.png)

L2 Weekly Stock Market News Analysis

July 5th, 2026

TLDR:

The biggest macro story last week wasn't another Federal Reserve meeting—it was a surprisingly weak June jobs report. The U.S. economy added just 57,000 jobs, roughly half of expectations, while payroll gains for April and May were revised sharply lower. The report eased fears that Chairman Kevin Warsh would need to raise interest rates again immediately, with markets lowering the probability of another hike later this year.

That doesn't mean the Fed is finished. Warsh continues to emphasize inflation as his primary concern, arguing that price stability remains the central objective even as labor markets soften. In other words, weaker employment alone is unlikely to trigger easier monetary policy if inflation remains stubbornly high.

Markets now turn their attention to the ISM Services PMI, which will provide another snapshot of the U.S. economy, while PepsiCo's earnings should offer insight into consumer spending and Delta Air Lines may provide clues on travel demand and energy costs following last month's Middle East disruptions. Earnings season also begins ramping up this week, marking the next major catalyst for equities after several weeks dominated by macroeconomic headlines.

Meanwhile, market leadership continued to broaden. Health Care (+4.04%) led the market for a second straight week, while Communication Services, Consumer Discretionary, Financials, Industrials, and Technology all finished higher. At the same time, investors rotated out of defensive sectors such as Utilities, Energy, Consumer Staples, and Real Estate, suggesting confidence is expanding beyond a handful of AI leaders into a healthier, more balanced rally.

While interest rates remain important, the bigger story unfolding may be where the AI investment cycle goes next.

Is The AI Business Model About To Change?

For nearly three years, the AI investment thesis has been remarkably simple: build larger models, sell more tokens, and continue expanding compute capacity. Last week, however, Palantir CEO Alex Karp publicly challenged that framework, arguing that many frontier AI companies have built business models that benefit the AI labs far more than the enterprises paying for them.

Karp claimed that executives across corporate America are becoming increasingly frustrated because they are spending millions of dollars on token-based AI services without seeing measurable economic value in return. Rather than charging customers based on the business outcomes they generate, he questioned why AI providers continue monetizing primarily through token consumption and compute usage.

His argument centered on a simple question: if an AI system truly generates billions of dollars in value for its customers, why is it priced by the token instead of taking a percentage of the value it creates? In Karp's view, pricing based on compute rather than results suggests companies are paying primarily for access to infrastructure rather than guaranteed productivity gains.

Karp also raised broader concerns about intellectual property. He argued that enterprises increasingly rely on frontier AI models to analyze internal documents, workflows, customer information, and proprietary business processes. While major AI providers publish policies describing how enterprise data is handled, Karp warned that many executives remain concerned about whether sharing increasingly valuable operational knowledge with external AI providers could eventually weaken their own competitive advantages. According to Karp, many CEOs privately worry they are transferring some of their organization's "alpha"—the unique knowledge, processes, and expertise that differentiate their businesses—to outside AI platforms.

His broader point extends beyond privacy. Karp believes the next phase of enterprise AI will be determined not by who builds the largest foundation model, but by who can securely deploy AI inside organizations while protecting proprietary data and delivering measurable business outcomes. That philosophy has largely shaped Palantir's own strategy, which focuses on private deployments, enterprise-specific AI agents, and keeping sensitive operational data under customer control rather than relying exclusively on public frontier models.

Whether investors ultimately agree with Karp or not, his comments reflect a broader debate beginning to emerge across corporate America. The first phase of the AI boom rewarded companies for building increasingly powerful models. The next phase may increasingly reward companies that can demonstrate tangible returns on investment, protect enterprise data, and apply AI directly to real-world business operations.

That shift helps explain why investor attention is gradually expanding beyond large language models toward physical AI, robotics, industrial automation, and other applications where the economic benefits are easier to measure.

Why Now?

Just a few years ago, humanoid robots largely belonged to science fiction. The hardware was expensive, artificial intelligence struggled to understand the physical world, and the economics simply weren't compelling enough for widespread adoption.

