broader market continued lagging beneath the surface.

The Trump–Xi Summit Shifted Focus Toward AI, Semiconductors, and Industrial Competition

The Trump–Xi summit in Beijing marked a noticeable shift in how markets are viewing the U.S.-China relationship. While the meeting produced few major trade breakthroughs, investors increasingly interpreted the summit as a signal that both countries are trying to stabilize tensions while continuing to compete aggressively around AI, semiconductors, energy security, and industrial leadership.

The summit focused heavily on technology access, AI infrastructure, semiconductor exports, and maintaining shipping flows through the Strait of Hormuz as energy markets remain under pressure. Treasury Secretary Scott Bessent confirmed the U.S. and China would begin formal AI safety discussions, while Nvidia CEO Jensen Huang joined the delegation as semiconductor policy and AI infrastructure became central themes throughout the meetings.

Huang’s attendance was especially notable given the ongoing debate surrounding Nvidia’s advanced H200 AI chips and whether China will ultimately allow broader purchases of the systems despite Washington already approving licenses earlier this year.

Markets largely interpreted the summit as reducing the risk of an immediate escalation around semiconductor restrictions and broader trade tensions. Chinese technology stocks rallied sharply throughout the week while investors rotated back into companies with meaningful China exposure.

At the same time, many of the underlying structural tensions remain unresolved.

Taiwan rhetoric intensified during the meetings, no major breakthrough emerged around Hormuz, and tariff negotiations still appear far from finalized. While Trump stated that Xi agreed the Strait of Hormuz “must remain open,” China stopped short of committing to directly pressure Tehran as oil markets, shipping routes, and global supply chains remain under strain from the conflict. The summit improved optics and stabilized sentiment short term, but it did little to resolve the larger geopolitical competition developing between the U.S. and China.

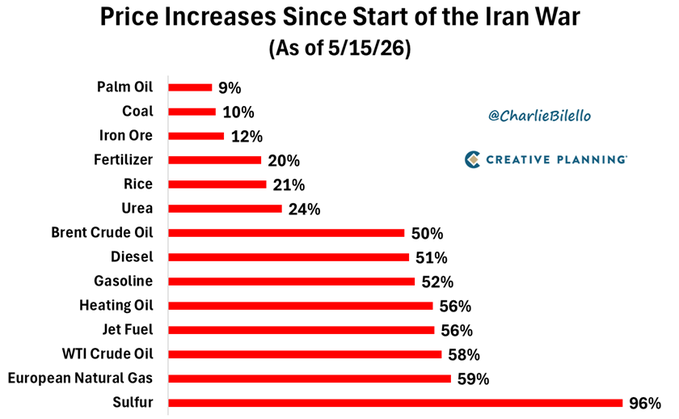

Image Above:

Notably, sulfur prices have risen more than almost any major industrial input since the start of the Iran conflict, reflecting how quickly Hormuz disruptions are spreading beyond oil markets into fertilizers, chemicals, semiconductors, and manufacturing supply chains.

That matters because sulfuric acid — the world’s most widely used industrial chemical — is critical for everything from phosphate fertilizers and petroleum refining to batteries, metals processing, clothing production, and semiconductor manufacturing. In 2025, roughly half of global sulfur supply came from the Middle East. China, one of the world’s largest sulfuric acid exporters, has already moved to restrict exports to protect domestic supply as regional trade and shipping flows remain disrupted.

The result is that U.S.-China cooperation around Iran and Hormuz is becoming increasingly important not just for oil prices, but for broader industrial and manufacturing stability globally.

Potential beneficiaries if sulfur shortages persist could include:

- Mosaic (MOS)

- Nutrien (NTR)

- CF Industries (CF)

Winners and Losers From The Summit

Semiconductor and AI infrastructure companies emerged as some of the clearest winners from the summit as markets increasingly priced in a more stable near-term U.S.-China trade backdrop.

The biggest beneficiaries remained companies tied to AI compute, semiconductors, and cloud infrastructure, particularly those with meaningful China revenue exposure.

Key beneficiaries included:

- Nvidia (NVDA)

- AMD (AMD)

- Broadcom (AVGO)

- Taiwan Semiconductor (TSM)

- Qualcomm (QCOM)

- ASML (ASML)

The rally reflected investor optimism that both countries are attempting to avoid a full technology decoupling despite ongoing strategic competition around AI and semiconductors.

At the same time, major uncertainties remain unresolved.

No major breakthrough emerged surrounding Nvidia’s H200 AI chip exports. While some licensing approvals had already been granted prior to the summit, semiconductor export controls remain a major sticking point between both countries and continue creating uncertainty around long-term AI chip access inside China.

Visa (V) also benefited after Trump publicly pushed for broader access to China’s payments market, which remains one of the world’s largest untapped financial networks.

Agriculture and energy-related companies also moved higher after reports that China could significantly expand purchases of U.S. soybeans, beef, agricultural products, and potentially energy exports as part of broader trade stabilization efforts.

Potential beneficiaries include:

- Deere (DE)

- Archer Daniels Midland (ADM)

- Bunge (BG)

- CF Industries (CF)

- Cheniere Energy (LNG)

Chinese internet and technology companies also rallied sharply as investors rotated back into underowned China exposure.

Key beneficiaries included:

- Alibaba (BABA)

- JD.com (JD)

- Tencent (TCEHY)

- Baidu (BIDU)

- PDD Holdings (PDD)

These companies benefited from improving diplomatic rhetoric, lighter positioning, and renewed investor appetite for Chinese AI, cloud, and technology exposure.

Meanwhile, Boeing (BA) underwhelmed expectations.

Investors had anticipated a significantly larger aircraft order announcement during the summit, but China reportedly committed to roughly 200 planes initially — below the more optimistic expectations heading into the meetings.

Rare earth restrictions also remained unresolved.

China did not announce any easing of export controls on rare earth materials, which continue affecting portions of the semiconductor, aerospace, EV, and defense supply chains. That remains a lingering vulnerability for U.S. manufacturers dependent on Chinese rare earth processing and refining capacity.

If tensions persist and no broader rare earth agreement is reached, potential beneficiaries could include:

- USA Rare Earth (USAR)

- U.S. Antimony (UAMY)

- MP Materials (MP)

- Energy Fuels (UUUU)

- NioCorp (NB)

Taiwan-related geopolitical risk also remained a lingering overhang for global supply chains and semiconductor manufacturing.

Areas that remain exposed include:

- Apple (AAPL)

- Consumer electronics manufacturers such as Dell (DELL) and HP (HPQ)

- Global semiconductor supply chains including Applied Materials (AMAT) and Lam Research (LRCX)

- Taiwan-linked exporters and assemblers such as Foxconn/Hon Hai Precision and Quanta Computer

Defense contractors could also see increased volatility as geopolitical tensions remain elevated, including:

- Lockheed Martin (LMT)

- RTX (RTX)

- Northrop Grumman (NOC)

Chinese Equities Rally As AI and Consumption Trends Improve

Chinese equities were among the strongest-performing global markets last week as investors aggressively rotated back into internet and technology names following the Trump–Xi summit.

The rally was supported by improving U.S.-China rhetoric, lighter investor positioning, and growing investor belief that China may be entering a new phase centered around AI infrastructure, cloud growth, and technology investment rather than purely property weakness and macro slowdown concerns.

Importantly, positioning across Chinese equities had become extremely light prior to the move.

That matters because many investors had heavily reduced exposure to China due to years of regulatory pressure, weak economic growth, and geopolitical tensions. When sentiment began improving following the Trump–Xi summit, investors who were underexposed were forced to rotate back into the trade quickly — helping amplify the rally across Chinese technology stocks and ETFs like KWEB.

KWEB — one of the largest ETFs tracking Chinese internet and technology companies including Alibaba, Tencent, JD.com, Baidu, and PDD — broke above major technical resistance levels last week as investors rushed back into underowned China technology exposure. ChiNext, China’s growth and technology-heavy index, also continued breaking into a stronger technical regime.

The broader setup increasingly resembles a positioning-driven catch-up trade.

While U.S. AI and technology stocks have dominated global performance over the past two years, many Chinese technology companies had been left behind due to concerns surrounding regulation, geopolitics, weak consumer demand, and slowing economic growth.

That dynamic may now be starting to shift.

Alibaba (BABA) reinforced the idea that China’s AI investment cycle is accelerating rapidly.

Cloud Intelligence revenue rose 38% year-over-year while external cloud revenue accelerated 40%, driven heavily by AI demand and adoption of Alibaba’s Qwen model ecosystem. AI-related cloud revenue has now posted triple-digit growth for eleven consecutive quarters.

More importantly for the broader China trade, Alibaba’s earnings showed that Chinese technology firms are increasingly positioning themselves around:

- AI infrastructure

- cloud computing

- enterprise AI adoption

- automation

- logistics efficiency

- ecosystem integration

rather than relying solely on low-margin consumer growth.

JD.com (JD) reinforced a similar trend.

While the company still showed stabilizing consumer activity, management focused heavily on logistics automation, robotics, food delivery expansion, and broader supply-chain infrastructure investment rather than simply retail demand alone.

That shift matters because investors are increasingly beginning to view parts of Chinese technology less as purely cyclical consumer trades and more as long-duration AI and infrastructure assets tied to cloud, logistics, and industrial automation growth.

The strongest beneficiaries of that rotation last week included:

- Alibaba (BABA)

- JD.com (JD)

- Tencent (TCEHY)

- Baidu (BIDU)

- PDD Holdings (PDD)

- KWEB

as capital rotated back into Chinese technology exposure following the summit.

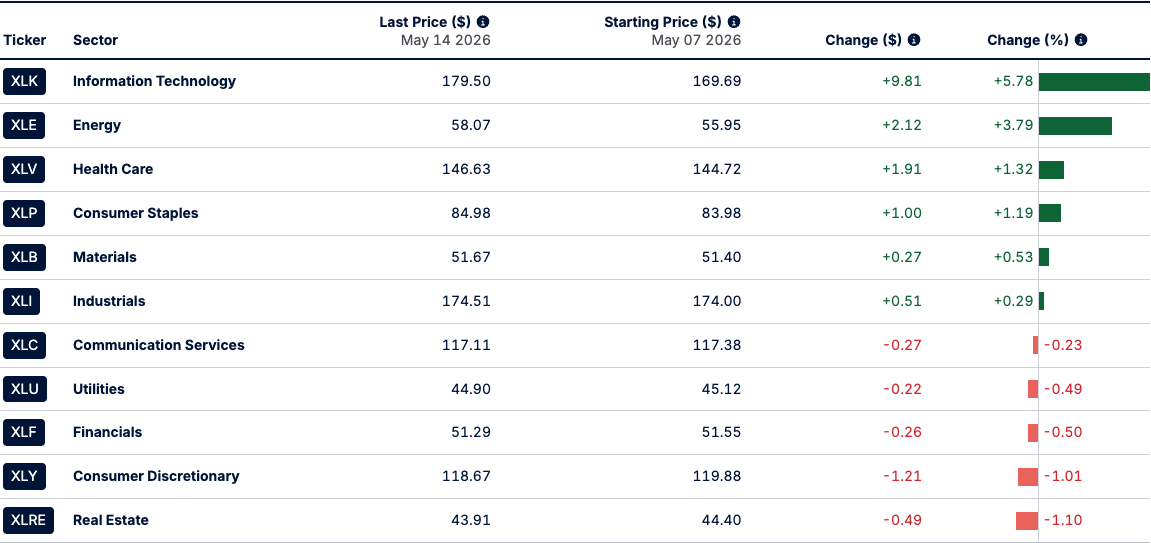

Last's Weeks Sector Winners & Losers

Sector performance last week reflected a concentrated rally led primarily by technology and energy as investors continued rotating toward AI infrastructure, semiconductors, and geopolitical commodity exposure.

Leadership came from:

- Technology (XLK +5.78%)

- Energy (XLE +3.79%)

Technology outperformed as investors continued crowding into AI-linked semiconductors, hyperscalers, and cloud infrastructure names following the Trump–Xi summit and continued AI spending optimism.

Energy also remained strong as oil markets stayed elevated amid ongoing Iran and Hormuz-related supply concerns.

Defensive sectors posted smaller gains, including:

- Health Care (XLV +1.32%)

- Consumer Staples (XLP +1.19%)

Meanwhile, several sectors finished negative:

- Real Estate (XLRE -1.10%)

- Consumer Discretionary (XLY -1.01%)

- Financials (XLF -0.50%)

- Utilities (XLU -0.49%)

- Communication Services (XLC -0.23%)

Overall, the move reinforced that market leadership remains heavily concentrated in AI infrastructure and energy-related names while much of the broader market continues lagging beneath the surface.

Upcoming Events This Week

Markets will remain heavily focused on the Iran conflict and any signs of either escalation or renewed diplomacy between the U.S. and Tehran as oil prices, shipping routes, and broader risk sentiment continue moving closely alongside developments surrounding the Strait of Hormuz.

At the same time, investors will closely watch the latest Fed meeting minutes following the unusually divided FOMC decision that saw three dissents. After hotter-than-expected CPI and PPI data, markets will be looking for further clues around the Fed’s willingness to keep rates elevated despite slowing growth concerns.

Economic data this week will center heavily around leading indicators, including:

- Flash PMI data

- Philadelphia Fed Manufacturing Index

- Michigan Consumer Sentiment

- Housing starts and permits

- Pending home sales

The data will help determine whether economic activity is continuing to soften beneath the surface as higher energy prices and elevated rates pressure consumers and manufacturing activity.

Earnings will also remain a major focus.

Key companies reporting include:

- Nvidia (NVDA)

- Walmart (WMT)

- Home Depot (HD)

- Analog Devices (ADI)

- Deere (DE)

- Lowe’s (LOW)

Nvidia’s report will likely be the biggest event of the week as investors continue watching whether AI spending remains strong enough to justify the ongoing rally across semiconductors and infrastructure names.

Globally, investors will also monitor China industrial production and retail sales data, Japan Q1 GDP, Eurozone flash PMIs, and UK inflation and retail sales figures.

Overall, the week remains centered on whether growth is slowing fast enough to pressure the Fed while geopolitical tensions continue driving inflation, commodity volatility, and supply-chain uncertainty.

Company News

LevelFields AI Stock Alerts Last Week

Jiuzi Holdings (JZXN) +48% — Digital Asset Gains + Share Buyback Catalyst

JZXN surged 48% in one day after announcing $210,000 in realized gains tied to its Distributed Capital Intelligence Protocol (DCIP) investment alongside approval of a new share repurchase program. Management framed the move as validation of its digital asset treasury strategy and broader blockchain-focused capital allocation framework.

The rally reflected continued speculative appetite surrounding small-cap companies tying balance sheet strategy, crypto exposure, and buybacks together as liquidity conditions improve.

PACS Group (PACS) +29% — Earnings Beat + $250M Buyback Authorization

PACS jumped 29% in one day after reporting significantly stronger-than-expected earnings and approving a massive $250 million share repurchase authorization. Revenue rose 11.2% year-over-year while adjusted EBITDA surged nearly 75% as occupancy, skilled nursing mix, and operating margins continued improving.

The combination of accelerating profitability, raised full-year guidance, strong cash flow generation, and aggressive capital returns triggered a sharp repricing higher across the stock.

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai