.png)

L2 Weekly Stock Market News Analysis

May 25th, 2026

TLDR:

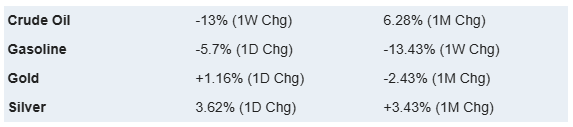

Over the weekend, progress in U.S.–Iran negotiations and improving shipping flows through the Strait of Hormuz triggered a major relief rally across global markets. Brent crude plunged more than 6% Monday as traders rapidly unwound fears of a prolonged energy shock.

Meanwhile, bond markets continued sending a much more cautious message underneath the surface.

The 10-year Treasury yield, which climbed above 4.5% more than a week ago for the first time since 2007, remained elevated as investors increasingly focused on persistent inflation, record government debt issuance, military spending, and massive AI-related infrastructure investment pushing borrowing costs higher.

That AI buildout remains one of the dominant themes underneath the market, reinforced again this week after Nvidia (NVDA) reported another massive quarter. Revenue surged 85% YoY while management stated that AI infrastructure spending could eventually reach $3–4 trillion annually as governments, enterprises, and industrial companies continue accelerating investments into data centers, semiconductors, power generation, networking, and grid expansion.

Sector performance reflected that tension last week. Utilities (XLU +3.37%), Health Care (XLV +3.30%), and Real Estate (XLRE +3.08%) led markets as investors rotated toward defensive and rate-sensitive sectors, while Technology (XLK +2.34%) continued outperforming on ongoing AI momentum. Meanwhile, Energy (XLE +0.08%) sharply lagged after oil prices collapsed following optimism surrounding Iran negotiations.

Looking ahead, investors will remain focused on Middle East developments, Treasury yields, and inflation data — particularly the Fed’s preferred inflation gauge (PCE) — as markets continue debating whether inflation pressures are beginning to stabilize or remain structurally elevated underneath the surface.

Iran Talks Trigger Massive Relief Rally As Oil Collapses

Markets entered the final trading week of May increasingly pricing in the possibility that the worst phase of the Iran conflict may be easing.

Over the weekend, U.S. and Iranian officials reportedly made progress toward a potential framework agreement that could eventually reopen the Strait of Hormuz and de-escalate the conflict. Iranian officials acknowledged that consensus had been reached on several major issues, though they cautioned that a finalized agreement was “not imminent.” At the same time, tanker traffic through Hormuz began gradually improving, with several LNG vessels successfully passing through the region.

Markets immediately reacted as if the worst-case oil shock scenario was beginning to fade.

Brent crude plunged more than 6% Monday as traders rapidly unwound the geopolitical risk premium that had built throughout the conflict. European natural gas prices also moved sharply lower while global equities rallied, particularly across semiconductors, AI infrastructure, and technology names that had previously been pressured by fears of a prolonged energy and inflation shock.

Still, many of the larger structural risks remain unresolved.

The U.S. naval presence around Hormuz remains active, negotiations surrounding uranium enrichment and sanctions remain unresolved, and Iran continues discussing long-term transit toll structures for vessels crossing the Strait. While shipping conditions have improved, markets increasingly appear to be treating the situation as a temporary stabilization rather than a fully resolved geopolitical breakthrough.

Yields Spike As Markets Reprice Inflation, AI Spending, and The New Fed Era

While oil prices collapsed Monday, bond markets are sending a much more cautious message underneath the surface.

Treasury yields surged throughout last week as investors increasingly questioned whether inflation pressures may remain elevated longer than markets had previously expected. The 10-year Treasury yield climbed above 4.5% — its highest level since 2007 — as markets reassessed the combination of persistent inflation, large fiscal deficits, and massive AI-driven capital spending.

Meanwhile, Kevin Warsh was officially sworn in as Federal Reserve chairman — a notable development because many investors had previously viewed him as potentially more dovish than the current Fed leadership. Despite that expectation, odds of a 2026 Fed rate hike spiked to nearly 46%.

The image below highlights how unusual the current environment is historically. Kevin Warsh entered office with the highest 10-year Treasury yield of any Fed chair since Ben Bernanke in 2006 and one of the highest starting yield environments of the modern Fed era, reflecting how much more inflation and borrowing-cost pressure markets are facing today compared to the ultra-low-rate environment of the 2010s.

Importantly, yields were not rising just because of oil.