That is beginning to change.

The same breakthroughs that transformed generative AI are now being applied to robotics. New Vision-Language-Action (VLA) models allow robots to interpret natural language, recognize objects, and perform increasingly complex physical tasks without requiring engineers to program every movement individually. At the same time, advances in simulation, teleoperation, and real-world data collection have dramatically reduced the cost of training robots—from roughly $340 per hour in early 2024 to approximately $118 today according to SVRC Research. Improvements in batteries, sensors, onboard computing, and open robotics software have also accelerated development while driving costs steadily lower.

Perhaps most importantly, companies no longer need humanoid robots to replace entire workforces to justify the investment. They only need robots capable of performing repetitive, labor-intensive tasks reliably enough to generate an attractive return on investment. That threshold is beginning to come into view for warehouses, manufacturing plants, semiconductor facilities, and logistics centers.

Morgan Stanley estimates the humanoid robotics market could ultimately reach $7.5 trillion by 2050, while SVRC Research expects commercial deployments to begin accelerating over the next several years as hardware costs continue falling and AI capabilities improve.

Why Humanoid Robots Matter

Industrial robots have existed for decades, but they've traditionally been designed to perform one repetitive task inside carefully engineered environments. Humanoid robots represent a fundamentally different approach.

Instead of redesigning factories around machines, companies are building machines capable of working inside environments already designed for humans. Warehouses, hospitals, factories, restaurants, and retail stores were all built for people. A robot with two arms, two legs, and human-like dexterity can theoretically perform many of those same tasks without requiring companies to rebuild their facilities.

The first commercial deployments are expectedto focus on industries facing persistent labor shortages and repetitive workflows. Logistics and warehousing remain the largest opportunity today, followed by automotive manufacturing, semiconductor production, healthcare support, food service, and retail operations.

Rather than replacing every worker, the first generation of humanoids will likely augment human labor by handling repetitive lifting, transporting materials, stocking shelves, operating equipment, cleaning facilities, and performing inspection tasks. The long-term opportunity extends much further, but enterprise deployments are expected to drive adoption well before consumer robots become commonplace.

The Companies Building The Robot Economy

Unlike the early AI boom, where investors largely focused on software developers and semiconductor companies, the robotics ecosystem spans nearly every part of the industrial economy. While many of the leading humanoid companies remain private, dozens of publicly traded companies already supply the chips, sensors, motors, software, and automation systems that make these robots possible.

Humanoid Robot Developers

- Tesla (NASDAQ: TSLA) – Optimus

- Figure AI (Private)

- Agility Robotics (Private) – Digit

- Apptronik (Private) – Apollo

- Boston Dynamics (Private / Hyundai)

- Physical Intelligence (Private)

- 1X Technologies (Private)

- Skild AI (Private)

These companies are building the humanoid platforms themselves, competing to become the operating system for physical AI.

AI Models & Compute

- NVIDIA (NASDAQ: NVDA) – Jetson, Isaac Sim, GR00T robotics platform

- Alphabet (NASDAQ: GOOGL) – Gemini Robotics / DeepMind

- Microsoft (NASDAQ: MSFT) – Azure AI infrastructure & OpenAI partner

- Meta (NASDAQ: META) – AI foundation models

- OpenAI (Private)

- Qualcomm (NASDAQ: QCOM) – Edge AI processors

- AMD (NASDAQ: AMD) – AI compute

- Intel (NASDAQ: INTC) – Robotics processors

These companies provide the AI models, simulation software, and onboard computing that allow robots to perceive their surroundings, understand language, and make decisions autonomously.

Vision, Sensors & Perception

- Ambarella (NASDAQ: AMBA) – AI vision processors

- Luminar (NASDAQ: LAZR) – LiDAR

- Ouster (NYSE: OUST) – Digital LiDAR

- Cepton (NASDAQ: CPTN) – LiDAR

- MicroVision (NASDAQ: MVIS) – LiDAR & perception

- Hesai (NASDAQ: HSAI) – LiDAR

- RoboSense (HK Listed)

These companies provide the cameras, LiDAR, depth sensing, and perception systems that allow robots to navigate and interact with the physical world.

Warehouse & Logistics Automation

- Amazon (NASDAQ: AMZN)

- Symbotic (NASDAQ: SYM)

- GXO Logistics (NYSE: GXO)

- FedEx (NYSE: FDX)

Warehouses are expected to become one of the earliest large-scale deployment markets. Amazon and GXO are already piloting humanoid robots, while Symbotic continues expanding AI-powered warehouse automation that could eventually integrate humanoid platforms alongside its existing autonomous systems.

Automotive Manufacturing

- Tesla (NASDAQ: TSLA)

- General Motors (NYSE: GM)

- Ford (NYSE: F)

- BMW

- Mercedes-Benz

- Toyota

Automotive factories provide one of the clearest early use cases, where humanoids can perform repetitive assembly, inspection, material handling, and logistics tasks alongside existing workers.

Industrial Automation & Motion Control

- Rockwell Automation (NYSE: ROK)

- Regal Rexnord (NYSE: RRX)

- Parker-Hannifin (NYSE: PH)

- Emerson Electric (NYSE: EMR)

- Honeywell (NASDAQ: HON)

- ABB (NYSE: ABB)

These companies manufacture industrial motors, motion control systems, drives, encoders, actuators, and factory automation equipment that form much of a humanoid robot's mechanical backbone.

Precision Components

- Timken (NYSE: TKR) – Bearings

- Novanta (NASDAQ: NOVT) – Encoders, precision motion, sensors

- Sensata Technologies (NYSE: ST) – Position & torque sensors

- ATI Industrial Automation (Private)

Bearings, encoders, force sensors, and precision motion components allow robots to move accurately and safely while interacting with people and objects.

Batteries & Power Systems

- Panasonic

- Samsung SDI

- CATL

- LG Energy Solution

Battery technology determines runtime, charging speed, and overall deployment economics for mobile humanoid robots.

The Material Bottleneck

- MP Materials (NYSE: MP)

- Energy Fuels (NYSE American: UUUU) (Rare earth processing expansion)

- Lynas Rare Earths (ASX: LYC)

Rare earth magnets are essential for electric motors, actuators, and precision movement. As humanoid production scales, domestic rare earth supply chains are expected to become increasingly strategic as the U.S. works to reduce dependence on China.

The U.S. And China Are Racing Toward The Same Goal

Humanoid robotics is rapidly becoming more than just another technology trend—it's emerging as a strategic competition between the United States and China.

The United States currently leads in AI models, robotics software, and foundation model development through companies like NVIDIA, OpenAI, Tesla, Figure AI, Agility Robotics, and Apptronik. China, however, maintains a significant advantage in manufacturing scale, batteries, rare earth processing, precision actuators, and many of the mechanical components that ultimately determine how quickly robots can be produced and at what cost.

Morgan Stanley expects China's humanoid robot shipments to grow at an 85% annual rate through 2030, supported by roughly $27 billion in government funding and an established manufacturing ecosystem built during the electric vehicle boom. That cost advantage has already allowed companies like Unitree to introduce humanoid robots at a fraction of Western prices.

For investors, this means the robotics opportunity extends well beyond the companies building humanoids themselves. The winners are likely to include manufacturers supplying motors, sensors, batteries, rare earth materials, industrial automation, and AI chips—the critical components every robot requires regardless of which platform ultimately dominates.

The Next AI Bottleneck

The first phase of the AI boom was constrained by GPUs, memory chips, networking equipment, and power. The next phase may be constrained by physical hardware.

As humanoid robots move from prototypes to commercial deployment, researchers expect actuators, precision reducers, rare earth magnets, batteries, sensors, and high-quality training data to become the industry's biggest bottlenecks. China currently dominates much of this supply chain, while the United States maintains an edge in AI software and robotics development.

Just as internet-scale data became the foundation of today's AI models, real-world robotic data may become the industry's most valuable asset. The companies that deploy robots at scale won't just automate work—they'll continuously improve their AI, creating a powerful competitive advantage that compounds over time.

Last's Weeks Sector Winners & Losers

Sector leadership broadened last week as investors continued rotating beyond the narrow group of AI infrastructure winners that dominated the first half of the year. Health Care (XLV +4.04%) led the market for a second consecutive week, followed by Communication Services (XLC +3.00%), Consumer Discretionary (XLY +2.62%), Financials (XLF +1.97%), and Industrials (XLI +1.75%). Information Technology (XLK +1.40%) also finished higher, suggesting investors remain constructive on AI despite broadening participation across the market.

The weakest sectors were Utilities (XLU -1.69%), Energy (XLE -1.42%), Consumer Staples (XLP -1.35%), Real Estate (XLRE -0.74%), and Materials (XLB -0.27%), as investors rotated out of many of the defensive areas that had outperformed during the recent bout of market uncertainty.

The week's performance suggests the market is becoming increasingly balanced. Rather than relying solely on a handful of AI leaders, investors appear to be expanding exposure into cyclical sectors such as Industrials, Financials, and Consumer Discretionary while continuing to maintain confidence in long-term AI-driven growth. This broader participation is generally viewed as a healthier backdrop than a rally driven by only a small number of mega-cap technology stocks.

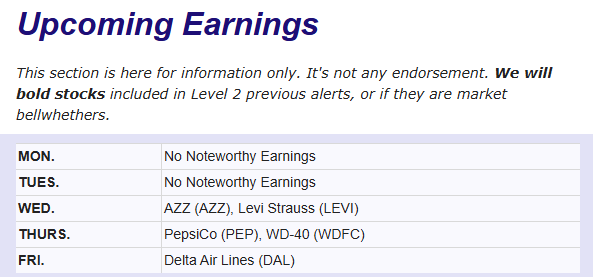

Upcoming Events This Week

Markets will shift their focus back to monetary policy this week as investors look for clues on the Federal Reserve's next move following the weaker-than-expected June jobs report. The Fed's June meeting minutes will headline the week, offering insight into how policymakers are balancing persistent inflation against signs of a cooling labor market.

Other key U.S. releases include the ISM Services PMI, existing home sales, and the U.S. trade balance, alongside updates on consumer credit and inflation expectations. Overseas, investors will watch ECB meeting accounts, China's inflation data, Japan's consumer spending and producer prices, New Zealand's interest rate decision, and OPEC's latest production meeting as energy markets continue stabilizing following the reopening of shipping routes through the Strait of Hormuz.

LevelFields AI Top Stock Alert Last Week

YRD (Yiren Digital) +60% (1D) — Massive Share Repurchase Program

Shares of Yiren Digital surged roughly 60% in a single trading session after the company authorized a new $20 million share repurchase program, allowing it to repurchase up to 10% of its outstanding shares over the next 12 months.

Share buybacks reduce the number of shares outstanding, increasing each remaining shareholder's ownership stake while often boosting earnings per share over time. The announcement also signals management's confidence that the stock is materially undervalued and that repurchasing shares represents one of the best uses of the company's capital.

Beyond the buyback, Yiren continues expanding beyond its traditional consumer lending business through artificial intelligence. The company recently launched its internally developed Zhiyu large language model and significantly upgraded its MagiCube AI Agent platform, positioning itself as an AI-native fintech company focused on digital lending, insurance, and enterprise financial technology.

.png)

How to use LevelFields for Options Trading

Tracking Stocks Without Spreadsheets

The Truth About Dividend Stocks

What's LevelFields' Premium Membership Provide?

This is not financial advice. All information represent opinions only for informational purposes. Given the vast number of stocks we cover in these reports, assume staff covering stocks have positions in stocks discussed.

Have feedback or a request for specific data? Drop us a note at support@levelfields.ai