Markets are increasingly worried that several large forces are all pushing borrowing costs higher simultaneously:

- Massive AI infrastructure spending

- Record government debt issuance

- Persistent fiscal deficits

- Continued military and defense spending

- A resilient economy despite higher energy prices

- Reshoring, tariffs, and infrastructure-related supply-chain costs

Normally, falling oil prices would help ease inflation concerns and lower pressure on interest rates. If the Strait of Hormuz fully reopens and oil prices keep falling, that could help ease some inflation fears and potentially bring yields lower as well. However, investors may increasingly be focusing on the possibility that borrowing costs could remain elevated even if the immediate Iran-related energy shock fades because several other structural forces are still pushing yields higher underneath the surface.

Part of that shift is tied directly to the AI investment boom itself.

Hyperscalers, utilities, and governments are simultaneously pouring enormous amounts of capital into data centers, semiconductors, power generation, and grid expansion. That spending is supporting economic growth, but it is also increasing demand for financing across the economy at the same time governments are issuing record amounts of debt.

If Treasury yields remain elevated, financing costs across infrastructure, commercial real estate, and leveraged growth sectors could continue rising, potentially making large AI and industrial projects more expensive to fund moving forward.

Higher yields matter because they raise borrowing costs across the economy — from mortgages and auto loans to commercial real estate and corporate debt — while also pressuring expensive, high-valuation growth stocks.

The result is an increasingly unusual setup where equities continue rallying around AI while bond markets remain far more cautious underneath the surface.

Market Implications

Areas that could face pressure if yields continue rising include:

- Utilities (XLU) — higher financing costs pressure dividend-focused sectors

- Real Estate (XLRE) — commercial and residential property financing becomes more expensive

- Consumer discretionary companies — higher credit-card and auto-loan costs can weaken spending

- Smaller speculative technology companies — many rely heavily on cheap financing and future growth expectations

- Highly leveraged infrastructure and private-equity financing structures — refinancing becomes more expensive

- Long-duration software and AI names trading at elevated multiples — valuations become harder to justify as rates stay high

Last's Weeks Sector Winners & Losers

Sector performance shifted this week as markets rotated back toward defensive and rate-sensitive sectors while technology continued grinding higher underneath the surface.

Utilities (XLU +3.37%) led the market alongside Health Care (XLV +3.30%) and Real Estate (XLRE +3.08%) as investors favored more stable cash-flow sectors amid rising geopolitical and rate uncertainty.

Technology (XLK +2.34%) also remained strong, supported by continued AI infrastructure momentum across semiconductors, data centers, and hyperscaler spending.

Consumer Discretionary (XLY +2.27%) and Financials (XLF +1.64%) finished higher as investors continued betting on resilient consumer spending and elevated financing activity.

Meanwhile, cyclical sectors lagged. Energy (XLE +0.08%) sharply underperformed after oil prices collapsed Monday following optimism surrounding Iran negotiations and improving shipping flows through the Strait of Hormuz. Materials (XLB -0.02%) and Communication Services (XLC -0.53%) were the weakest sectors overall.

Overall, leadership remained relatively narrow, with investors continuing to crowd into AI, defensive positioning, and large-cap quality names while many cyclical sectors struggled to sustain momentum underneath the surface.

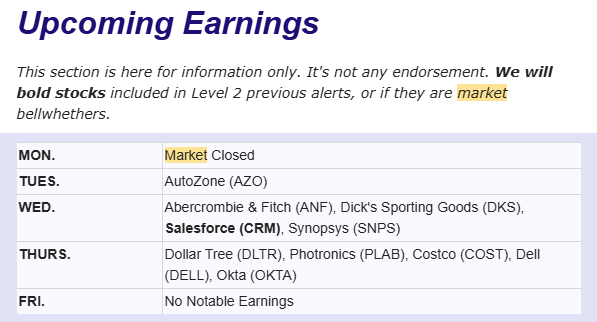

Upcoming Events This Week

Headlines surrounding the Middle East and progress toward restoring energy exports through the Strait of Hormuz will continue driving global markets this week. Investors are increasingly balancing two competing forces: strong earnings and AI-driven capital spending versus the inflationary impact of the war and elevated energy prices.

Inflation will remain the primary macro focus.

In the United States, markets will closely watch the personal income and outlays report, which includes the Fed’s preferred inflation gauge — the PCE price index. Investors will also monitor durable goods orders, the second estimate of Q1 GDP, manufacturing surveys, and housing data for signs that higher energy costs and elevated interest rates are beginning to pressure economic activity more broadly.

At the same time, markets will continue parsing speeches from Federal Reserve officials following Kevin Warsh’s swearing-in as Fed chairman, especially as investors debate whether elevated inflation and rising yields could delay future rate cuts.

Company News

LevelFields AI Stock Alerts Last Week

Bio-Rad Laboratories (BIO) +13.8% — Elliott Stake Sparks Activist Repricing

Bio-Rad Laboratories surged roughly 13.8% in one day after reports emerged that activist investor Elliott Management had built a significant stake in the life-science tools supplier.

The move fueled investor optimism that Elliott could push for operational changes, cost reductions, capital returns, or strategic restructuring efforts aimed at unlocking value after years of underperformance relative to peers in the life-sciences and diagnostics sector.

The rally also highlighted a broader trend developing across healthcare and industrial companies where activist investors are increasingly targeting firms with valuable assets, strong cash flow generation, or depressed valuations following the recent market volatility and higher-rate environment.

Other Company News

Nvidia Earnings Reinforce That AI Infrastructure Spending Is Still Accelerating

Nvidia (NVDA) once again delivered massive results that reinforced just how aggressively the global AI infrastructure buildout continues accelerating.

Revenue surged 85% YoY to a record $81.6 billion while Data Center revenue jumped 92% YoY to $75.2 billion. Nvidia also guided next-quarter revenue to roughly $91 billion, announced an additional $80 billion buyback authorization, and raised its quarterly dividend from $0.01 to $0.25 per share.

More importantly, the earnings call made clear that AI spending is no longer limited to just a handful of hyperscalers.

Management repeatedly emphasized that demand is now expanding across:

- Sovereign AI projects

- Enterprise AI infrastructure

- Industrial AI factories

- Robotics

- Autonomous vehicles

- AI cloud providers

- Telecommunications infrastructure

- Physical AI systems

Nvidia stated that AI infrastructure spending could eventually reach $3–4 trillion annually by the end of the decade as governments, enterprises, and industrial companies increasingly build their own AI systems.

The company also highlighted several developments that reinforced how broad the AI buildout is becoming:

- Networking revenue nearly tripled YoY to $14.8 billion

- AI cloud revenue more than tripled YoY

- Sovereign AI revenue rose over 80% YoY

- The number of AI data centers exceeding 10 megawatts nearly doubled in one year

- Nvidia said it now has visibility into nearly $20 billion of CPU revenue this year alone

Jensen Huang repeatedly described AI factories as “the largest infrastructure expansion in human history.”

Importantly, Nvidia also said it expects to remain supply constrained throughout the entire life cycle of its upcoming Vera Rubin chip platform, suggesting demand still exceeds available supply even after years of massive capacity expansion.

What Nvidia’s Earnings Potentially Mean For Other Stocks

The earnings continue reinforcing several themes we have been discussing for months:

Potential Beneficiaries

AI Infrastructure / Electrical Buildout

- Vertiv (VRT) — cooling and power systems for AI data centers

- Eaton (ETN) — electrical equipment and grid infrastructure

- Quanta Services (PWR) — transmission and electrical buildout

- EMCOR (EME) — mission-critical electrical construction

- Constellation Energy (CEG) — power demand tied to AI infrastructure

- Vistra (VST) — electricity demand growth from hyperscalers

- Bloom Energy (BE) — on-site power systems for AI facilities

Nvidia’s comments reinforced that power and infrastructure constraints remain one of the largest bottlenecks for AI expansion.

Networking / Optical Infrastructure

- Broadcom (AVGO)

- Marvell (MRVL)

- Arista Networks (ANET)

- Lumentum (LITE)

- Coherent (COHR)

Networking revenue nearly tripled YoY, reinforcing that AI is not just a GPU story anymore. Optical networking, high-speed connectivity, and AI data-transfer infrastructure continue becoming larger bottlenecks as compute clusters scale.

Semiconductor Manufacturing / Equipment

- Taiwan Semiconductor (TSM)

- Applied Materials (AMAT)

- Lam Research (LRCX)

- KLA (KLAC)

- ASML (ASML)

Nvidia’s guidance continues signaling that semiconductor manufacturing demand remains elevated across advanced packaging, lithography, and AI chip production.

Robotics / Physical AI

One of the more important long-term takeaways from the call was Nvidia’s growing emphasis on “physical AI,” robotics, industrial automation, and autonomous systems.

Potential beneficiaries include:

- Tesla (TSLA)

- Rockwell Automation (ROK)

- ABB

- Symbotic (SYM)

- Zebra Technologies (ZBRA)

Management repeatedly emphasized that the next major AI wave may extend beyond chatbots and hyperscalers into factories, logistics, robotics, and industrial automation.

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai